Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineEmpire building: Why does Mike Ashley want to own so many retailers?

Billionaire Mike Ashley has become quite a character in the business world. He has developed a reputation for being attracted to struggling companies with the aim of buying stakes in them while they are going cheap, just like the general public hitting the shops in search of a bargain.

Ashley’s acquisition vehicle is Sports Direct International (SPD), where he holds sway as chief executive and personally owns a 61.45% stake through his Mash Beta and Mash Holdings vehicles. He also owns Newcastle United Football Club, to the chagrin of the ‘Toon Army’.

Given the well-documented challenges facing the retail industry – weak consumer confidence, rising costs, Brexit uncertainty, online channel shift – investors are asking if there is any method to the ‘madness’ of hoovering up high street assets?

INVESTING IN OTHER LISTED COMPANIES

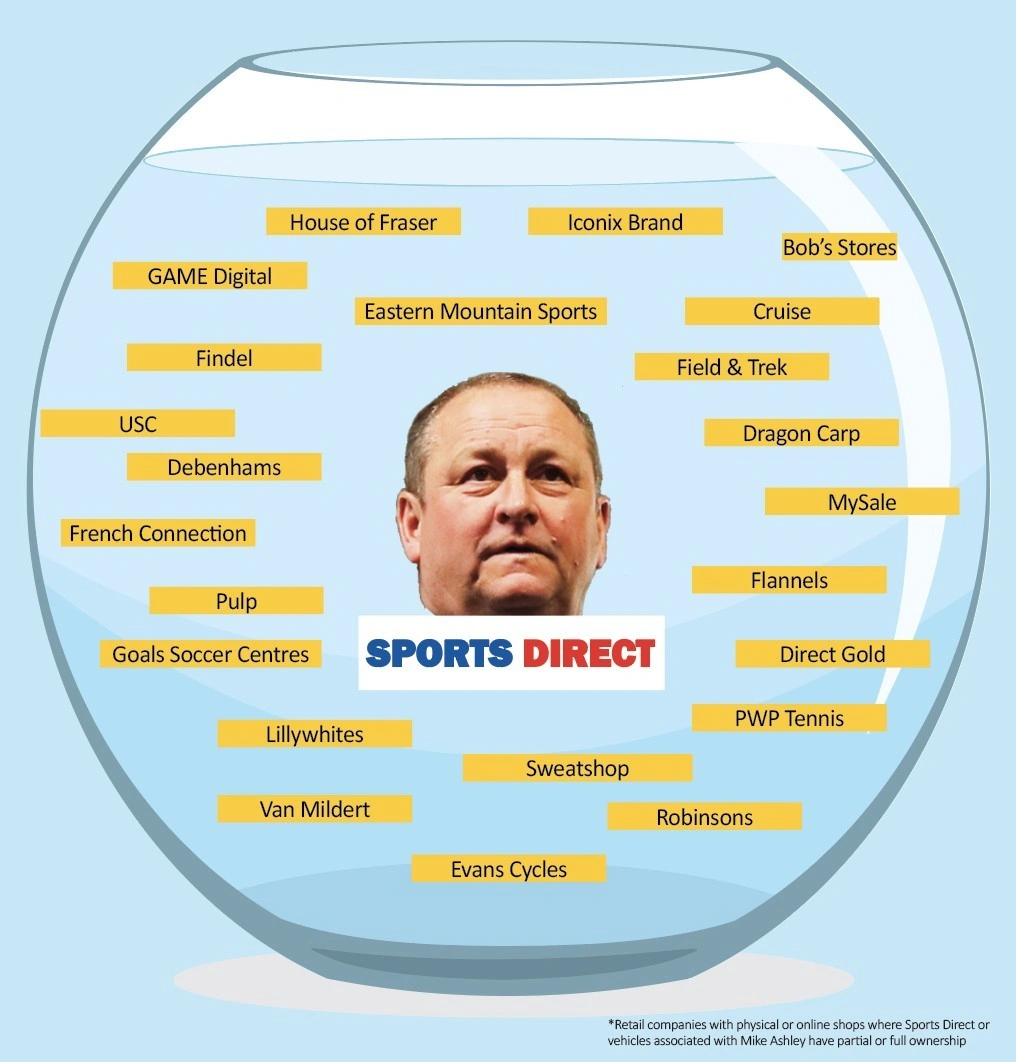

Ashley has amassed a retail empire that includes House of Fraser and high-end clothing outfit Flannels, as well as sizeable stakes in various companies on the stock market including GAME Digital (GMD), French Connection (FCCN) and Findel (FDL).

In recent years Sports Direct has saved House of Fraser from collapse with a £90m rescue, as well as buying Evans Cycles and Agent Provocateur from administration.

The highest profile chase has been Sports Direct’s desire to gain control of Debenhams (DEB), where it is the largest shareholder with a near-30% stake.

Financial motivation aside, Ashley’s House of Fraser rescue and attempt to support Debenhams have also been driven by a desire to help the overall reputation of Sports Direct.

Attempts to add HMV and Patisserie Valerie to the Ashley stable have fallen flat, although magic Mike continues to have plenty more targets such as LK Bennett, according to media reports.

THE FIGHT FOR DEBENHAMS

Sports Direct recently announced a possible £61.4m offer for Debenhams with Ashley also offering to assist the embattled retailer ‘in addressing its immediate funding requirements’.

However, his bid to bag Debenhams and possibly merge it with rival House of Fraser has seemingly been scuppered.

Debenhams’ bondholders have agreed to change the terms of some of their bonds, so that the retailer can secure new loans of up to £200m from existing lenders in a refinancing likely to wipe out shareholders, Ashley included.

EUROPEAN RETAIL EMPIRES

Examples of European fashion empires include the Arnault family-controlled LVMH and the rival Pinault family-owned Kering.

LVMH owns, among others, the Bulgari, Christian Dior, Givenchy, Hennessy, Kenzo, Louis Vuitton, Moet & Chandon and TAG Heuer brands in an empire covering leather goods, champagne, cosmetics, watches and jewellery.

The Arnault family owns more than 40% of the shares both directly and through its Paris-listed Christian Dior holding company to ensure control of the business.

Kering owns the Alexander McQueen, Balenciaga, Gucci and St Laurent luxury fashion brands as well as producing leather goods, jewellery and watches and like LVMH is controlled by a more than 40% family holding.

The use of holding companies is typical among wealthy families in Europe with the Agnelli dynasty, owners of the Fiat car and Ferrari luxury sports car brands, controlling their assets through their majority-controlled Exor investment vehicle based in the Netherlands.

WHAT IS HE UP TO?

In bidding for and buying this raft of struggling retailers, companies, landlords and investors are desperate to know exactly what Ashley is up to. There is a fine line between genius and madness.

Ashley built Sports Direct from a single store in 1982 into the UK’s biggest sporting goods retailer by revenue with tentacles extending overseas.

One investment trust manager describes Ashley to Shares as ‘a typical swashbuckling entrepreneur’ and ‘a retail genius’.

City detractors dislike his poor corporate governance and argue he is taking massive risks that could see his empire come crashing down, with one fund manager (who wished to remain anonymous) informing Shares that ‘I think he has lost his marbles in a way’ following his recent spate of investments.

THE ASHLEY PLAN

When Ashley picks up stores from the administrators, the skilled trader gets the stock for next-to-nothing, inventory that he can then shift at big discounts for a quick profit by selling it through his raft of retail chains and websites.

He also acquires store chains out of administration free of debt and with no pension liabilities.

In addition, Ashley’s increased grip on the high street is strengthening his bargaining power with landlords that already have lots of square feet of physical stores relying on Sports Direct for rent.

As the anonymous fund manager adds: ‘Retail is what he knows, so if he can stir up the landlords by taking these freeholds, he has better leverage for the core Sports Direct chain estate to get rent reductions.’

GROWING EMPIRE

Ashley’s sprawling empire also spans the Lillywhites sporting shop as well as a range of sporting brands including Slazenger, Lonsdale, Everlast, Karrimor and Kangol, labels bringing exposure to different types of shoppers.

And he has also invested in online operators such Findel and MySale (MYSL:AIM), thereby increasing the distribution channels for his wares.

By assembling diverse retail brands, Ashley has the option of creating mini-department stores on the high street with multiple brands under one roof.

Critics say there isn’t an overarching strategy, merely deal-by-deal opportunism with Ashley unable to resist steaming into strugglers, slashing costs and closing stores.

Other detractors suggest his ego is the driving force; Ashley is buying these chains and brands because he wants to be the man who saves the high street, a theory lent credence by his claim he’ll transform House of Fraser into the ‘Harrods of the high street’.

What is beyond dispute is that Ashley is one of the few entrepreneurs with the cash, confidence and contrarian ethos to hoover up high street assets in this way.

SPORTS DIRECT’S VIEW OF ITS STRATEGIC INVESTMENTS

Here’s what Sports Direct says about its strategic stakes: ‘Strategic investments are an integral part of the group’s overall strategy. Against a backdrop of a challenged retail market, we believe innovative strategic partnerships will help to differentiate our offer and enhance the consumer experience.

‘We look for ways to extend our reach into new retail channels and geographies, as well as selectively grow our market share. We maintain an active dialogue with the management teams of each of our investments, continually looking to explore new ways of working together. Given the breadth of our business, the strategic benefits can be varied and extensive.’

In the six months to 28 October 2018, Sports Direct recognised a seismic £76.7m of value reductions relating to Debenhams and other poorly-performing investments. Yet while stakes in Debenhams and others have been losing trades, other strategic interests have been more successful.

Last year, major rival JD Sports Fashion (JD.) took over NASDAQ-traded footwear seller The Finish Line, in which Sports Direct held a 19.3% stake, for almost £400m, generating a £45.2m windfall for Ashley.

Earlier this month, JD Sports put its struggling competitor Footasylum (FOOT:AIM) out of its misery with a £90m takeover offer. A month earlier, the Peter Cowgill-guided JD Sports acquired an 18.7% strategic stake in Footasylum, perhaps in order to block the deal-hungry Ashley from taking a stab at the business.

THE ASHLEY EMPIRE*

Iconix Brand

Sports Direct has an 8.29% stake in Iconix Brand, the New York-based company with dozens of brands including Candie’s, Bongo, Danskin, Joe Boxer, Rampage, London Fog, Mossimo, Pony and Starter as well as Rocawear/Roc Nation.

Debenhams (DEB)

Sports Direct is the biggest shareholder in the structurally-challenged department store with a 29.9% stake, although Ashley’s bid to wrest control appears to have been thwarted at the time of writing.

House of Fraser

Hours after House of Fraser announced it was seeking administrators last summer, Ashley agreed to buy the business for £90m. Since then, he’s been trying to get the troubled store back on its feet as online shopping continues to grow and his Debenhams bid sparked speculation he wants to merge these rival chains.

GAME Digital (GMD)

Sports Direct has a 29.89% stake in the video games seller, expanding the latter’s BELONG e-sports arenas which bring video-gaming to high streets and shopping centres. In February 2018, GAME and Sports Direct inked a collaboration deal which has the potential to accelerate the roll-out of BELONG through access to new locations including Sports Direct stores.

Jeroen Bos-managed Church House Deep Value Fund (B79XM02) is also an investor in GAME Digital. He says: ‘A perennial problem with retailers is that their store portfolio tends to be leased and these are then long term liabilities, not immediately apparent, when looking at the financial position. GAME Digital is in a very good position in that 70% of the stores have lease terms of 12 months or less.

‘This gives the company tremendous flexibility in being able to release those stores it no longer requires while it transitions to becoming a venue operator which require different property solutions.’

Bos says Sports Direct’s extensive retail property portfolio is a potential home for GAME Digital venues. ‘GAME Digital is concentrating on opening gaming venues where these games are played in store for an hourly charge. It is a business model that has shown very strong growth, albeit from a low base. Competitive gaming is a worldwide success story, and GAME Digital’s dominant position in the UK market should offer a good opportunity for this company to capitalise on this trend.’

French Connection (FCCN)

Sports Direct has a 26.7% stake in the faded fashion brand which returned to profit in the year ended 31 January 2019. French Connection has put itself up for sale and remains in talks ‘with a number of parties’ which we speculate to include Ashley and Sports Direct.

Findel (FDL)

Having increased its stake to 36.8%, Sports Direct has made a mandatory takeover offer for the online value retailer-to-education supplies outfit at 161p. Findel’s board has rejected the bid, insisting it significantly undervalues Findel and its future prospects.

Findel and Sports Direct had previously forged a commercial supply arrangement with the sporting goods giant supplying clothing to Findel’s Studio site.

Goals Soccer Centres (GOAL:AIM)

Sports Direct has an 18.92% stake in the troubled small-sided soccer pitch play, whose shares are currently suspended following revelations of accounting errors including an alarming VAT misdeclaration.

MySale (MYSL:AIM)

Sports Direct has a 4.8% stake in the international online retailer, having spotted the potential for collaboration opportunities in Australia and Asia, although the MySale share price has cratered following a number of punishing profit warnings.

Evans Cycles

The British cycling retailer collapsed into administration in October and Ashley bought the business for £8m in a pre-packaged deal from private equity firm ECI Partners.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.