Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

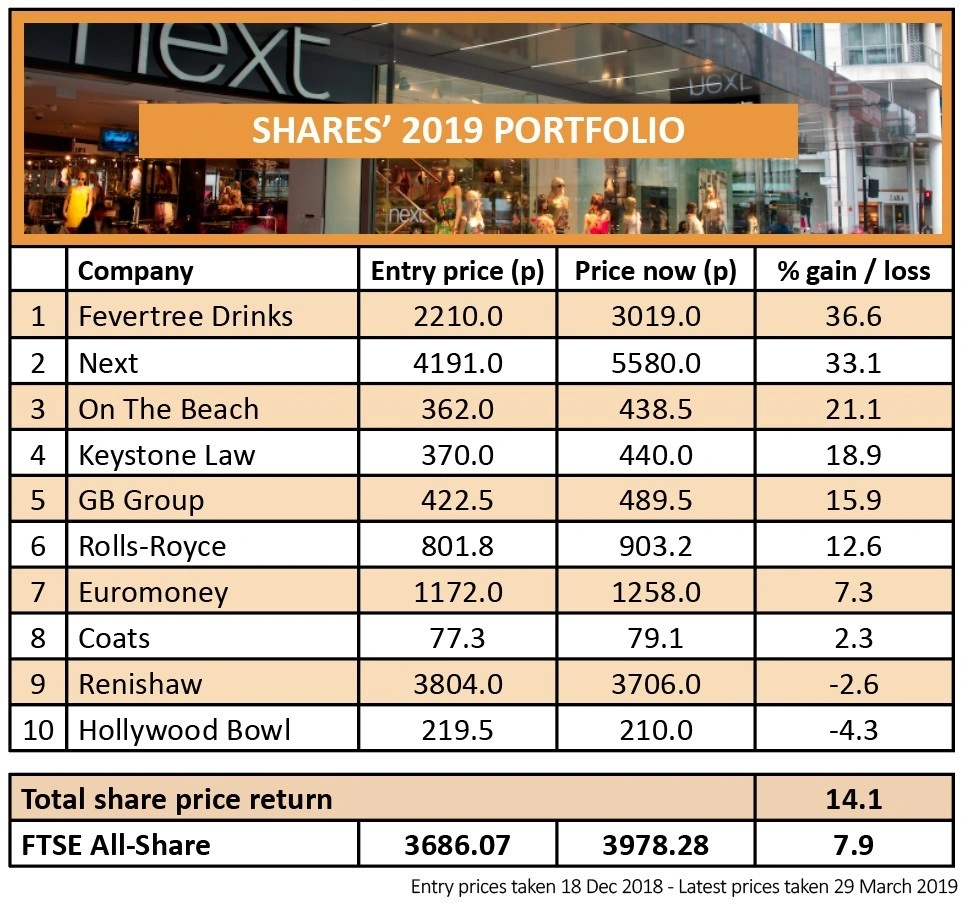

magazineNearly double the market return from our 2019 share portfolio

Our top picks of the year have got off to a great start with the portfolio up 14.1% versus 7.9% from the wider market.

We’ve only suffered one profit warning and only two of the 10 stocks are in negative territory. Six of the stocks have delivered double-digit gains, so hopefully you are sharing our success with your own portfolio.

The best performer is Fevertree Drinks (FEVR:AIM), up 36.9% after a really good trading update earlier this year was followed up by a solid set of full-year results on 26 March.

Pre-tax profit increased by a third to £75.6m and the dividend was lifted by 36% to 14.5p. Impressively, net cash at year-end jumped to £83.6m from £50.9m a year earlier.

While it looks like growth could be harder to achieve in the UK, where it already has a solid market position, the US roll-out is going well and the business remains confident about cracking that geographic territory.

Fevertree is also investing in Europe whose mixer market is three times as big as the UK, says Investec analyst Nicola Mallard.

RETAIL BOUNCES BACK

The retail sector has put on an impressive performance this year and Next (NXT) has proved to be one of the most resilient companies in the sector. Its share price has been on a real tear since issuing its post-Christmas trading statement on 3 January and full year results on 21 March.

‘Next is well-managed with an experienced management team and tight stock and cost control,’ says Shore Capital analyst Greg Lawless.

Holiday seller On The Beach (OTB) has also done well in recent months, rising 21.1% in value to 438.5p. We are now slightly cautious on this stock because several tour operators have issued profit warnings and various airlines are talking about soft ticket prices due to weaker demand. However, we’re sticking with the trade for now.

Brexit uncertainty is weighing on consumers’ minds and it looks like many people are holding off from buying a holiday until they are sure that airlines are still allowed to fly in the EU and there won’t be large delays at airports.

On The Beach last updated on trading in February where it said everything was going well. We note that its shares haven’t been weak in recent months despite negativity in its sector, so the market is optimistic about its fortunes. The next scheduled announcement is 14 May when it publishes half year results.

Keystone Law (KEYS:AIM) issues its full year results on 8 May and has already told the market it expects to report profits ahead of market expectations.

GB EXPANDS THROUGH ACQUISITION

You would have made more than twice as much as a FTSE All-Share tracker fund by investing in GB Group (GBG:AIM) when we said to buy last December. While the data intelligence firm hasn’t updated on trading in the past quarter, it has acquired an identity verification business called IDology which is expected to enhance group earnings over the next year.

Engineer Rolls-Royce (RR.) is up 12.6% since we said to buy the shares. Full year results in February revealed improvements to both profit and free cash flow.

We recently explained why shares in threads manufacturer Coats (COA) had taken a hit, principally around one-off costs.

Share weakness should be seen as an opportunity to buy more stock in this fantastic company which has a long history of generating solid returns from the money it invests in its business.

ONLY TWO LOSING TRADES

Two stocks from our portfolio of 10 are currently in negative territory, although only by a very small amount. Precision engineer Renishaw (RSW) is down 2.6% following an Asia-linked consumer electronics profit warning. We’re inclined to hold on to the shares as the business still has numerous attractive qualities.

‘Consumer electronics is not the sole, or even most important, market for Renishaw,’ says Investec analyst Michael Blogg. ‘Its technology and product portfolio offers much that is of interest to manufacturers – of aero-engines, auto assemblies and medical prosthetics – and its vertically-integrated model gives it plenty of insight into their challenges.

‘Precise measurement and automation enable customers to develop more refined and efficient (and therefore differentiated) products and to make them more cost-effectively.’

Down 4.3% is tenpin bowling centre operator Hollywood Bowl (BOWL). We expect a trading update very soon and for the company to say it is business as usual.

EUROMONEY’S FRESH START

And finally we have Euromoney (ERM) which is slightly lagging the market albeit still generating a 7.3% positive return since we said to buy. Its big news is that Daily Mail & General Trust (DMGT) has given its 49% stake in the media group to its shareholders.

Peel Hunt analyst Malcolm Morgan says this is important for two reasons. First, it means Euromoney’s board will no longer have a DMGT representative. Second, he expects Euromoney to vigorously pursue acquisitions, potentially funded by issuing new shares.

‘Any such transaction will no longer be pre-vetted and cornerstoned by the dominant shareholder. Bigger transactions could now be more readily contemplated and easily delivered as the deal need to serve institutional needs rather than the requirements of a publisher with more limited capital resources,’ says Morgan.

While that sounds exciting, we have to consider that DMGT shareholders may not want to keep the Euromoney shares they’ve just been given and so the latter’s share price could be volatile in the near-term if people are selling out.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.