Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineHow fund managers are reacting to the coronavirus crisis

Just as retail investors are being forced to deal with significant disruption to the markets, so too professional fund managers are having to react to the new realities created by the coronavirus outbreak.

In this article Shares talks to the people at the helm of two popular investment trusts to get some insight into how they are coping with the current volatility.

With its focus on ‘safety first’ and running a resilient portfolio, Mid Wynd International Investment Trust (MWY), has been one of the better performers in the global equity arena during the coronavirus crisis.

One of Shares’ running Great Ideas selections, from the start of the year to the market close on 25 March, Mid Wynd shares were down 9.7% against a fall of 15.9% in the Morningstar Global Equity sector, according to data from the Association of Investment Companies (AIC). The trust’s net asset value (NAV) fell by 10.5%.

Managed by the Artemis Global Select team of fund managers, Mid Wynd invests across the globe using a thematic approach. Among the long-term themes it invests in are online services, automation, high-quality assets, healthcare and the move towards a low-carbon future.

BENEFITS OF DIVERSIFICATION

In terms of the portfolio, the managers try to keep a balance between ‘quality growth’ stocks, which can deliver predictable profit growth but tend to trade at a premium to the rest of the market, and ‘defensive’ asset-backed stocks which typically trade on lower multiples.

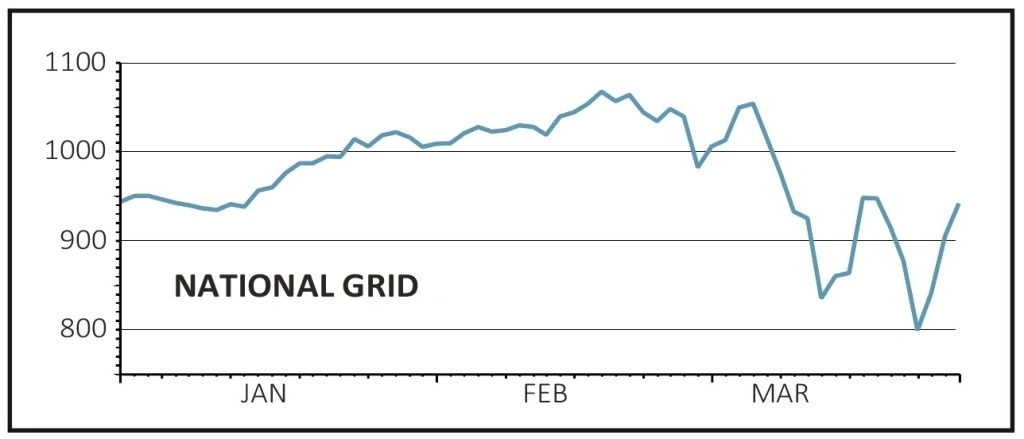

This split helped performance during February thanks to holdings in ‘defensive’ utility companies such as National Grid (GN.) and Iberdrola, which thematically encompass both the move towards a lower-carbon economy and the need for high-quality real assets. Although the trust doesn’t focus on income, the fact that both stocks carry attractive dividend yields is a bonus.

Due to the managers’ conviction that equity markets were highly-rated going into the crisis, the trust had a sizeable cash position which has helped it weather some of the sell-off in stocks. With governments and central banks around the world launching unprecedented stimulus and aid measures, the team is now putting cash to work buying high-quality, resilient stocks at deeply discounted prices.

US EXPOSURE REDUCED

As part of its strategy the trust cut its US exposure from over 56% to below 50% by selling out of banks, railways and other sectors with direct exposure to the US economy.

According to manager Simon Edelsten, ‘The US is only now going into measures which will slow activity while some of Asia is emerging from those measures.’

The fact that US citizens are not used to the government telling them how to live – and are more anxious about the economic and financial costs of the virus than the potential health risks – means the crisis could last well into the summer, creating a recession.

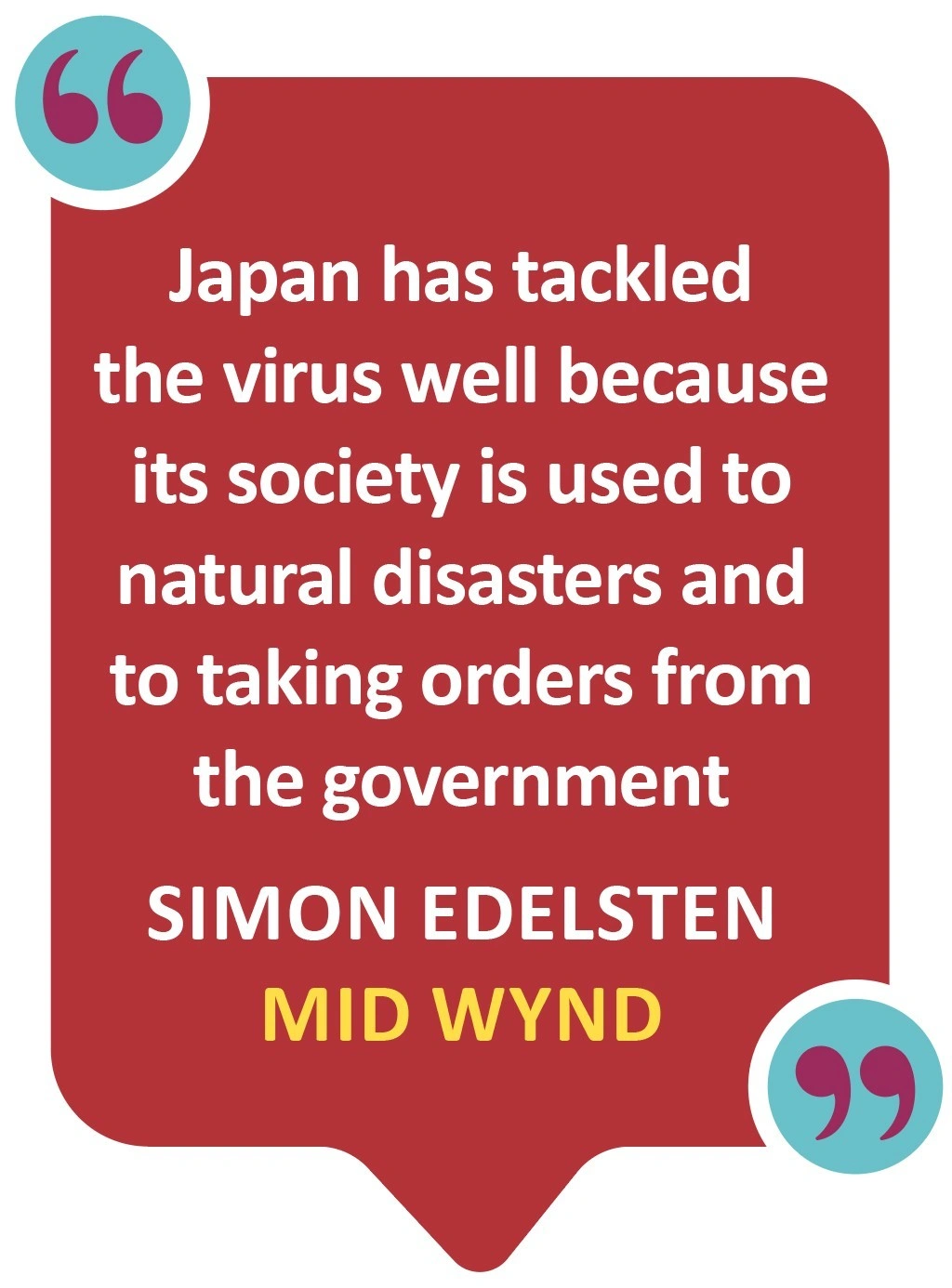

Instead the team has increased its exposure to Asian markets, notably Japan which has risen from around 12% of the portfolio to 17% with the addition of automation and telecoms stocks such as Hoya and Nippon Telegraph.

‘Japan has tackled the virus well because its society is used to natural disasters and to taking orders from the government,’ says Edelsten.

The trust’s exposure to China and other Asian markets has also risen with investments such as chipmaker Taiwan Semiconductor and telephone mast operator China Tower, which is a play on the roll-out of 5G technology.

‘By switching money out of the US, some of the valuation risk in the portfolio has been reduced,’ adds Edelsten. The trust has been able to buy high-quality non-US stocks with strong balance sheets at low multiples, thereby giving it more upside potential should markets mount a concerted rally.

Longer-term, as the global economic demand recovers and factories have to ramp up supply, Edelsten expects the trust’s automation and technology holdings to do particularly well.

RADICAL CHANGES

Edelsten’s counterpart at the £475m Scottish Investment Trust (SCIN), Alasdair McKinnon made radical changes to his portfolio in early February as supply chain issues across Hubei province started to become apparent.

While the market seemed oblivious to the gathering storm clouds amid the virus reaching Italy, McKinnon and his team were busily changing the shape of the trust’s portfolio which resulted in making as many changes to the fund in a couple of weeks as they would normally make in a whole year.

The team debated what the lockdown in China meant for the rest of the world. Their sense was that if such a scenario happened elsewhere, earnings forecasts couldn’t be relied upon.

Without any idea of likely near-term cash flows, it is nigh on impossible to value companies whose earnings visibility isn’t that great to begin with, what natural contrarian McKinnon calls his ‘Ugly Ducklings’. These are ‘out of favour’ companies whose near-term outlook is foggy at best.

Before February the fund had a 60% to 70% weighting in these types of businesses. In less than two weeks, the weighting was shredded to 40% with the remainder in what the team considers to be better quality companies, with ‘much greater earnings visibility’.

Out went US retailers Target, Gap and Macy’s as well as UK retailer Marks & Spencer (MKS). Holdings in banks were reduced with sales in Royal Bank of Scotland (RBS), French bank

BNP and Dutch insurer ING.

STABLE AND DEFENSIVE

In their place McKinnon populated the portfolio with companies whose revenues were perceived to be relatively insulated from the general economy and where cash generation was robust. The move was more about survival than any other consideration.

New purchases included Japan Tobacco, which was preferred over UK equivalents Imperial Brands (IMB) and British American Tobacco (BATS) because it isn’t as heavily indebted.

UK utilities Severn Trent (SVN) and National Grid (NG.) were added to the portfolio as well as US firms Duke Energy and Dominion. US Healthcare giant Gilead Sciences was another addition as well as adding to the position in Pfizer.

The fund’s weight in gold miners was increased, adding to Newmont, Barrick Gold and Newcrest Mining, and collectively they now represent a significant 25% of the portfolio.

The team’s rationale was that these firms are more disciplined and efficient operators than in the past.

McKinnon believes the stimulus measures seen so far will go some way towards mitigating the economic fall-out from the pandemic. If those actions are enough to generate a sharp v-shaped recovery, deep-value cyclicals will probably perform the best.

However, that prospect is someway off and for now the fund manager is more comfortable sticking to his defensive posture.

According to Morningstar data, over the last month the trust has outperformed its benchmark, with the NAV down 13.8% against the FTSE World index which is down 15.1%. However, over three years the fund has delivered an average annual return of minus 1.1% against plus 3.5% for the benchmark.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Feature

First-time Investor

Great Ideas

Investment Trusts

News

- Market mood lifted by huge financial support but investors remain wary

- Why oil prices have plunged to 18-year lows

- Housing market goes into coronavirus hibernation

- Bill Ackman sets record straight after $2.6bn win

- Temple Bar dumps holdings after share price collapse

- Byotrol steps up in the fight against coronavirus

- Have capital preservation funds lived up to their name?