Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineTaking an income in retirement: how much should I withdraw a year?

Changes in 2015 to the way pensions could be accessed mean you no longer have to buy an annuity with your pension, thereby opening the door to a wide range of options for retirees, and some conundrums in how to invest.

You can still choose to buy an annuity to obtain a guaranteed income for life. But what are your choices if you reach retirement and want to keep your money invested? How do you know where to invest and how much income to take? This article offers some answers to these questions.

HOW MUCH INCOME CAN I TAKE EACH YEAR?

In order to work out what you should be invested in as you near retirement, you need to first work out how much income you want to take each year. Usually people base this on a percentage of their initial pension pot size.

The key is balancing the amount you take off in income each year with the amount the pot is growing each year or the amount of income it’s generating.

If you draw off more income and invest in lower-returning assets then you are likely to exhaust your pot more rapidly and be left with nothing. It’s a tricky balancing act.

You need to balance withdrawal targets with how much you think you’ll actually need to live on during retirement.

The answer largely depends on what lifestyle you plan to have in retirement, so how much travelling you plan to do, for example, and also your living situation – do you own a home mortgage-free or are you renting?

The general rule of thumb is that you need two-thirds of your working age income during retirement. This broadly assumes that you are paying no rent or mortgage. You need to tot up how much income you’ll get from other sources, such as the state pension, any defined benefit pensions, any rental properties and other investments you own.

SHOULD I KEEP ALL MY PENSION INVESTED IN THE MARKET?

Once you’ve decided on a withdrawal target, how can you make sure you pension pot delivers?

One option that some financial advisers recommend is to split your pension pot into two. You add up all the essential costs in your life, namely bills, food, transport and any housing costs, and you compare that figure to the state pension you’ll receive.

If there’s any shortfall you use some of your pension pot to buy an annuity that delivers that income.

This means your essentials are secured and the income you’ll take from the remainder of your pot is for all the fun stuff – holidays, entertainment, buying a new car, gifts for family, day trips etc.

Once you’ve determined what income you need to generate from you investments you can organise them and make sure you’re in the right assets.

DIVIDEND-PAYING INVESTMENTS

The general wisdom from many investors is that they need to invest in income-generating assets in order to be able to take their required money out each year. This means moving to funds focused on income and to dividend-yielding stocks.

This is certainly not a bad idea, particularly at a time when the FTSE 100, the UK’s main stock market index, is currently yielding more than 4%.

There are also various income-producing funds and investment trusts that have long-standing fund managers who have proven their worth over time. The UK equity income funds space is one of the most competitive with some of the highest-profile fund managers for a reason.

If you take this route you’ll need to target investments that have a similar yield to the one you’re hoping to draw off. If you’re aiming for 4% yield then that will leave you with a wealth of options, but if you’re aiming for 7% yield then you’ll find you need to invest in riskier assets and will have fewer to choose from.

One key factor when hunting out yield is to look for a payout that has grown over time. You don’t want to just be drawn to something that’s delivering high income today. Instead, you want to know that it can continue growing over time and ideally keep pace with inflation.

The Association of Investment Companies’ website has a helpful list of ‘dividend hero’ investment trusts – trusts that have increased their dividends for each of the past 20 years or more – which is a good place to start. This income approach means that you may invest in assets that sacrifice some capital growth for income, but if you invest in the right assets you could end up drawing off the natural income from your portfolio and leaving the pension pot untouched.

This is a great option if you aim to pass on your pension to future generations, or if you want to be able to take lump sums from your pension too.

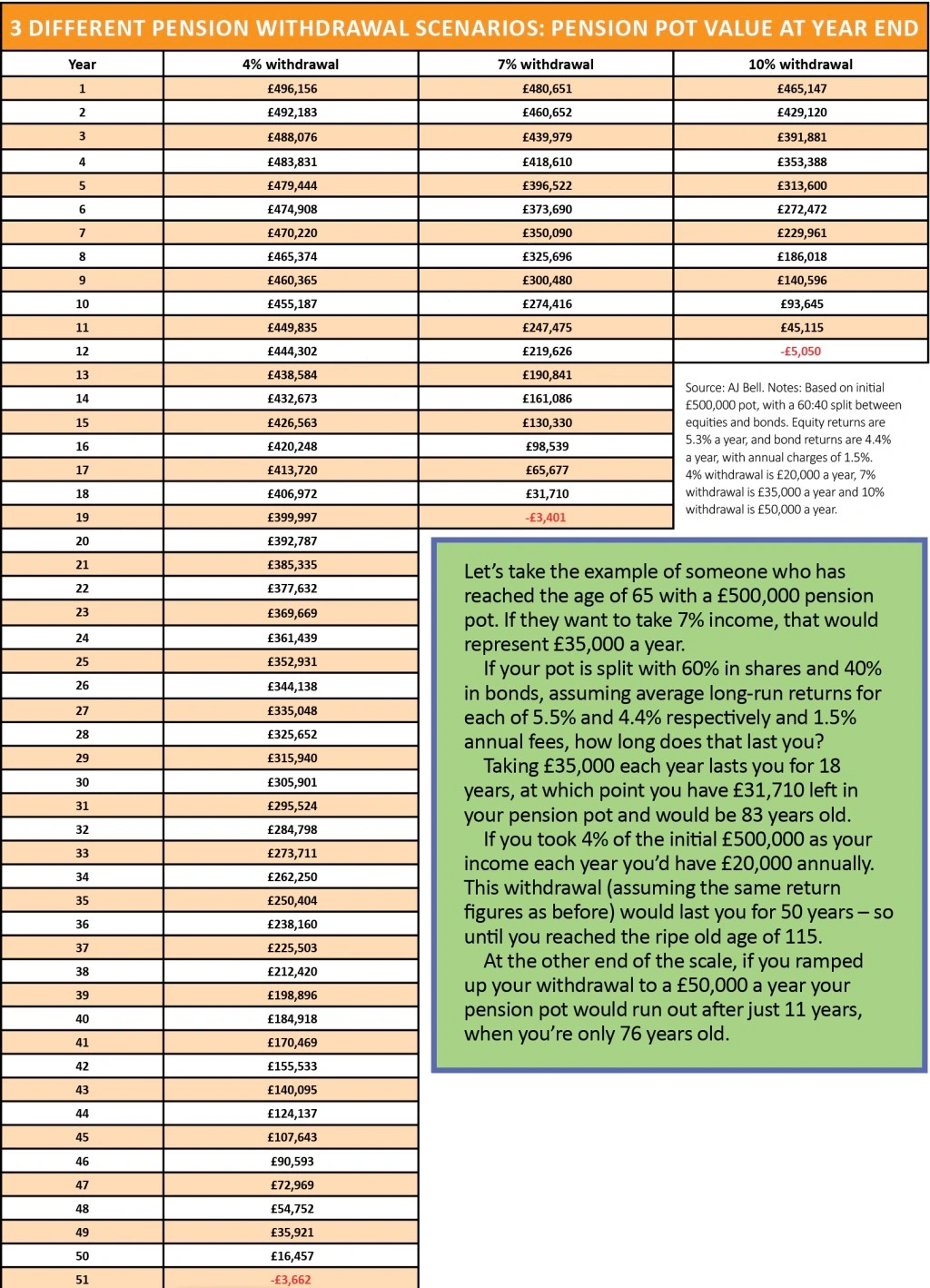

Let’s take the example of someone who has reached the age of 65 with a £500,000 pension pot. If they want to take 7% income, that would represent £35,000 a year.

If your pot is split with 60% in shares and 40% in bonds, assuming average long-run returns for each of 5.5% and 4.4% respectively and 1.5% annual fees, how long does that last you?

Taking £35,000 each year lasts you for 18 years, at which point you have £31,710 left in your pension pot and would be 83 years old.

If you took 4% of the initial £500,000 as your income each year you’d have £20,000 annually. This withdrawal (assuming the same return figures as before) would last you for 50 years – so until you reached the ripe old age of 115.

At the other end of the scale, if you ramped up your withdrawal to a £50,000 a year your pension pot would run out after just 11 years, when you’re only 76 years old.

OTHER STRATEGIES TO CONSIDER

However, this isn’t the only option. You could instead take a more holistic approach and just aim to maximise the growth on your investments, whether that’s capital growth or income and then take your income through a mixture of natural yield and selling units of funds or shares.

This means you’re not restricted to just focusing on income-producing assets and can get a mixture of different assets and of growth and income.

For example, if your portfolio generates 2% income and 5% capital growth you could draw off this income and then sell units or shares to take out that capital growth, in order to take your income.

A word of warning: if you’re selling shares or units of different funds you’ll incur higher charges than just drawing off natural income. When you sell a fund or share you incur transaction costs, and you’ll need to account for these in your calculations.

What is pound cost ravaging?

When markets fall, drawing a set income off your pension pot, regardless of what has happened to the value of it, can have disastrous effects. This process is known as ‘pound cost ravaging’ and is when assets that have fallen in price are sold to fund withdrawals.

When markets fall you need to sell more shares or units of a fund to generate the same level of income. This means you are leaving fewer assets to profit when markets rebound as you have effectively cashed in a larger lump of your savings at lower prices.

Therefore markets need to rebound by an even higher figure to restore your pot to sufficient levels to keep drawing off the same income.

In particular, if your pension suffers from bad investment returns in the early years this can have a long-lasting effect. Even good returns in future years might not be able to restore the balance because your pension has to work extra hard to recover from the initial loss.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- News on Vodafone, RELX, GoCompare and more over the past week

- A tale of two founders: Ted Baker and Superdry

- Smithson beats its benchmark in maiden set of results

- What happens next with Brexit and what could it mean for investors?

- New IMI boss hoping to use his Halma-earned growth magic

- Take advantage of price dip in manufacturer Coats