Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineHow are sin stocks stacking up?

As the environmental, social and governance (ESG) juggernaut has rolled on, forcing institutional investors to put more and more money into companies with the best socially-responsible credentials, old-fashioned ‘sin’ sectors such as alcohol, tobacco and gaming have fallen out of favour.

Yet given their relative resilience when the global economy slows, which it is likely to do at some point, is it time to re-appraise these deeply unfashionable sectors?

TO ESG OR NOT ESG?

Long before ESG became the must-have strategy, investors wanting to side with the angels and buy with a clear conscience would typically avoid ‘sin’ stocks despite the fact that they tended to have fairly dependable cash-flows and dividend streams.

As the head of responsible investing at Norway’s largest pension fund put it, ‘we need energy, but we don’t need tobacco’. With energy there is a choice between fossil fuels and renewables. With tobacco, for now there really isn’t a similar choice.

Yet, without making predictions about the direction of the market or the UK economy, it’s well known that defensive sectors such as alcohol and tobacco outperform when fears of a slowdown arise due to the fact that consumption of booze and cigarettes tends not to be greatly impacted by economic cycles.

A DROP OF THE HARD STUFF

Alcohol producers are the obvious targets when looking for ‘sin’ stocks in the beverages space, as soft-drink makers have already fallen into line in the fight against obesity by re-formulating their drinks.

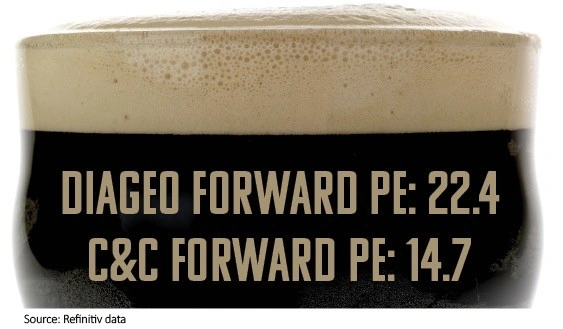

The biggest constituent in the sector is Diageo (DGE), owner of iconic spirits brands such as Smirnoff, Johnnie Walker, Tanqueray and Baileys, as well as the world’s leading stout, Guinness.

From the start of 2017 to the end of September this year when the shares hit £36 it had rewarded investors with an 80% total return including dividends.

The shares have since dropped to £31, which still values the firm at more than £70bn against net sales of less than £13bn and pre-tax profits of £4.2bn for the year to June, so they can hardly be described as cheap.

However, joining the FTSE 350 at the end of this year with luck is Irish beverages group C&C (CCR), famous for its Bullmers and Magners cider brands.

Following the acquisition of Matthew Clark and Bibendum in 2018, most of C&C’s revenues and profits come from the UK rather than Ireland hence its decision to de-list in Dublin and seek admission to the FTSE.

C&C has a lower profit margin than Diageo, which explains why it trades on a lower price to earnings ratio. Its market capitalisation is €1.4bn with annual sales of around €1.7bn and pre-tax profit of around €80m last year, expected to rise to €100m this year.

RUNNING OUT OF PUFF?

Another classic ‘sin’ sector is tobacco. Despite falling consumption, cigarette producers have been able to increase their revenue through a combination of higher prices and a higher value-added product mix.

In its full year results published earlier this month, Imperial Brands (IMB) reported a 4.4% drop in cigarette volumes but a price/product mix improvement of 5.5% leading to net tobacco revenue growth of 1.1%.

Rival British American Tobacco (BATS) registered a 3.5% drop in cigarette volumes and a 7% increase in price/product mix in its half-year report, published in August.

However new research from Morgan Stanley suggests that tobacco firms’ pricing power is waning while volume trends are worsening.

In a survey of 3,000 smokers across five European countries, its analysts found that unfavourable demographic trends (fewer young people taking up smoking) and rising price elasticity (customer resistance to rising prices, resulting in trading down), together with a rising preference for reduced-risk products (such as vaping), are likely to put pressure on the profits of major cigarette producers.

Europe is ‘key to earnings for global tobacco, contributing over $13bn in combined operating profit for Philip Morris International, BAT, Japan Tobacco and Imperial Brands in 2018, or 18-50% of total profits’ according to the analysis.

Both firms have pinned their hopes on new generation products (NGP), with BAT opting for tobacco-heating product (THP) technology and Imperial betting on vaping. However official opposition to vaping is spreading around the globe, which suggests that Imperial may have an uphill battle on its hands.

BETTING ON US GROWTH

Gambling and betting firms are most definitely ‘sin’ stocks, and up until six months ago they were very much out of favour. However, with the impact of the clampdown on fixed-odds betting terminals now receding, and a softening in US online gambling regulation with the PASCA act, they are back to winning ways.

The UK gambling sector turned over around £16bn last year, which isn’t bad going but equates to less than 5% of the global market. The golden goose is the US, where UK firms have tried before and failed to make a meaningful impact.

However, the US market is creating what GVC (GVC) believes is the biggest sports-betting opportunity in 20 years. Americans watch 36bn hours of sport a year, with 37 networks offering coverage of more than 10,000 different events.

As more states allow online sports betting, market intelligence firm Gambling Compliance believes that within four years revenue could grow by $5.7bn, putting the US second behind China in terms of market size even without California, Florida or Texas opening their markets.

Less positively, in the UK a cross-party group of politicians focused on gambling-related harm has proposed reducing the limit on online slot machines to £2 in line with the in-store terminals.

Gambling consultancy Regulus Partners estimates that the sector as a whole could see its revenue impacted by between 5% and 10% while slot-led gaming operators could see up to 30% of their revenues disappear if the proposal were to be made law.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.