Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineUS stocks need to deliver strong second quarter earnings

As America celebrates Independence Day, investors with exposure to US equities will be looking for fireworks of a different kind from the imminent second-quarter reporting season.

The latest round of financial updates and – perhaps more importantly – outlook statements will begin in earnest on Monday 11 July when megabank Citigroup will unveil its results for the April to June period.

A trickle of data will then become a deluge as 57 S&P 500 index constituents report during the week that begins 11 July and 167 more in the following working week and it may be that forward guidance for the remainder of the year matters more than the Q2 numbers themselves.

This is because so many companies and analysts are talking about a ‘second-half recovery’ to justify estimates. Earnings growth is expected to be no better than low single-digit, in percentage terms, through to September before a 26% year-on-year surge in the final quarter of the year.

For the moment it is hard to quite see where that could come from, without a marked surge in global economic activity, and the danger is that disappointment starts to creep in and erode the healthy gains made in US equities by investors, just as happened in 2018.

DON'T LOOK BACK IN ANGER

The first quarter reporting season exceeded expectations. According to data from S&P Dow Jones, 371 of the S&P 500 index’s constituents beat earnings forecasts while just 95 undershot them and the rest lived up to their billing.

That meant that overall earnings for the S&P 500 benchmark rose by 4% year-on-year. That might not sound like much (and frankly it isn’t much) but it did at least mean that the ‘worst case’ of an actual drop in profits was avoided.

This upside surprise, coupled with hopes for some kind of trade agreement between China and America and the US Federal Reserve’s apparent new-found enthusiasm for interest rate cuts, is one reason why the S&P 500 is now bearing down on a new-all time high and the 3,000 threshold.

The question now is whether earnings momentum can remain strong enough to keep US stocks at these lofty levels or indeed take them higher.

LOW BASE

Helpfully, expectations are at least low – and keep getting lower.

The good news is this sets a low bar for expectations and sets the scene for the ‘earnings beat’ which can juice share prices, at least in the short term.

However, it does create a challenge for the longer term.

Since 1 January 2018 the S&P 500 has risen by 10%, even though 2019 estimates have sagged by 5%. What that means, therefore, is the S&P 500 has gone up because of multiple expansion (the ‘P’ in the price/earnings ratio) and not earnings (the ‘E’).

Consensus earnings forecasts now put the US stock market on 17.9 times forward earnings per share estimates for 2019 and 15.9 times for 2020, based on the premise that earnings will rise by 9% this year and 12% next.

Bulls will argue that those earnings forecasts are perfectly achievable, especially if he US economy can meet President Trump’s target of 3% GDP growth a year, a trade deal is hammered out with China, the Fed cuts rates (reducing interest bills on debt) and US corporations add in a little financial alchemy in the form of yet more share buybacks. From such a perspective, US stocks do not look unduly expensive relative to their history, especially if earnings estimates start to creep higher, not lower.

Bears will challenge that 9% growth estimate by pointing out that the forecast 2019 earnings per share figure for the S&P 500 of $165 already represents a record high. With corporate profit margins also near record highs, there has to be a risk that those margins come under pressure, with unemployment low, wages ticking higher, the dollar still strong and tariffs on imports potentially placing further costs on supply chains and consumers.

MARGIN OF SAFETY

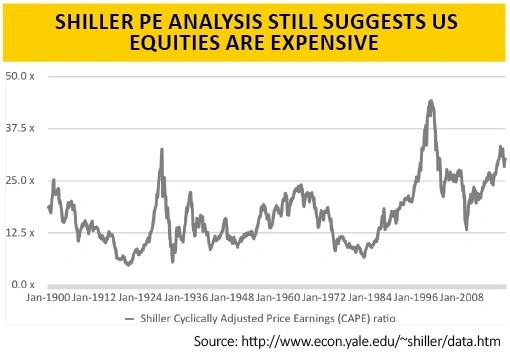

A different valuation methodology also suggests the risks may be greater than they seem. Professor Robert Shiller’s cyclically-adjusted price/earnings ratio (CAPE) calculation, which is based on inflation-adjusted historic earnings on a ten-year rolling basis, still argues that US stocks may be overvalued, at 30 times forward earnings.

The S&P 500 reached a CAPE rating of around 30 times on two prior occasions, in 1929 and 1998-2000, and neither of those episodes ended well for owners of US stocks.

Others will argue the CAPE indicator has been calling out US stocks as dangerously expensive for several years, to no great effect. This looks like a perfectly fair comment, given how US equities continue to not just go up but outperform on the global stage, but American stocks are riding positive earnings momentum. The situation would look a lot less rosy were earnings estimates to keep falling and profits to stop growing or start shrinking.

This is why the July reporting season is so important, as the outlook statements will shape estimates for the second half and beyond.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.