Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineThe psychology of stock market bubbles

The US investor John Templeton famously observed that bull markets ‘are born on pessimism, grow on scepticism, mature on optimism and die on euphoria’.

Indeed, by the final stages of a bull market many investors have come to believe that either they have some magic gift or that they are destined to make money from everything they touch.

In fact, all that is happening is that the market is going up, and by having money in the market they are profiting, nothing more.

Perhaps the best way to spot a bubble is identifying a certain topic everyone is talking about, such as cobalt last year – the price is down 40% this year.

COLLECTIVE WISDOM BEGETS COLLECTIVE MADNESS

There is a popular argument that collective wisdom is a force for good in business, economics and even society because together ‘the many’ are smarter than individual experts.

Where stock markets are concerned however, collective wisdom frequently morphs into collective mania and greed.

As the journalist Charles Mackay said, investors ‘go mad in herds’ and ‘only recover their senses slowly, one by one’.

Even the most rational investor finds it near-impossible to stand by and watch other people make money for what seems like little risk and no effort.

During the South Sea Bubble of the 1720s, no less a figure than Sir Isaac Newton was lured into playing the final stage of the bull market and lost a fortune.

Having doubled his money in the early stages of the bubble and sold out, Newton became swept up in the fever for South Sea shares and went back in at what turned out to be the very top.

Instead of keeping his £7,000 profit, he lost over £20,000 prompting him to rue that he could ‘calculate the motions of the heavenly bodies, but not the madness of the people’.

CONDEMNED TO REPEAT THE MISTAKES OF THE PAST

Investors have such short memories that in the decade since the financial crisis half a dozen new bubbles have been inflated in various asset classes.

Some have burst, while some are being sustained by ultra-low interest rates which are driving people to chase better returns than they can get on cash.

In early 2017 the price of crypto-currencies soared on speculation that one day they would come into widespread use as an alternative to cash.

From less than $950 at the start of 2017, the price of Bitcoin hit $17,500 by the end of the year. Today the price of Bitcoin is less than $4,000.

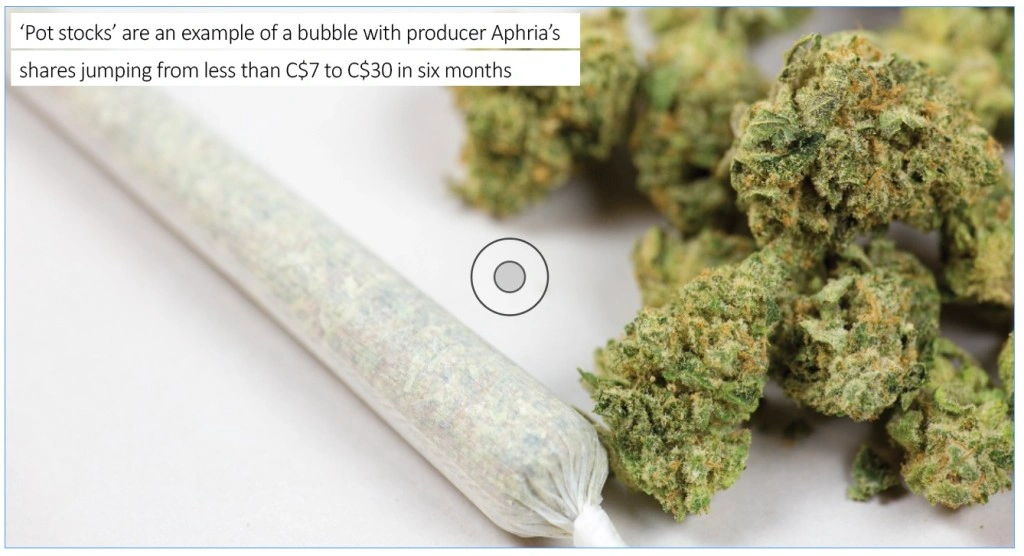

While the Bitcoin bubble was inflating, another bubble was developing in cannabis or ‘pot stocks’ on the premise that governments around the world would legalise its use for medicinal purposes.

Between July and December of 2017 shares in Canadian producer Aphria jumped from less than C$7 to C$30 per share.

Shares in rival producer Canopy Growth also rallied from below C$7 to C$30 over the same period but carried on to hit C$75 last October.

There was also a bubble in ‘low volatility’ of all things with traders bidding up the price of the XIV index – which paid the inverse of the VIX volatility index – by 2,200% over five years.

That bubble burst spectacularly last February when in a single day the VIX index doubled, causing the XIV to collapse and forcing the issuer, Credit Suisse, to shut the product down.

THERE’S ALWAYS A BUBBLE SOMEWHERE

Views differ as to whether the US market and in particular the ‘FAANG’ stocks (Facebook, Amazon, Apple, Netflix and Google/Alphabet) are in a bubble.

There is clearly a bubble in leveraged lending (effectively loaning cash to companies with bad credit ratings). This trend has drawn dire warnings from central banks and the International Monetary Fund.

Less than a decade on from the financial crisis there are new bubbles in residential property in Amsterdam, Hong Kong, London, Munich, Toronto and Vancouver, spurred on by low interest rates.

Fine art prices have soared since the crisis, with a growing number of works crossing the £10m threshold. Last year’s highest-priced work by an Old Master fetched £11.5m against its pre-sale estimate of ‘just’ £1.5m.

The fine wine market has also seen a resurgence of interest with first-growth Bordeaux leading prices higher and more 100-point ‘perfect’ scores awarded.

Last month, for the first time in Bordeaux history, four leading critics have given the same wine the perfect score – 2016 Mouton Rothschild, a snip at £600 per bottle after tax and duties.

Lastly, it’s debatable whether the bubble in classic car values has ever deflated. Prices for the most sought-after cars such as pre-1958 Ferraris barely blinked during the financial crisis and have more than doubled in the last decade.

Even fairly modern cars like 1980s and 1990s Porsches regularly command six figures today with prices up by 20% to 30% in the last year alone for certain models.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- News on Vodafone, RELX, GoCompare and more over the past week

- A tale of two founders: Ted Baker and Superdry

- Smithson beats its benchmark in maiden set of results

- What happens next with Brexit and what could it mean for investors?

- New IMI boss hoping to use his Halma-earned growth magic

- Take advantage of price dip in manufacturer Coats