Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineUS Treasury yields surge as Fed toughens stance on mounting inflation

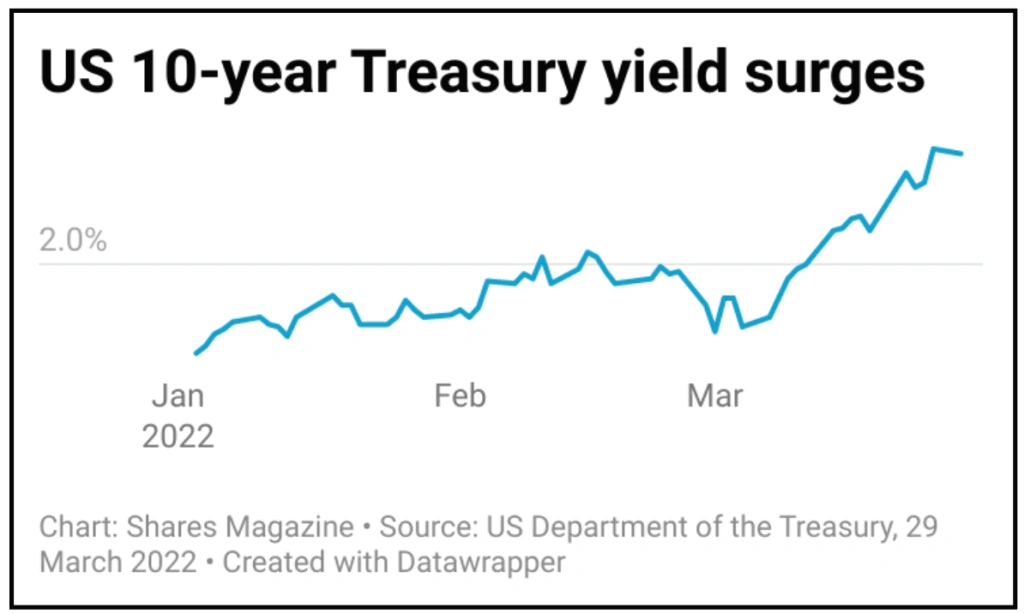

As we write March is shaping up to be the worst month for US government debt (Treasuries) since 2016. Downward pressure on prices recently pushed the 10-year Treasury yield as high as 2.5%.

This marks not far off a full percentage point increase since the beginning of 2022.

Bond prices and yields move in opposite directions, falling prices mean higher yields, while rising prices mean lower yields.

When the 10-year yield goes up, so do mortgage rates and other borrowing rates. It also impacts the rate at which companies can borrow.

This may reduce their ability to engage in projects that foster growth and innovation and maintain generous dividends to shareholders.

WHY IS IT HAPPENING?

There are two inter-related reasons that explain the recent surge in Treasury yields. First, the Federal Reserve has recently acknowledged that it underestimated the threat of inflation.

Second, after remaining stubbornly dovish in 2021, or in other words relatively relaxed about keeping rates low, Federal Reserve chairman Jerome Powell has turned far more hawkish, or committed to tightening policy.

SURGING US INFLATION

The Federal Reserve has been caught off guard by a cost-of-living crisis which has only been exacerbated by the war in Ukraine. For months senior Fed officials dismissed the surge in prices as transitory. They argued it was principally the result of the reopening of the US economy.

The Fed argued that disruptions and shortages would be transitory, and result in a rapid reversal in inflationary pressures. However, price rises accelerated and became increasingly ubiquitous.

The US consumer price index rose by 7.9% through February, the fastest pace of inflation in 40 years. Rising food and rent costs contributed to the increase, as did a nascent surge in gas prices.

The Fed has recently estimated the rate of US inflation would average 4.3% in 2022. This is up from the bank’s 2.6% estimate four months ago and just 1.9% a year earlier.

These seismic changes are decidedly out of character for a conservative central bank that rarely makes big changes to forecasts.

The 16 March outlook by the Federal Reserve for interest rate rises was far more hawkish than the market had anticipated.

The Fed has pencilled in a total of six more rate hikes, excluding the recent 25 basis point rise. It forecasts rates going to 2.8% in 2023 and staying at that level in 2024.

This represents a huge shift in its monetary policy outlook since December when the median view was for only three quarter-point hikes in 2022, and three more in 2023. The next policy announcement is on 4 May.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Feature

- Make the most of your ISA allowance: three stocks to buy now

- Recession fears: How to protect and grow your wealth if the economy weakens

- How bond fund managers analyse investments and assess risk

- How important are commodities in the Brazilian economy and market?

- Emerging markets: Views from the experts

Great Ideas

- ConvaTec has turned a corner and offers growth and re-rating potential

- AG Barr fizzes to profit ahead of pre-Covid levels

- SDI’s £7.7 million deal to immediately boost earnings

- Homeserve shares surge higher on bid approach

- Value specialist Temple Bar is well placed for inflation and rising rates

- Beat inflation with Diversified Energy’s big dividends

- Strong demand drives gains in logistics, residential and development

- Our faith in the managers is undiminished despite a slow first half

Investment Trusts

News

- What a harsh EU clampdown means for Apple, Google and other big tech firms

- Why Pendragon might be the next auto retail takeover target

- US Treasury yields surge as Fed toughens stance on mounting inflation

- Mark Barnett makes a comeback with new Tellworth equity income fund

- Terry Smith uses Fundsmith investor meeting to criticise Unilever top brass