Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineRecession fears: How to protect and grow your wealth if the economy weakens

Recession concerns have been seeping into the investment narrative in recent weeks. The war in Ukraine has exacerbated supply shortages and added unexpected fuel to the inflationary fire.

Inflation in basic non-discretionary goods crimps spending elsewhere and could put a big dent in the expected nascent global recovery.

While recession isn’t the base case for most economists, investors may do well by heeding the sage advice of French chemist Louis Pasteur, who invented some of the earliest vaccines. Pasteur said, ‘Fortune favours the prepared mind’.

In this article we look at the key factors which could tip the global economy from growth into recession and reveal four investments to weather the storm.

Don’t panic and stay focused on the long term

A recession is technically two consecutive quarters of negative growth in the economy. Recessions are a natural part of economic cycles and occur at the end of economic expansions.

Depending on their severity they should not be feared and can even be beneficial for long term investors who are able to pick up stocks on the cheap.

In terms of preparing on a practical level, paying off expensive credit card debts or consolidating debts onto a cheaper rate, if possible, is a good idea.

Try to build up a cash reserve to cover any unexpected emergencies. This is not going to be easy with rising energy and household bills, although some people may still have cash which they saved during the Covid lockdowns from not going out.

One thing everyone can do is to take advantage of the only free lunch in finance, also known as diversification.

This means spreading risk. Check your portfolio has a broad exposure to different types of assets, sectors and geographies. Reducing exposure to economically sensitive shares and upping weightings to defensives and staples should reduce volatility and risk.

What are bond markets telling investors?

It might sound bonkers, but US bond markets were flashing warning signals of recession even before the US Federal Reserve raised interest rates (16 March) by a quarter of a percentage point to 0.5%.

Even more worryingly, Fed chairman Jerome Powell has indicated more increases, potentially one at every policy committee meeting this year. This implies a Fed funds rate at 1.95% by the end of 2022. So, what’s going on?

Based on the yield curve (we’ll explain this in a second), the bond market is telling us it thinks the Fed is making a policy mistake by aggressively raising interest rates.

Admittedly, the Fed is stuck between a rock and a hard place. It has an obligation by law to tackle current high inflation and it knows the war in Ukraine is pushing up energy prices, adding to inflationary pressures.

What is the yield curve?

Investors need to look at the yield curve which is the level of expected interest rates at different points in the future.

The shape of the yield curve provides predictive information about expectations for future growth.

In a healthy economy longer term interest rates are higher than short term rates. This means the slope of the curve is upward sloping from left to right when looking at a chart.

Bonds which mature further into the future usually have higher yields because they are risker. Investors demand a higher coupon (amount of interest) to compensate them for that risk.

A 10-year government bond paying a 2% coupon provides annual income of £2 for every £100 invested.

When short term interest rates are below longer term rates, the economy is expected to continue to expand. But when long term rates fall while short term rates increase, this causes the curve to flatten or even invert.

Historically, inversions have presaged recessions – and we briefly reached the inversion point on 29 March.

The most common rates to compare are two and 10-year rates. The reason is because two-year rates more readily capture expected Fed rate rises.

This spread has narrowed from 1.6% a year ago to 0.02%. Based on prior inversions, it is possible to calculate the likelihood of recession.

According to consultancy Macro Hive, the probability (chance) has increased from 18% at the start of 2022 to 45%, a big jump.

What are the chances of a soft landing?

The Fed is attempting to engineer a soft-landing. In other words, reduce demand in the economy to cool the jobs market sufficiently to slow growth without endangering the economic expansion.

The idea is to increase the cost of money to dampen demand in the interest rate sensitive parts of the economy and thereby reduce the imbalance between supply and demand for labour.

The Fed is implicitly assuming supply chain disruptions get fixed over time and, along with higher base effects, also reduce inflation.

Soft landings are an incredibly difficult thing to achieve if history is a good guide.

Alan Blinder was Fed vice-president under chairman Alan Greenspan during the 1990s. His work showed the Fed only achieved two out of 11 soft landings during tightening cycles between 1966 and 1994.

Economic research firm TS Lombard has looked at the episodes in more detail. It reveals successful soft landings were mainly achieved when inflation was relatively well behaved.

The problem occurs when inflation is already high and perceived to be a problem by the Fed. Sound familiar? It should do because Powell has categorically said the Fed needs to tackle inflation which at 8% is too hot to maintain long term price stability.

Without price stability the Fed believes it cannot deliver on the second part of its dual mandate to achieve maximum employment.

TS Lombard believes if inflation turns out not to be transitory and remains above what the Fed can tolerate, the chances of a soft landing are practically zero.

Europe is in the eye of the storm

While the US may escape a recession, the EU is in a more precarious position due to its proximity and economic ties to Ukraine and Russia.

The OECD (Organisation for Economic Co-operation and Development) estimates the conflict and rise in commodity prices could slow the EU economy by 1.4% in 2022.

Goldman Sachs estimates cutting off energy supplies to Europe might knock 2.2% off growth and push the region into recession.

Even more worrying, economists Lutz Kilian and Michael Plante at the Dallas Federal Reserve Bank have warned of global recession if oil prices remain elevated.

The burden of shoring up consumer confidence and mitigating inflation will fall on national governments. Ireland and France have said they will subsidise rising fuel prices and other countries will probably follow suit.

In his spring statement (23 March) UK chancellor Rishi Sunak temporarily lowered duty on petrol by 5p per litre and reduced VAT on energy saving devices to zero from 5%.

Despite government help, the outlook for the UK consumer looks pretty scary after the OBR (Office for Budget Responsibility) said it expects real disposable income to fall to the lowest level since records began in the 1950s.

It is not just rising energy costs hitting the consumer’s pocket. There has been major disruption to fertiliser supplies because Russia and Belarus are two of the biggest exporters. Fertilisers are needed to maintain and improve crop yields.

Disruption to supplies has the potential to hinder crop production in many parts of the world when food prices are already high.

No one has a crystal ball with perfect foresight, but the evidence suggests taking precautionary action with your investments now could pay off later. Here are four suggestions for investments to own given what’s potentially on the horizon.

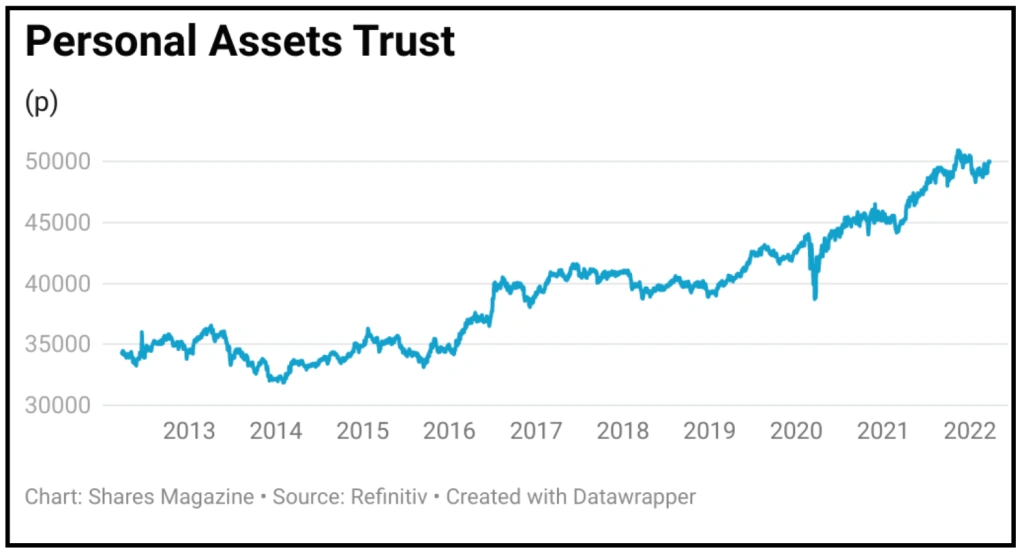

Personal Assets Trust (PNL)

Price: £498.50 Market Cap: £1.79 billion

This trust is well positioned to provide downside protection in poor equity market conditions while also participating in upswings.

The trust’s objective is to protect and grow shareholder value over the long-term. It can invest across different asset classes to find the best risk-to-reward opportunities.

Importantly returns have been delivered with less than half of the volatility (how much the price moves) of the index. Indeed, the trust has one of the lowest volatilities in the unconstrained sector.

The manager is concerned about the economic outlook and the high valuation of both bonds and equities. The priority is therefore to preserve capital.

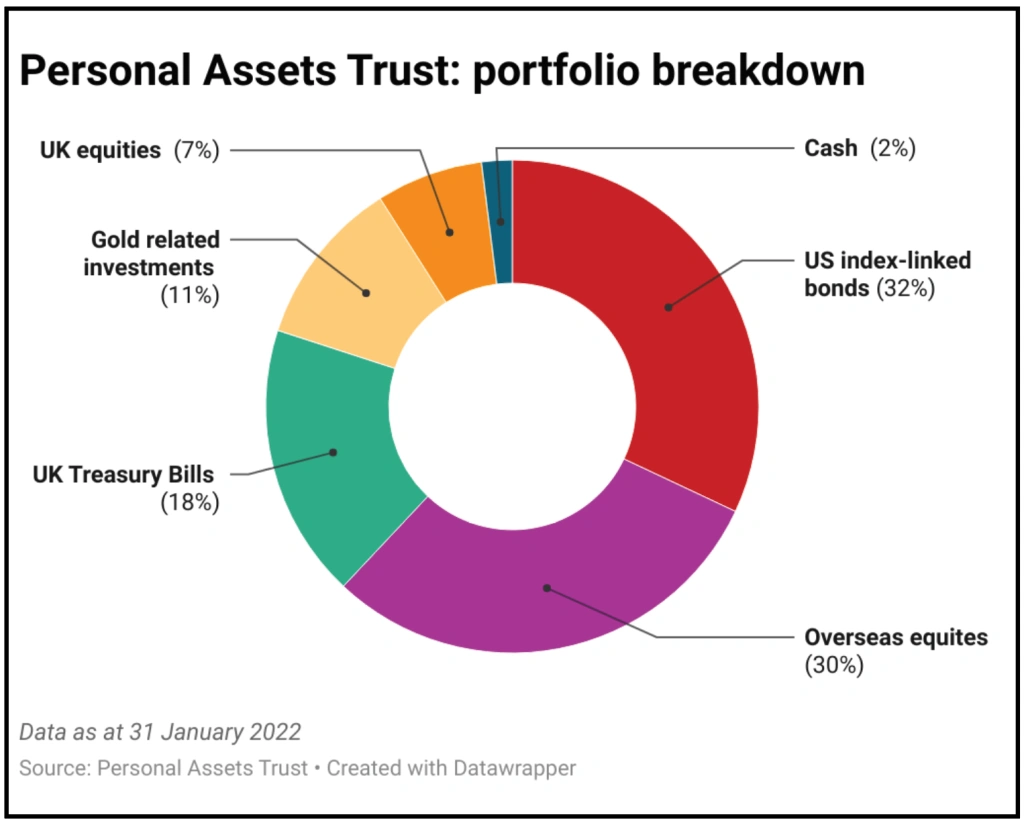

Equity exposure is at the low end of the 15-year range (32%-72%) at 37%. The equity assets are concentrated in companies with quality characteristics, with Microsoft (MSFT) and Alphabet (GOOG) the two largest holdings.

US inflation-linked bonds represent 32% of the net asset value. The manager believes these will provide some protection against a backdrop of low real interest rates and rising inflation.

UK Treasury bills and cash represent 20% of the net asset value, while gold related exposure is 11%. The trust has an ongoing charge of 0.73% a year.

Polar Capital Global Healthcare Trust (PCGH)

Price: 288p Market Cap: £350 million

Healthcare is considered non-discretionary expenditure which gives the sector defensive qualities during economic downturns.

In addition, spending on healthcare has more than kept pace with inflation, making it doubly attractive when inflation is high.

The £350 million Polar Capital Global Healthcare Trust (PCGH) trades at an 11% discount to net asset value which looks attractive given the improved performance over the last year.

The trust handsomely outperformed the MSCI Global Healthcare index, delivering a total return in NAV of 18.4% compared with the 14.7% return of the benchmark.

Over the three years performance is marginally ahead of the benchmark.

The trust’s mandate was changed in June 2017 to focus more on capital growth, rather than the previous focus on income. The investment approach is high conviction and actively traded.

The managers can invest up to 20% of assets in small cap innovators that drive disruption leading to new drugs and surgical treatments.

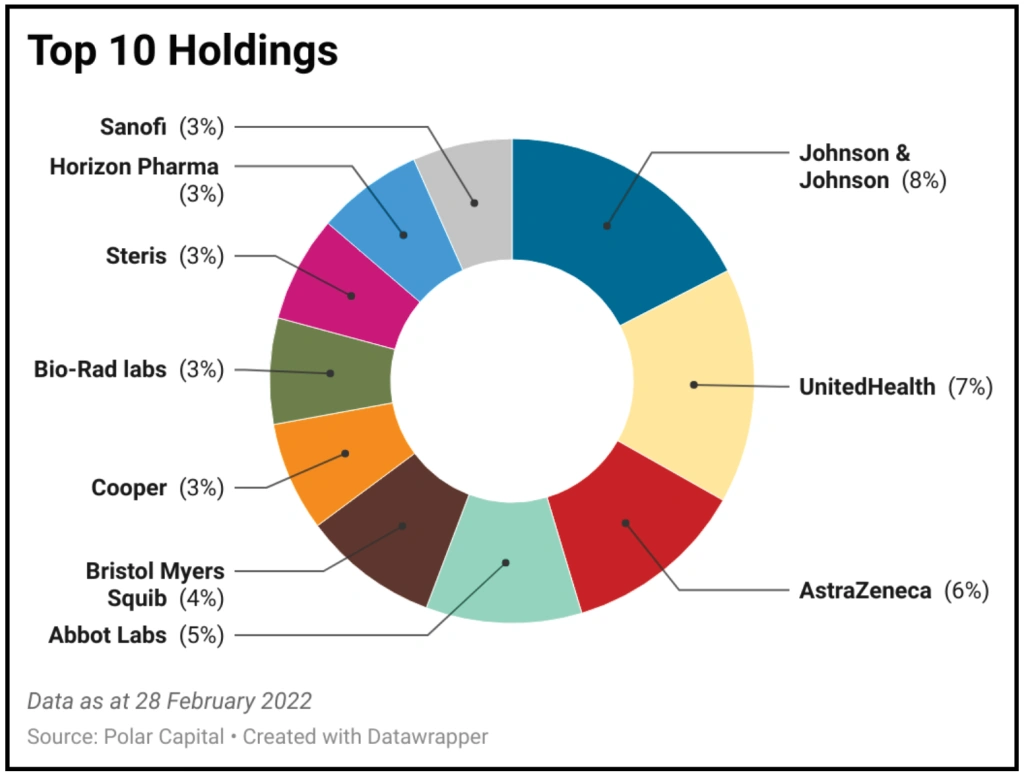

A key characteristic of the portfolio is its underweighting of pharmaceutical companies which represent the largest component of the benchmark, around 38%.

Instead, the trust is overweight healthcare equipment and facilities companies as well as biotechnology firms.

The trust’s largest weightings are in Johnson & Johnson, UnitedHealth and AstraZeneca (AZN). The annual ongoing charge is 1.09%, in line with sector peers.

Vodafone (VOD)

Price: 125.8p Market cap: £35.3 billion

While investors have become obsessed with growth over the last few years, telecommunications companies have flown under the radar. However, we believe they are a good place to invest ahead of a downturn.

Their income is more reliable and less economically sensitive, giving them a defensive quality.

In addition, they tend to pass through inflation which means they are decent hedges against rising prices.

Because they are considered dull, their ratings tend to be modest in relation to the market. Vodafone (VOD) has a 6.1% prospective dividend yield and trades on a modest 13 times price to earnings ratio.

This looks cheap compared with the 14% earnings growth that analysts expect over the next couple of years. Vodafone is making operational improvements with the intention of increasing returns on capital.

An additional potential upside for investors is increased interest in the sector from private equity buyers looking for bargains. Cevian Capital is rumoured to have built up an undisclosed stake in Vodafone.

While analysts at Numis Securities remain sceptical about the extent to which Cevian Capital may be able to force Vodafone’s hand, they do believe the investor’s interest could spark a re-evaluation of Vodafone’s business model, strategy and scope for profits recovery.

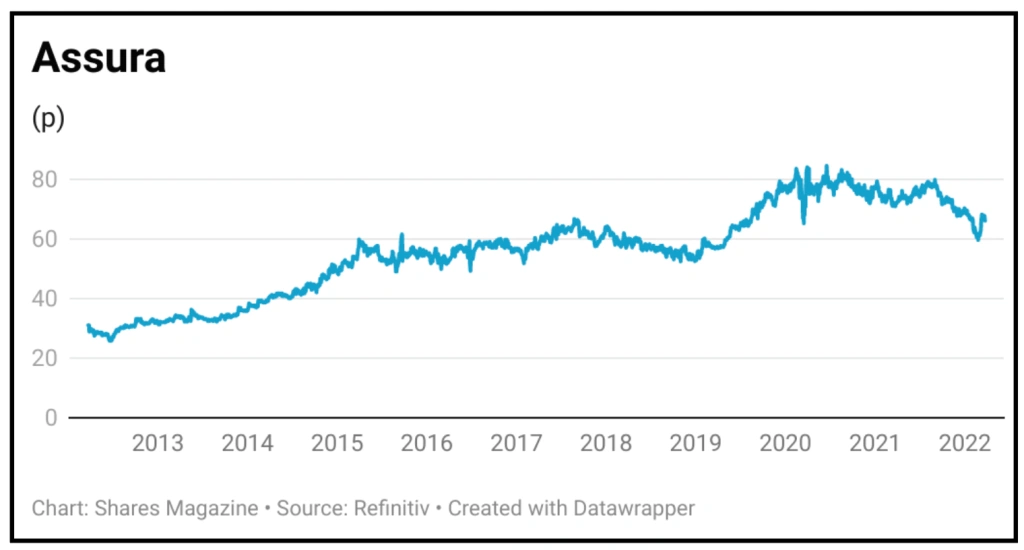

Assura (AGR)

Price: 65.9p Market Cap: £1.96 billion

Real estate investment trust Assura (AGR) owns and develops medical centres serving GP (general practitioner) practices.

The NHS wants to modernise legacy assets and increase community-based services. The government is supportive of private capital getting involved to support its goals.

Roughly 45% of UK primary care medical centres are owned by GPs, usually as part of their pension provision. But younger GPs are increasingly choosing not to participate in property ownership according to Shore Capital.

This means older GPs are looking for exits through disposals to specialist REITs like Assura, which has built up a rough 6% share of the UK market.

Assura’s shares trade at a 2% discount to its net asset value compared with an 11% premium for rival Primary Health Properties (PHP).

Shore Capital believes the discount is unwarranted given Assura’s superior prospective dividend yield of 5% and better dividend growth profile emanating from its development pipeline.

Growth is expected to come from a pipeline of new medical centres estimated to be worth around £480 million, plus bolt-on acquisitions.

The shares offer defensive growth and an attractive yield while regular rent reviews provide some inflation protection.

The company minimises rent risk when developing new properties by pre-letting them before construction starts.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Feature

- Make the most of your ISA allowance: three stocks to buy now

- Recession fears: How to protect and grow your wealth if the economy weakens

- How bond fund managers analyse investments and assess risk

- How important are commodities in the Brazilian economy and market?

- Emerging markets: Views from the experts

Great Ideas

- ConvaTec has turned a corner and offers growth and re-rating potential

- AG Barr fizzes to profit ahead of pre-Covid levels

- SDI’s £7.7 million deal to immediately boost earnings

- Homeserve shares surge higher on bid approach

- Value specialist Temple Bar is well placed for inflation and rising rates

- Beat inflation with Diversified Energy’s big dividends

- Strong demand drives gains in logistics, residential and development

- Our faith in the managers is undiminished despite a slow first half

Investment Trusts

News

- What a harsh EU clampdown means for Apple, Google and other big tech firms

- Why Pendragon might be the next auto retail takeover target

- US Treasury yields surge as Fed toughens stance on mounting inflation

- Mark Barnett makes a comeback with new Tellworth equity income fund

- Terry Smith uses Fundsmith investor meeting to criticise Unilever top brass