Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineTime to take profits on IT security group Avast

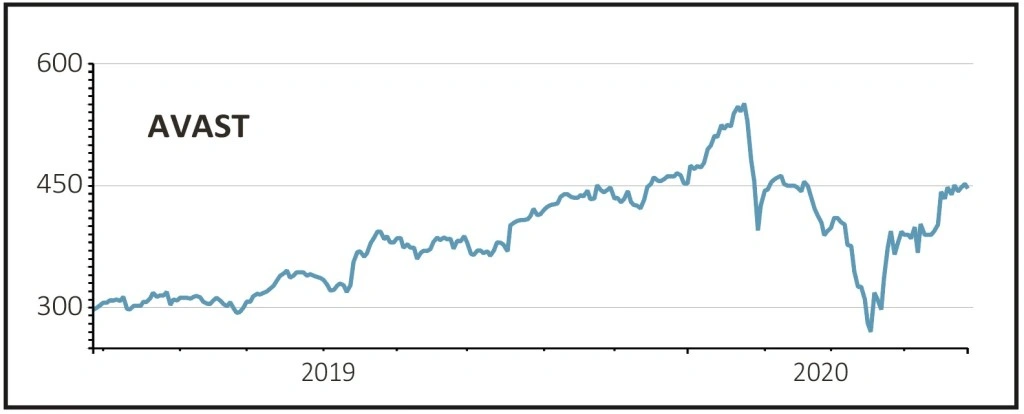

AVAST (AVST) 450.6p

Gain to date: 50.8%

Original entry point: Buy at 298.8p, 16 May 2019

To call the recent rally for IT security firm Avast (AVST) pronounced would be an understatement. The stock has jumped by two thirds in a month since hitting pandemic panic lows of 270.6p in March, sparking a big paper profit recovery for our original investment pitch.

Driving that rapid recovery is a market mood buoyed by an impressively stable first quarter, with a 3.1% increase in adjusted earnings before interest, tax, depreciation and amortisation (EBITDA) to $121.2m.

That was on $213.1m revenue, 6.5% ahead once the defunct Jumpshot business is excluded and currency oscillations are flattened out, implying 56.9% margins, up on 2019’s 55.3%. It also committed to pay the $0.10 per share 2019 final dividend.

Avast saw freemium-to-paid conversion rates and billings accelerate for its desktop solutions as customers increasingly worked from home, although weaker advertising rates came as no surprise. Mobile security sales are still very slow though.

A robust balance sheet is comfortably within banking covenants, with more than $1bn of borrowing capacity available.

SHARES SAYS: Avast remains a robust business but slow mobile progress continues to grate. This is a sensible time to crystallise those paper profits into hard cash. Sell.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

First-time Investor

Great Ideas

- Digital change expert Kainos remains a great pick

- Time to take profits on IT security group Avast

- Computacenter resilient but dividends are off the menu

- Luceco can move beyond ‘darkest hour’

- Buy ITV shares as advertising activity could soon pick up

- Travis Perkins can capitalise on homebuilding restart