Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhat does coronavirus mean for markets long-term?

In last week’s edition this column looked at the potential near-term implications for financial markets of the coronavirus outbreak.

At the time of writing, markets are still trying to rally and are being encouraged to do so by the combination of ongoing monetary and fiscal support from central banks and governments and a gradual move in some nations to ending the lockdown.

Italy, the initial epicentre of the European outbreak, is relaxing its rules step-by-step and Milan’s MIB-30 index continues to make steady progress as a result.

It is to be hoped that the trend remains down, for humanitarian reasons above all others and if so investors might have to start thinking about not just the shape and nature of the economic recovery in the short-term but the longer-term implications of the outbreak and how the authorities, companies and individuals responded.

TRIO OF OPTIONS

From this column’s perspective, looking at the outbreak solely through the narrow prism of investment, there are three crude alternatives: everything goes on as before; a few things change; or there are radical shifts in behaviour which could have profound implications for markets and asset valuations.

Option 1: Business carries on as before and firms behave in the same way as before. The world recovered quickly after 9/11 in 2001 and it was not that long after the financial crisis of 2007-09 that merger and acquisition activity, stock buybacks, adjusted earnings numbers and other forms of financial engineering were back in fashion and WeWork was being valued at $48bn by its backers.

Moreover, private individuals who had been frightened about losing their money on a bank run in 2008 were, barely a decade later, at various stages paying $900 a share for Tesla and nearly $20,000 for a Bitcoin.

To paraphrase JK Galbraith, such is the extreme brevity of the financial memory and it may be that risk appetite recovers quickly and markets carry on as before, especially as central banks seem happy to backstop them with bounteous liquidity in the form of the quantitative easing (QE) and zero interest rate policy (ZIRP) schemes.

Option 2: Company behaviour does alter in some ways. One change that is perfectly possible is companies abandon theories of efficient balance sheets and the primacy of return on equity and focus instead on cash. Just like any private individual listening to their financial adviser, their first step is to build a cash buffer and then sit on it, so that six to 12 months’ operational and capital expenses can be met whatever the circumstances.

Debt and leverage to goose returns go out of fashion. Managers breathe more easily but shareholders get lower profits, lower returns on equity and less dividend growth, perhaps with the result that dividends do not return to 2019’s levels for some time.

The logical corollary of all of this is that equities suffer a de-rating. Even as profits recover (the E in the price-to-earnings ratio), the multiple that investors are prepared to pay (the P) goes down and equity returns are crimped.

Such fallow periods are not unprecedented. Japan turned away from borrowing toward saving after its bubble burst in 1989 and the Nikkei 225 stock index stands at barely half of where it did at its peak as a result. The irony then is that Japanese returns on equity (now on the way back up under Abenomics) meet American and British ones on the way down.

Option 3: Things change a lot. Under the first two scenarios, stock markets may rise or at least flip-flop to give traders something to tackle according to whether central banks are applying or vainly trying to withdraw stimulus.

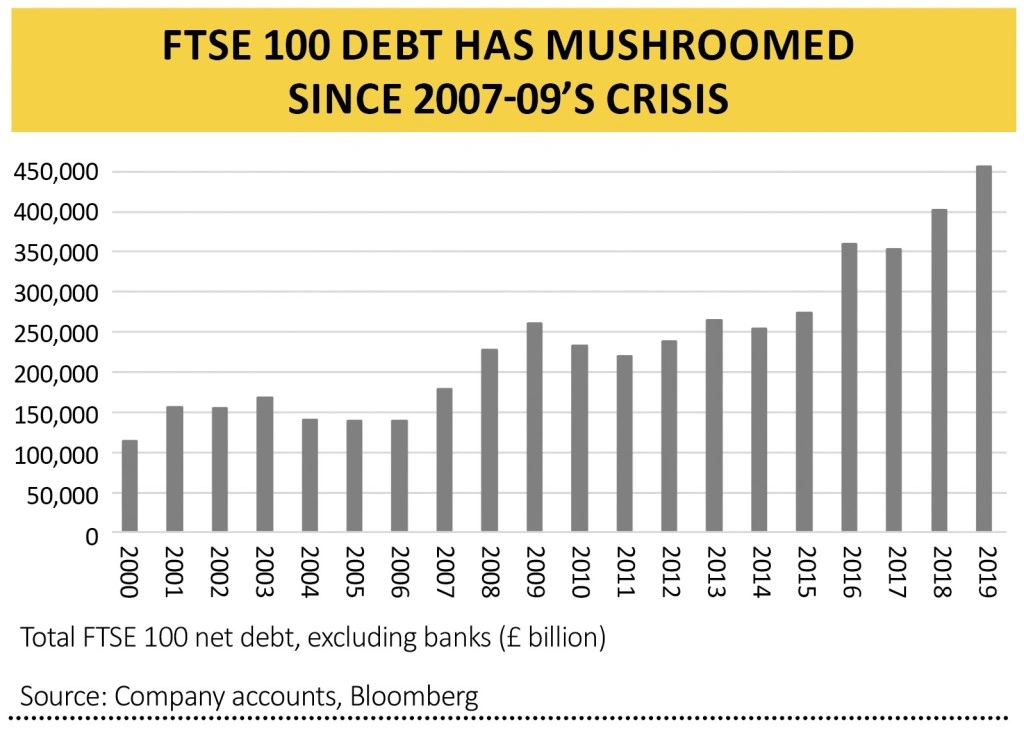

It is tempting to think Japan’s experiences cannot be repeated but the FTSE 100 traded at 6,930 in December 1999 and it stands near 5,800 today, after some 21 years’ huffing and puffing. Such a world also places an even greater emphasis on dividends as part of equities' total return.

The third scenario is more serious still. Government is providing support to many firms through multiple schemes. It may exact a price in the future. Banks and insurers have already been asked by regulators to cancel dividends and buyback programmes. Taxes could rise.

Firms that are perceived by the public/politicians/both to have ‘behaved badly’ may find themselves under greater scrutiny. Reputations could be tarnished in the current, extraordinary environment, fairly or unfairly, with long-term repercussions for how firms are perceived by customers, to the potential detriment of revenues and business levels – and ultimately the value of their stock.

Greater regulatory or state-intervention is generally anathema to financial markets (rightly or wrongly) and firms should do their bit to avoid this by focusing on the needs of staff and customers (stakeholders) more than ever. If they can do that well, the rest may well take care of itself over time.

Shareholder value comes from firms providing a service or product to customers and doing it well, to the satisfaction of those customers. Shareholder value is not an end or aim in its own right. It is impossible to create any value if you have no (happy) customers, as current circumstances show.

But happy customers served by happy staff is the dream ticket that leads to profits, cash flow and ultimately the dividends which could prove even more valuable if the West really is about to get some Japan-style returns for a while.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

First-time Investor

Great Ideas

- Digital change expert Kainos remains a great pick

- Time to take profits on IT security group Avast

- Computacenter resilient but dividends are off the menu

- Luceco can move beyond ‘darkest hour’

- Buy ITV shares as advertising activity could soon pick up

- Travis Perkins can capitalise on homebuilding restart