Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWould the FTSE 100 be better equally weighted?

As investors we’re used to looking at the price of indices like the FTSE 100 fairly regularly but it probably never occurs to most of us how the index is constructed or how its value is calculated.

Like most indices, its value is calculated by taking the free

float London adjusted market value of all the companies within the index and dividing it by a number to get an index value.

When it was launched in 1984 the base value for the FTSE 100 was 1,000 points.

Working out the right weighting for each stock within the index is highly complex as their market values are constantly changing.

On top of that, adjustments have to be made to the index value for stocks going ex-dividend, corporate actions like rights issues, and takeovers such as last year’s deal between Melrose (MRO) and GKN.

That said, the weighting of the top 10 stocks is about the same today as it was 10 years ago at around 45%.

OILS AND BANKS DOMINATE THE FTSE

The stocks with the biggest weightings are Royal Dutch Shell (RDSB) and BP (BP.) which together make up just under 20% of the index.

However this is a bit misleading as there are two classes of Royal Dutch Shell shares, A and B, and each is included in the index meaning there are actually 101 stocks in the FTSE 100.

For most investors the FTSE is the benchmark and no-one questions whether there might be a better way of calculating it.

For those who don’t want all their eggs in one basket however, there is a FTSE 100 equally-weighted Index.

It includes all the same constituents as the FTSE 100 index but each company has a weighting of just 1%.

Launched in September 2011 with a base value of 100, it has out performed the standard FTSE 100 since inception with a compound annual growth rate of 8.5%.

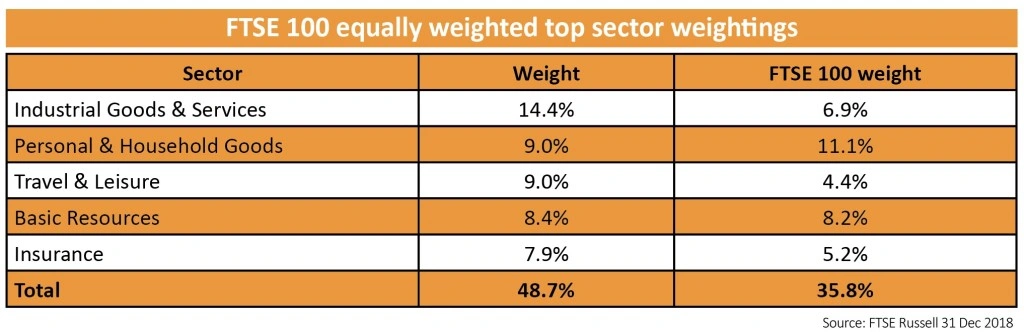

On an equally-weighted basis oil producers are the major losers with their weighting falling to just 2.8%.

Banks are also big losers with their weighting falling to just 5%.

The big winners are industrial goods and services, travel and leisure, retail and media.

While mining stocks look as though they are winners, taking three of the top five spots, in fact the sector has a similar weighting to the standard FTSE 100.

REDUCING THE INFLUENCE OF MEGA-CAPS

Clearly what equally--weighting the index does is play down the impact of mega-cap stocks like BP, Royal Dutch Shell and HSBC (HSBA), and play up the performance of smaller stocks.

It also increases diversification and reduces the risk profile of the index because mega-cap stocks can just as easily lose money as make money and by reducing their relative weight any damage can be limited.

There is a wealth of historical evidence to show that smaller stocks do better than larger stocks over the long term.

In an article in the Financial Times, authors Robert Ferguson and David Schofield showed that from January 1966 to June 2010 an equally-weighted portfolio of S&P 500 stocks beat the market value-weighted S&P 500 by around 3% per year.

Even in the short time that the equally-weighted FTSE 100 has been in existence it has beaten the standard index by around 1.5% per year.

VOLATILITY IS LESS THAN YOU MIGHT EXPECT

In theory giving smaller stocks a bigger influence ought to make the equally-weighted index more volatile than the standard index but that’s not the case.

As the table below shows, over one year, three years and five years the volatility figures are very similar.

Naturally as share prices move the weightings of each stock changes over time so the equally-weighted index is re-balanced every quarter.

This means taking money out of stocks which have outperformed and putting it into those which have underperformed so that they are equally weighted again at the start of the next quarter.

There is a cost to this but it is more than compensated by the better performance of the equally-weighted index over time.

In fact by taking small profits in stocks which have outperformed and reinvesting the gains in those which have underperformed the index is using a ‘buy low/sell high’ approach.

Naturally there are no guarantees with investing but for those interested in an equally-weighted approach there are tools and products out there. Among them exchange-traded fund Xtrackers FTSE 100 Equal Weight (XFEW) which has an ongoing charge of 0.25%.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.