Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineIs the US Federal Reserve stuck between a rock and a hard place?

As the central bank calibrates policy, pulling on levers such as interest rates and its unorthodox quantitative easing (QE) programmes, it is logical to assume that the US Federal Reserve is the lord of all that it surveys.

After all, one goal of record-low interest rates and QE was to inflate asset prices in an attempt to create a wealth effect. It has certainly succeeded, at least with regard to the first half of that mission, with the S&P 500 and Dow Jones Industrials stock averages sitting less than 5% from last year’s all-time highs.

But while the Fed has had success – in some eyes at least – with low rates and QE it is encountering greater difficulty in extricating itself from these supposedly temporary measures and taking monetary policy back to more ‘normal’ paths.

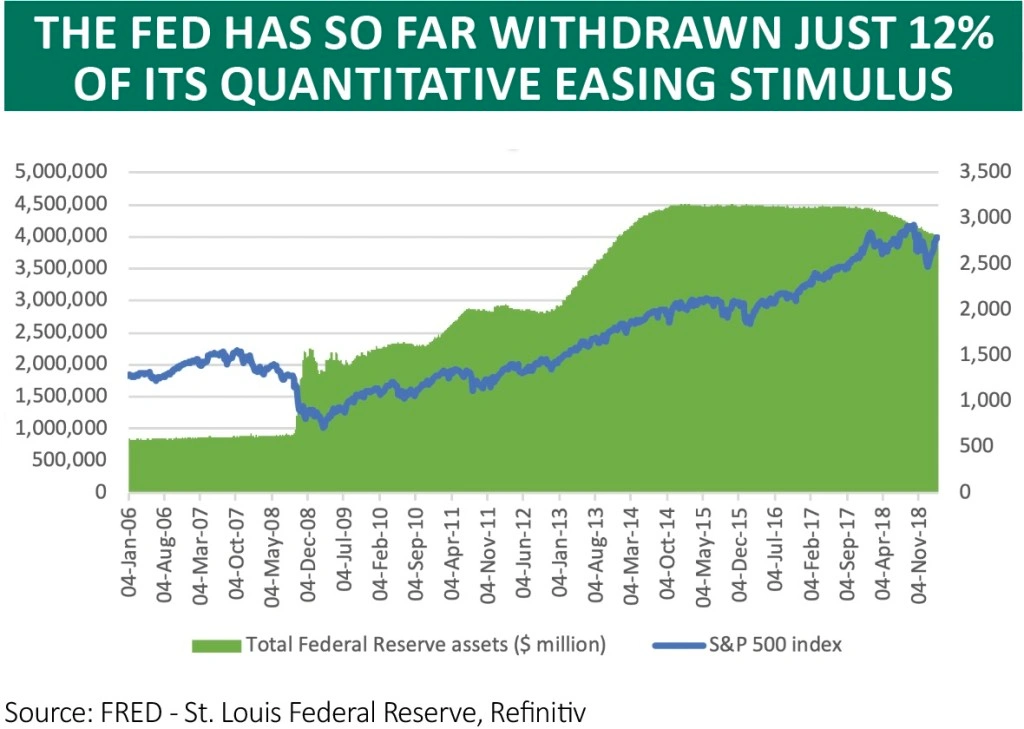

After a gradual series of nine interest rate rises over a three-year span from December 2015 and a 12%, $530bn shrinkage in its balance sheet the Fed has started to backtrack, putting rates on hold and hinting that it may end quantitative tightening this year.

The Fed has cited economic concerns – but with unemployment near 50-year lows, wage growth humming along above 3% and US President Donald Trump proclaiming an economic miracle in his State of the Union speech many will wonder why it is so concerned.

POLICY POSER

Perhaps the Fed has been shunted around by the financial markets which protested about the withdrawal of cheap and plentiful cash.

Share and bond prices wobbled badly in late 2018 – even though US interest rates reached just 2.5% compared to the 2006 peak of 5.25% and QE swelled the Fed’s balance sheet by $3.5trn or 350% – and it seems as if chair Jay Powell and his colleagues are backing off as a result.

One reason may be the swoon in US consumer confidence which accompanied last year’s stock market dip.

Consumer confidence, as measured by the Conference Board, has soared alongside the S&P 500 since the end of the global financial crisis in 2009 – something which says the Fed’s asset-price-promotion and wealth-creation policies have worked.

But as soon as the Fed tried to tighten policy, the US stock market wobbled and seemed to take consumer confidence with it, as even the FAANG companies tumbled briefly into bear market territory, with a drop in their aggregate market value that exceeded 20%.

PRISONER'S DILEMMA

Equally, stock prices – and consumer confidence – have surged again now that the Fed has begun to adopt a softer line.

This begs the question of who is in charge of whom? Is the Fed able to bend the markets to its will – even if Powell has said on several occasions that it was not the central bank’s job to stop people losing money on their investments – or are asset prices simply too integral to the US economy, thanks to the Fed’s wealth-creation plan, meaning that the markets are dictating policy to the Fed?

We may find out in the coming months but the launch of QE-II, Operation Twist and QE-III after stock market slides under the Ben Bernanke-led Federal Reserve would suggest the central bank is paying acute attention to stock prices, despite any denials to the contrary.

We could end up with a situation whereby a financial market wobble knocks consumer confidence and that in turn hits the US economy hard.

Equally, any pause (or reversal) in policy to avoid that scenario could conceivably prompt stock markets and other asset prices to start melting up once more, ironically in the wake of any Fed move to stop a meltdown.

That brings dangers all of its own and conceivably makes it harder for the central bank to tighten policy in the future.

This is a wretched position for Powell to inherit but it shows that even the US central bank is still finding out what may be the possible unintended consequences of a decade’s worth of unintended policy.

And remember that this policy’s main architect, Bernanke, did not envisage low interest rates and QE lasting for anywhere near this long when they were introduced in 2009, itself a sign that it is too early to declare whether they really did work or not.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- News on Vodafone, RELX, GoCompare and more over the past week

- A tale of two founders: Ted Baker and Superdry

- Smithson beats its benchmark in maiden set of results

- What happens next with Brexit and what could it mean for investors?

- New IMI boss hoping to use his Halma-earned growth magic

- Take advantage of price dip in manufacturer Coats