Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhat are preference shares and should you buy them?

A little understood part of the market, preference shares could be worth a look for some investors. A hybrid financial instrument with characteristics of both equities and bonds, they might appeal to older investors looking for a steady and reliable yield.

WHAT ARE PREFERENCE SHARES?

There are two types of shares you can own in a company: preference shares (also called preferred stock) and ordinary shares (also called common stock). While they both give you a stake in a business, preference shares give you the extra rights of a preferred shareholder.

This means you are at the front of the queue for dividend payments: companies can’t pay their ordinary dividends until they have paid dividends to their preferred shareholders. Preference share dividends are fixed at a certain level, and usually paid twice a year but, because they are fixed, you can’t get a share of excess profits above that pre-determined rate.

You’ll also be first in line for a claim on assets in the event a company goes bust. However, preference shares don’t give you voting rights, so you won’t have a say in how the company is run. But you can choose to hold convertible preference shares, which convert into ordinary shares. The other option is redeemable preference shares, where the initial investment is repaid.

Preference shares can be cumulative or non-cumulative. If the latter, and the issuer misses a dividend payment, you can’t claim the dividend in the future. This makes cumulative preference shares worth more than non-cumulative versions.

You pay income tax on any dividends you earn from preference shares outside of the dividend allowance.

‘In the capital structure a preference share is the next down from equity, it is more akin to equity than a bond as it pays dividends not interest,’ says Chris Burgoyne, director of fixed interest at Canaccord Genuity. ‘As such, dividends that fall within the £2,000 dividend allowance are tax free and any dividends in excess of this figure are taxed according to the income tax band you fall into.’

Preference shares are issued primarily by banks and other financial institutions, and were originally intended as a way to raise capital without diluting value for their ordinary shareholders. But they were an expensive way for companies to raise money given their high coupons and the fact they were not-tax deductible.

They are being phased out as a form of tier one (core) capital by 2026, so this may reduce the size of the market in future. ‘Given they will no longer serve the purpose for which issuers originally intended, the preference share market has been shrinking over time,’ adds Burgoyne.

WHY BUY PREFERENCE SHARES?

Although they are technically equities, preference shares offer a yield similar to that of a high yield bond, but with typically lower credit risk and volatility.

Preference shares yields are decent, on average about 6% in the current environment, and this makes them attractive to retirees and those looking to generate stable income from their portfolios over the long term without taking on too much risk.

WHAT ARE THE DOWNSIDES?

While the capital value of preference shares can go up and down depending on how well a company is doing, the fixed dividend means you don’t benefit from as much share price upside as if you held ordinary shares. Burgoyne explains: ‘Dividends on the equity can grow as the profitability of the company grows, so your capital growth is uncapped on the equity whereas, if you buy the preference shares, the price goes up, the yield goes down and they become less appealing because the upside is capped. For example, Lloyds (LLOY) preference shares yield more than their corresponding equity at the moment but you won’t enjoy as much capital growth.’

There’s also a small risk the issuer could cancel its preference shares to reduce its debt pile – in 2018 Aviva (AV.) threatened to do just that before backtracking in the face of shareholder ire, but not before causing a big sell-off in preference shares market-wide. Aviva argued that technically it would have been within its rights to cancel the shares, which holders had thought irredeemable, so investors should beware of other issuers taking the same stance in future.

HOW TO BUY PREFERENCE SHARES

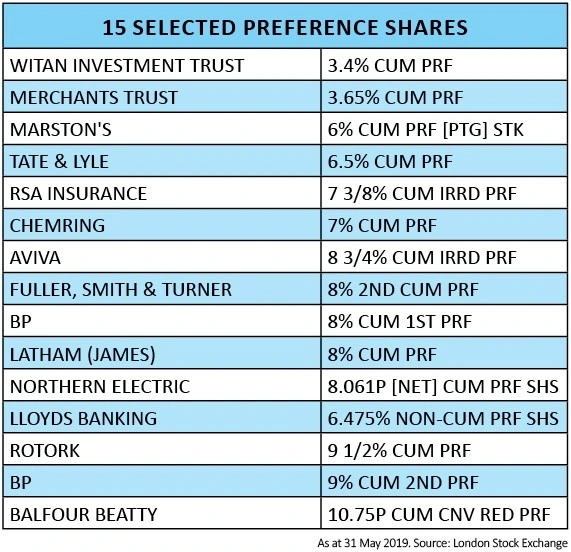

Individual preference shares are issued by UK companies such as Tate & Lyle (TATE), Marston’s (MARS), BP (BP.) and Aviva (AV.), and investment trusts such as Witan (WTAN), Brunner (BUT) and Merchants Trust (MRCH). You can buy these shares the same way you would buy any others, through a stockbroker or share dealing platform.

There are exchange-traded funds (ETFs) which hold preference shares, such as the Invesco Preferred Shares UCITS ETF (PFRD).

Some funds and investment trusts also hold them – Shires Income Trust (SHRS), for example, aims to generate a high income through a mix of UK equities and fixed income (around 30% of the portfolio) including preference shares and convertible bonds.

There’s also the £770m Janus Henderson Preference & Bond (0765172) fund which holds preference shares, government bonds and corporate bonds, although preference shares only accounted for around 2% of the portfolio as of 31 May.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.