Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineThe market alarm bell is ringing for the banks

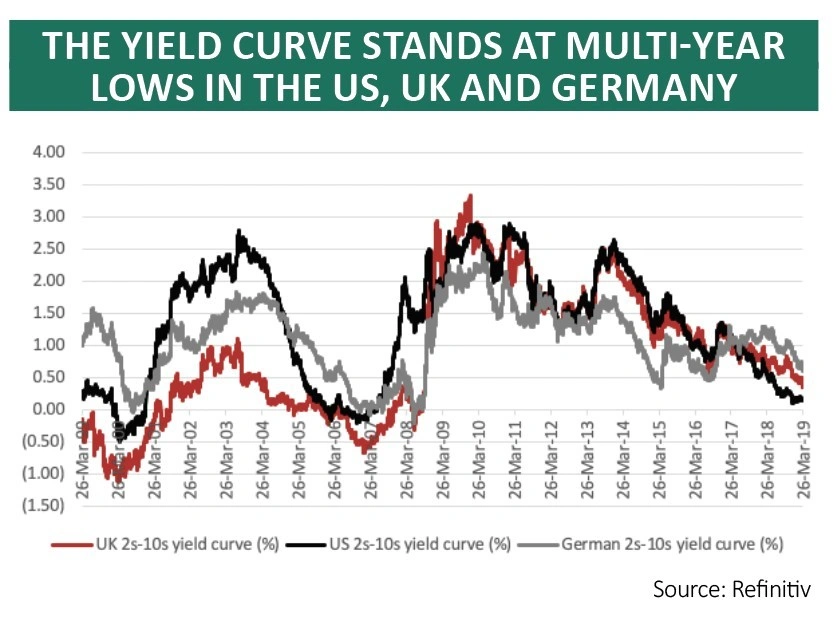

It may not have gone negative yet but the yield curve – as measured by the difference in the yield available on 10-year and two-year government bonds – is as at its lowest level since 2007 in the US, 2008 in the UK and 2016 in Germany.

Whether the yield curve is forecasting an economic slowdown or recession (accurately or not) or whether it is simply anticipating a fresh round of interest rate cuts and quantitative easing from nervous central banks remains open to debate.

But one thing does seem certain and that is banking stocks do not like what they are seeing from the yield curve.

Banking shares are doing badly not just in the UK but the US and Europe as well – and if there’s one sector that investors would like to know is in good health after their experiences of 2007-2009 it is the banks, so this is a trend that needs to be watched.

MIND THE GAP

The yield curve measures the difference between different maturities of government debt, with the gap between two-year and 10-year paper a common benchmark.

In theory, the yield on the 10-year should always be higher. This is simply because more things can go wrong in the life of a 10-year bond than in a two-year one. Investors will demand a higher yield as compensation for the higher risks, which, in the case of fixed-income, come in the form of default, interest rate movements and inflation.

But sometimes the gap between the 10-year and two-year government bond yields can narrow. This is often (though not always) because the yield on the 10-year falls quickly as markets price in an economic slowdown or recession. Central banks’ usual response is to cut interest rates in an attempt to boost the economy.

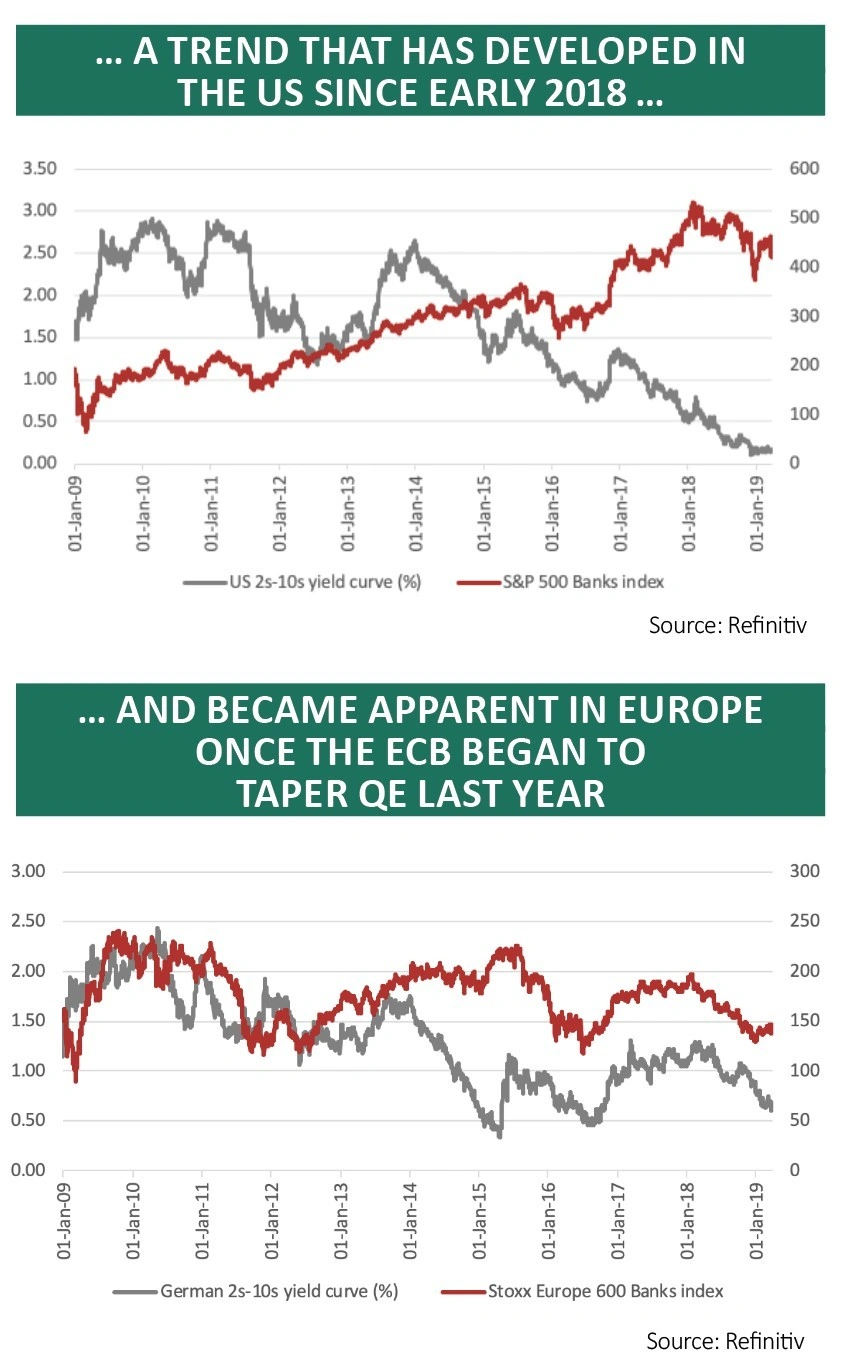

At the moment, the yield on 10-year Government Gilts in the UK, Treasuries in the US and Bunds in Germany is falling faster than the 2-year yield, to flatten the yield curve.

As a result, banking shares are starting to struggle on the UK, American and European stock exchanges.

The thinking behind this is that a flattening yield curve damages banks’ earnings power.

Banks tend to raise funds by borrowing in the short-term and lending over the long-term, in what it known as maturity transformation. The idea is that this enables them to borrow at a lower interest rate and lend money at a higher one, pocketing the difference as their profit – this is called their net interest margin.

THROWN A CURVEBALL

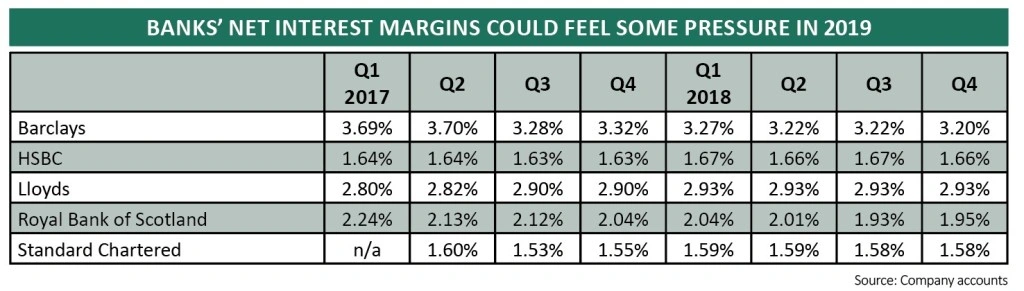

The problem now is that a flattening yield curve will be weighing on net interest margins. That will leave the banks relying on fees from any wealth management or private banking operations that they might have, or trading commissions and advisory fees from an investment bank, if they are brave and well capitalised enough to own one.

We can already see how the net interest margins at the UK’s Big Five banks have started to come under pressure, or least stop expanding, and one key test of April’s first-quarter results will be the trend here.

Downgrades to net interest margin expectations could well feed into cuts to earnings estimates and no matter how cheap a stock may look on book value, dividend yield or earnings it is generally pretty hard for it to perform, at least in the short-term, if profit forecast momentum is negative.

This does not have to mean the end of the equity bull market. But it is an unwelcome complication, especially for the UK, where banks are expected to make big contributions to profit and dividend growth in 2019 and beyond. It is also a potential warning to central banks that unorthodox policies can have unintended consequences.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.