Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazine6 of the best income funds

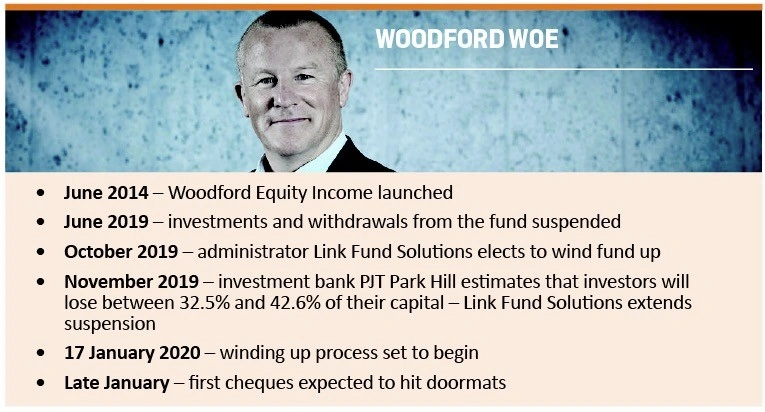

The recent fiasco surrounding Neil Woodford’s Equity Income fund will have left many people burnt by the experience and unsure of how to get a decent income on their money.

However, cases like Woodford are actually very unusual and there are excellent funds and investment trusts with track records of consistently paying out generous dividends over the long-term. In this article the Shares team reveals six of its very best income fund ideas.

THE BACKGROUND

An estimated 300,000 investors caught up the Woodford affair will start receiving cheques from Link Fund Solutions in January. The administrator has confirmed that it expects the winding-up process to begin on 17 January 2020, with first payments likely to reach investors later that month.

Winding up a fund means closing it down and returning cash to investors, usually in instalments as the assets are sold off, a move that the one-time star fund manager Neil Woodford was dead set against.

‘This was Link’s decision and one I cannot accept, nor believe is in the long-term interests of Woodford Equity Income fund investors’, he said when the decision was announced.

Investors will certainly not be celebrating getting their money back. They face losing at least a third of the savings they originally invested, according to an analysis by the experts shipped in to oversee the sale of the fund’s assets.

Investment bank PJT Park Hill was called in by Link Fund Solutions to run an analysis of the likely scale of losses that would result from the sale of Woodford Equity Income’s more illiquid assets, and the resulting figures make grim reading.

On PJT’s base case, investors face losses on their capital of 32.5%. In other words, for every £1,000 an investor had put into the fund, they’ll get just £675 back. That’s the base case. Under PJT’s worst case scenario losses could total 42.6%, handing back to investors just £574 for every £1,000 of capital invested. More on why, later.

INCOME NEED NEVER GREATER

With bond yields and bank rates at record lows, and rental property struggling to give attractive returns, (and possibly facing a tax attack in future, depending on the election result), investors have never been as starved for good, solid and safe income investment options.

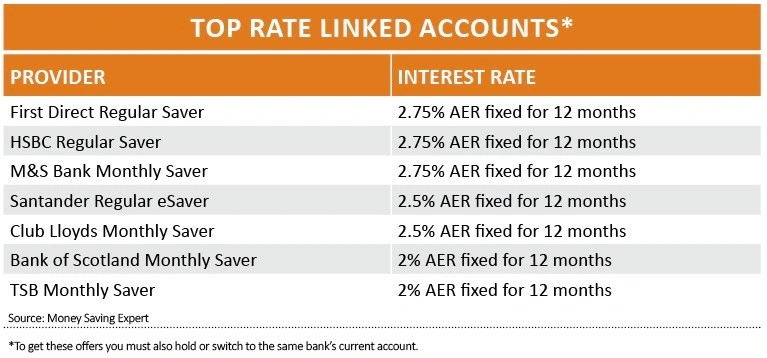

For example, the yield on a 10-year UK gilt is currently just 0.7%, while 2.75% is the best the banks can do on long-term savings, according to Martin Lewis’ Money Saving Expert website, and that’s with caveats.

The Woodford debacle may have done substantial damage to the reputation of the investment industry, and particularly the income sphere, but experts stress the saga is atypical.

‘The problems with the Woodford fund were high profile, but it’s important to remember that he is just one fund manager and it’s the only example of such a large fund being suspended and then liquidated in recent history,’ says Laura Suter, personal finance analyst at investment platform AJ Bell.

We agree and continue to believe that funds and investment trusts can provide solutions whatever an investor’s requirements might be.

The six hand-picked fund and trust options in this article provide a good starting point for further research, whether you are just starting out in saving for your long-term future, or are approaching or already in retirement.

DANGERS OF OFF-MARKET INVESTING

Part of the reason for the hefty losses incurred by the Woodford fund is that a large chunk of the capital it invested on behalf of its fund holders was placed into illiquid, privately-owned start-up businesses.

Selling on such assets is much more difficult than it would be to offload stakes in stock market-listed companies, where buyers can readily be found for unwanted stock. This means that getting shot of stakes in off-market, private businesses will usually mean selling at prices far below previous book values.

‘Given these estimates are over and above what investors have already lost through the underperformance of the fund, it could mean investors’ overall see their investment shrink by even more,’ said Adrian Lowcock, head of personal investing at financial services firm Willis Owen.

Woodford Equity Income, which reached a peak size of £10.2bn in 2017, saw assets collapse to just £3.7bn as savers reacted to a dismal run over the past three years and withdrew cash. The loss of a key client in May, reported to be Kent County Council, appears to have been the straw which broke the camel’s back, hence the suspension in June.

COMPOUNDING OVER THE LONG-TERM

Long-term data shows the scale of impact income can have on investment returns thanks to compounding. Once described by Albert Einstein as the eighth wonder of the world, compounding has a seemingly magical way of super-charging investment growth.

Compounding describes the process where the returns from an investment themselves generate future gains. The value of an investment can increase exponentially because growth is earned on both the initial sum of money plus the accumulated wealth.

Imagine you invest £1,000 in a stock and it increases by 5% in year one to £1,050. If the stock rises by another 5% in year two, it will be worth £1,102.50. In the first year you earned £50 and in the second year you earned £52.50. The effect is the same whether you are compounding capital returns over time, or income that is then re-invested back into the stock.

The impact of compounding becomes very powerful if you invest for a long time. In fact, it takes around a decade for the effects to be really noticeable. It is perhaps why legendary American investor Warren Buffett once asserted: ‘If you don’t feel comfortable owning a stock for 10 years, you shouldn’t own it for 10 minutes.’

Over the last century, around 75% of the return from UK equities has come purely from the dividend yield, according to the well-respected Barclays Equity Gilt Study.

‘This is often forgotten in bull markets, when investors are chasing big gains in share prices’, say experts at fund management firm Liontrust.

Barclays’ annual study shows reinvesting dividends can make a significant difference to overall returns in the long-term. An investment of £100 in UK shares in 1899 would have been worth only £173 in real terms at the end of 2018 based on capital growth in the Barclays UK Equity Index alone.

But had all the dividends received over the years been reinvested back into buying more shares, the total value of the portfolio would have soared to £30,776 over the same period.

Equity income funds can be a good long-term savings vehicle for investors able to tolerate the additional risk, with the potential for capital growth along with the compounding effect we have highlighted. But it needs drumming into investors that higher returns potential equates to more risks, so individuals must assess their own level of comfort.

Neil Woodford moved away from what had made him so successful at his previous employer Invesco Perpetual, where he pretty much concentrated on buying larger cap stocks whose income potential had been undervalued by the market.

One of his big calls was buying big tobacco stocks in the early 1990s, when others were worried that aggressive US authorities would drive them out of business. He subsequently benefited from significant capital gains and a steady flow of dividends, a far cry in investment style from chasing capital growth from start-ups.

City of London (CTY)

417p. Yield: 4.6%. Five-year annualised returns: 6.2%

Source: Morningstar

Good for someone looking to achieve strong compound returns over the long term

The dividend track record of City of London (CTY) is exceptional. It has raised the dividend each and every year since 1967. And these are not just piecemeal increases, dividend growth might not be spectacular but it is solid – averaging around 5% over the last five years. The yield is also generous at 4.6%. These attributes have been recognised by investors and accordingly shares in the investment trust trade at a slight premium to net asset value.

The approach is underpinned by exposure to a large number of FTSE 100 stocks including Royal Dutch Shell (RDSB), Diageo (DGE) and Unilever (ULVR) which themselves have enviable track records as income stocks. The focus is very much on cash generative businesses which can continue to fund dividends into the future.

The portfolio sees relatively limited turnover and is well-diversified, encompassing around 100 holdings. That means one or two dividend cuts shouldn’t undermine the dividend-paying capacity of the trust as a whole. Like other investment trusts, City of London can (and does) hold some of the income it receives back as a buffer against hard times. At the helm is Job Curtis who has been in post since 1991.

JP Morgan Global Growth & Income (JPGI)

340p. Yield: 3.8%. Five year annualised return: 14.4%

Source: JPMorgan

Ideal for investors looking for a regular, predictable income while leaving their capital to compound

With a quarterly dividend and the freedom to tap into the best ideas from JPMorgan’s hugely-experienced research team, the JP Morgan Global Growth & Income (JPGI) trust is described as a ‘go-anywhere’ fund designed to provide index-beating total returns over the long term.

Run by a trio of managers – all multi-year veterans of the firm – the trust holds a concentrated portfolio of between 50 and 90 stocks selected using a fundamental, bottom-up process which is agnostic of country or sector benchmarks. The managers typically take a five-year view when picking stocks, with a focus on growth and cash generation. Current holdings include shares in blue-chip companies such as Amazon, Diageo and Microsoft as well as high-quality corporate bonds.

There is good daily liquidity in the trust’s shares, and the ongoing charge of 0.56% is one of the lowest in the sector. Dividends are set at the beginning of the year at roughly 4% of net asset value (NAV), and over the last five years the payout has increased by an average of 30% per year. Although this average is inflated by a big step up in the dividend in 2016 as the company introduced a revised distribution policy.

Given the trust’s record of compounding value over the long term, we believe investors shouldn’t be put off by the small (2%) premium to NAV at which the shares currently trade.

Jupiter Asian Income (BZ2YND8)

160.14p. Yield: 3.8%. 3 year annualised returns: 9.6%

Source: Morningstar

Suitable for higher risk, patient investors in the accumulation phase of their life

Asset manager Jupiter says by next year the number of Asian companies offering dividends in excess of 4% should have tripled since 2001.

Its Asian Income fund invests in ‘reliable’ asset-backed companies, according to Jupiter vice chairman Edward Bonham Carter.

Fund manager Jason Pidcock is highly regarded and considered to be a real expert in spotting opportunities in the Asian market.

‘Companies must have strong management and a sustainable advantage allowing them to generate cash over a long period to fund dividends,’ says the investment team at AJ Bell about how the fund picks stocks.

The portfolio includes positions in Samsung Electronics and gambling resorts specialist Sands China. The minimum market cap for companies in the portfolio is $2.5bn.

Bonham Carter says Jupiter Asian Income has outperformed in 85.7% of down markets since April 2016 and a stress test indicates it could liquidate 78% of its portfolio in just three days, should investors all want to get out.

This fund would suit someone looking to back cash-generative businesses and where they can reinvest dividends to enjoy compounding benefits. It is higher risk because a large portion of the portfolio is invested in emerging markets.

Legg Mason IF RARE Global InfrastructureIncome Fund (BZ01WT0)

135p. Yield: 5.95%. Three year annualised return: 12.7%

Source: Morningstar

Suitable for individuals with investment time frames of five years or longer, looking to protect future income from inflation

The objective of the fund is to provide an income comprised of dividends as well as achieve long-term capital growth. It was established in 2006 and offers expertise across global infrastructure projects with the aim of investing in high-quality listed assets.

Its goal is to deliver absolute returns over an investment cycle and specifically to beat average inflation across the largest group of seven (G7) nations by 5.5% a year. The fund has 34 holdings and the top 10 represent around 43% of the total holdings. Electric and gas assets are the largest areas of the fund’s exposure and represent over 72% of the portfolio. In geography terms, Canada, the US and the UK assets represent half of the portfolio.

The managers invest the fund’s assets in large listed companies involved in building roads, bridges or airports. The largest company in the portfolio is Canadian based Enbridge, which is involved in energy transportation and distribution. The UK’s National Grid (NG.) is in the top 10 holdings of the fund, as is energy supplier SSE (SSE).

TB Evenlode Global Income (BF1QMV6)

127.39p. Yield: 2.2%. Five year annualised return: N/A

Source: Trustnet

Long-term investors seeking dividend growth with the prospect of some capital growth are ideal for this fund

Managed by Ben Peters and Chris Elliott, the Evenlode Global Income (BF1QMV6) fund was launched in late 2017 with the intention of replicating Cotswolds-based asset manager Evenlode’s successful investment process across a broader, global universe of equity opportunities.

The £544.37m portfolio would suit a long-term investor seeking a high level of income combined with the prospect of some capital growth. A focused portfolio of quality global stocks – 38 names at last count – Evenlode Global Income aims to deliver sustainable real dividend growth over time, compensating for a modest current yield.

The emphasis on sustainable real dividend growth, through a focus on companies with high returns on capital and strong free cash flow, lends the fund resilience during periods of market volatility. Peters and Elliott put money to work in companies with diverse multi-national revenue streams.

Leading positions span the likes of Marmite maker Unilever (ULVR) and Schwarzkopf shampoo maker Henkel to computer chip maker Intel, publishing play RELX (REL), global foods and beverages behemoth giant PepsiCo and the Dutch digital information and services conglomerate Wolters Kluwer. Since launch, the fund has outperformed both the IA Global Equity Income sector and the MSCI World benchmark.

TROY Trojan Income (BZ6CQ17)

106.9p. Yield: 4.1%. Five-year annualised returns: 7.5%

Source: Citywire, Morningstar

A steady, reliable income fund for those in retirement

For those in the know, the Troy Trojan Income (BZ6CQ17) fund has long been a steady and reliable option with a decent dividend yield, low volatility and solid, if unspectacular, capital growth. Launched in 2004, the fund is entrusted with £3.2bn of investors’ hard-earned money, which it puts into high quality FTSE 100 companies with the potential to grow their dividends.

The large cap nature of the portfolio, combined with the management team’s focus on capital preservation, means the fund has consistently performed better than most of its peers for standard deviation and maximum drawdown, two useful measures for volatility.

Over five years, the fund has a standard deviation – the difference in performance compared to its peer group – of 8.6. Anything below 10 is considered to be low volatility. Over the same time period, the fund has a max drawdown – the difference between its highest value and lowest value – of just -9.1%, demonstrating the reliability of its returns so far.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.