Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineThis fund makes money every time the songs it owns are played

Investments uncorrelated to the market are increasingly sought by individuals looking to diversify their portfolio during volatile times.

That might explain why investment trust Hipgnosis Songs Fund (SONG) is currently trading at a premium to the value of its assets.

It owns the rights to certain pieces of music and receives a royalty payment each time they are played on the radio, streamed online, feature in adverts, films, TV programmes or computer games, or are bought on CDs or vinyl. It is confident this income should help to fund a steady stream of quarterly dividend payments for shareholders.

Merck Mercuriadis, former manager of artists Elton John and Iron Maiden and founder of the investment trust’s adviser The Family (Music), argues that music is consumed regardless of the economic backdrop, meaning that Hipgnosis’ income stream should be predictable and reliable.

‘People consume music in both good and bad times. In difficult periods people want entertainment to get away from the negativity in real life,’ he says.

IPO DELAYED THREE TIMES

Hipgnosis had a few false starts joining the stock market as potential investors took a long time to fully understand the music rights market, says Mercuriadis. ‘The IPO took longer than I expected; it was naivety on my part. It took time for investors to understand why the asset class was predictable and reliable.’

Seneca Investment Managers was among the institutions to have backed the trust, saying it was attracted to its bond-like characteristics and low correlation to other asset classes.

‘We understand Hipgnosis’ broad cash flows and pricing models,’ says Gary Moglione, a fund manager at Seneca. ‘The Hipgnosis team is comprised of industry veterans, including songwriters and chief executives-to-chief financial officers from the music industry.

‘We feel they can identify the best catalogues, complete the purchase at the right price and manage those assets by enhancing revenue from other areas such as advertising and video games to give us that extra upside potential.’

ACQUISITION COSTS

Having finally floated in July 2018, Hipgnosis has now deployed at least £73m of the £200m raised at its stock market listing, with a £600m pipeline of future deals under negotiation. The trust is bound by confidentiality agreements concerning deal pricing and can only reveal that investments to date have been made on an average of 12.2 times historic annual net income.

‘The valuation process is difficult as this is a fairly opaque market,’ says Moglione. ‘A little over a year ago Round Hill Music purchased one of the industry’s prized assets in the form of the Carlin music catalogue. This contained songs from James Brown, AC/DC, Meatloaf and Billie Holliday and Christmas classics such as Santa Baby and Jingle Bell Rock’.

‘The reported price paid was 16 times the catalogue’s earnings generating yields of around 6%. An “evergreen” catalogue may trade at 11 to 13-times (yielding 7% to 9%). The more speculative “unproven” catalogues will trade on lower multiples,’ adds the fund manager.

EXAMPLES OF SONGS HIPGNOSIS OWNS

The goal is to obtain the rights to music that has long-lasting appeal. So far Hipgnosis’ investments include a mixture of new and old songs including the rights to songs performed by Sister Sledge and Diana Ross such as We Are Family and I’m Coming Out, respectively.

It recently acquired a music catalogue from songwriter Itaal Shur which includes the song Smooth, recorded by Santana and ranked as the second most successful song of all time, according to Billboard. The media outlet last year said Smooth generates approximately 1m on-demand streams per week, citing Nielsen Music data.

Hipgnosis focuses on striking deals with producers and songwriters rather than artists because it believes they are more likely to want to take a cash lump sum upfront instead of having a longer-term stream of income from royalties.

‘If you’re an artist like Neil Young and we approach you to buy the rights to your songs, you have several options. One is to sell to us, but the others include going on tour and selling tickets and merchandise to get more money.

‘Neil Young has the brand to do that; a songwriter doesn’t have the same ability which is why many are happy to take our money upfront,’ says Mercuriadis.

FIGHTING OFF COMPETITION

While there is competition to buy song royalties, Mercuriadis claims his team is the only one to come from the artistic community, giving them an advantage during the negotiating process.

‘I’ve made my success with artists rather than at the expense of them and producers. Other people buying royalties are just bankers. I will take someone’s output and make sure it is nurtured, loved and appreciated and that their legacy will grow.’

The investment adviser says many companies who own the rights to tens of thousands of songs only have a limited number of staff, meaning they struggle to deal with licencing requests and they miss revenue opportunities.

‘We have fewer songs but a good team who come up with ideas and go looking for ways to implement them with the right partners. For example, it might be saying this song would be great for this movie, or that song would work in that game,’ he comments.

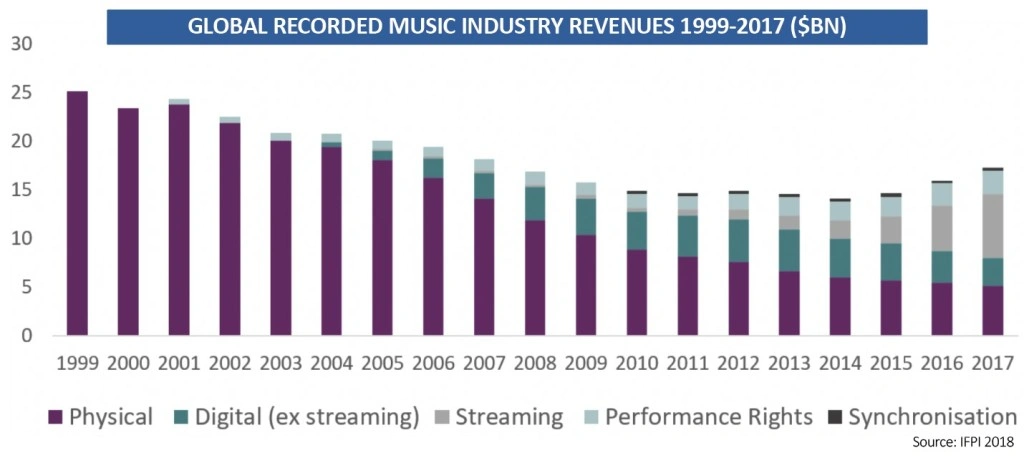

THE PROS AND CONS OF STREAMING

The public is increasingly streaming music via sites such as Spotify or YouTube rather than buying CDs or digital downloads. Artists continue to complain about the extremely small royalty cheques they receive from these services. Could this not pose a risk to Hipgnosis in terms of future income?

Mercuriadis admits that rates are low but insists it is just an evolutionary process. He gives the example of The Beatles signing to EMI in 1962 and the advent of the long-player (LP) format.

‘In the early days The Beatles were getting less than 1% royalty. More people then started consuming music via LPs and by the time The Beatles broke up eight years later they were on 25% royalties. The same thing will happen to streaming services.

‘The idea of streaming payments currently being anaemic is not something you can argue with. Instead, you should focus on the explosion in music consumption.’

He draws attention to various telecom companies bundling streaming subscriptions as part of new phone contracts as an example of how even greater numbers of people are accessing these services.

POTENTIAL EARNINGS UPLIFT

Last year the Copyright Royalty Board announced that songwriters’ share of royalties would increase from 10.5% to 15.1% in the US streaming market over the next five years.

‘To date the music streaming market has been dominated by YouTube with a 46% share,’ says Moglione at Seneca. ‘However, YouTube pays a much smaller percentage of revenue on royalties compared to companies such as Spotify. It uses outdated safe harbour laws from 1998 that were intended to protect passive online intermediaries.

‘If the legislation were updated to ensure YouTube had to move toward Spotify’s level of royalty payments this would provide a sizeable revenue uplift.’

OUR VIEW ON THE INVESTMENT CASE

Hipgnosis was priced at 100p when it floated last summer and said it would target an initial 3.5% dividend yield based on the listing price.

Once fully invested it expects the yield to rise to 5%. It hopes to generate 10% or more annual total net asset value returns over the medium term, net of fees.

The shares currently trade at 108p which is a 10.6% premium to the 97.68p net asset value as at 30 September 2018, the last published information.

In general, investors should only consider buying a trust at a premium if there is something special on offer, such as a high quality fund manager or superior assets.

In Hipgnosis’ case, we think the shares are worth buying at the current price as the investment adviser has already shown expertise in buying good assets and it looks like there is a lot more to come.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.