Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineFantastic 4imprint is a master of promotion so buy its shares now

Investors should take advantage of an opportunity to buy promotional products firm 4imprint (FOUR) while its valuation is towards the bottom of its historic range and as the benefits of a recent marketing push start to become apparent.

Full year results on 5 March could offer a near-term catalyst to drive the share price higher. We also see this as a growth stock to hold for the longer term with a credible target to hit $1bn in sales by 2022. For context, 2018 revenue was a little under $740m.

WHAT DOES THE COMPANY DO?

The firm sells items like branded mugs, dongles and pens to companies, almost entirely in the US, and has a nice habit of under-promising and over-delivering while generating plenty of cash.

The company has invested heavily in technology to build a proprietary processing platform which uses database analytics to drive efficient marketing to its client base.

Principally based in Wisconsin, 4imprint does not typically manufacture the products it sells itself but outsources this work to third parties which means it has limited capital requirements.

This underpins a modest but growing ordinary dividend and the company has paid special dividends in the past when cash has built up on the balance sheet.

It also only carries limited inventory with suppliers holding stock instead, printing the relevant product and often shipping direct to the client. However, 4imprint does have a large distribution centre with some manufacturing capability for higher specification items.

All told it has thousands of products which can be customised and shipped in 24 hours or less. Strong relationships with its suppliers are underpinned by good lines of communication and timely payments.

The idea of promoting a business through a branded pen or coffee cup might seem old-fashioned but in there is still strong demand from corporations for these items for both external marketing and to motivate staff.

SUCCESS WITH SELF-PROMOTION

Unsurprisingly given its area of expertise, 4imprint is good at promoting itself. A brand awareness programme, at a cost of $7m, was launched in 2018. This encompassed a TV-based campaign and was aimed at making the company synonymous with promotional goods.

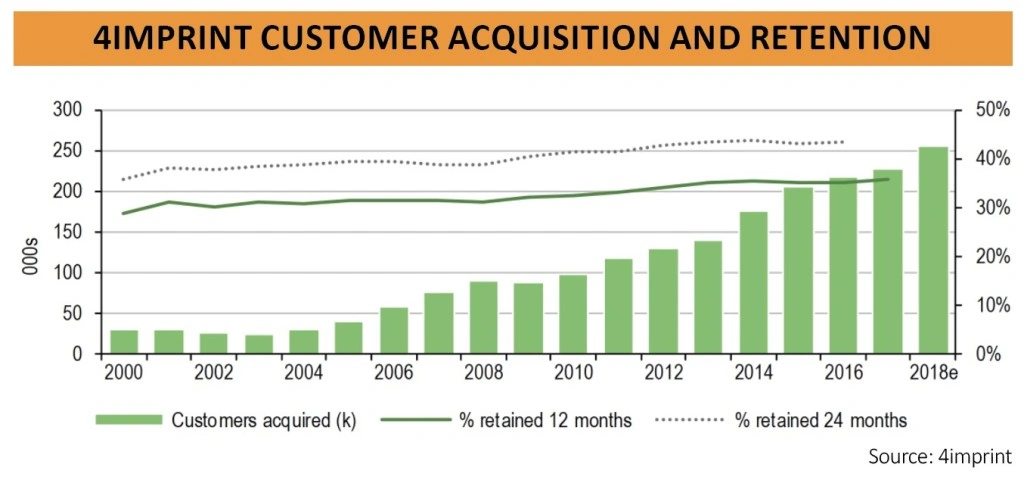

The effort appears to have reaped early benefits, helping propel year-on-year organic revenue growth in the second half of 2018 to 18.7% from 16.5% in the first half according to a 17 January trading update which also guided for full year profit to be at least at the top end of the market range at around $45m. Management estimate that second half growth in its wider market was more like 5%.

Despite being the leading operator, 4imprint has a very large addressable market to exploit. Worth some $23bn in the US, the promotional products market is highly fragmented and 4imprint has less than a 3% share.

ORGANIC GROWTH FOCUS

4imprint is growing organically rather than looking for short-cuts through acquisitions, with all the risks of over-paying and integration that might entail.

It does something which in our view all the best businesses have in common – it really understands its customer base. It uses a mixture of technology and people skills to anticipate what clients want which reinforces its ability to retain and acquire new customers.

The shares currently trade on a price-to-earnings (PE) ratio of around 17.5-times based on Peel Hunt’s earnings per share forecast for 2019. This compares with a five-year average PE of 19.7-times according to the broker, with the stock frequently trading at more than 20 times earnings. The well-supported forward dividend yield comes in at 2.9%.

WHAT ARE THE MAIN RISKS?

A key risk for investors to weigh is the company’s historic tendency to track fluctuations in US GDP growth. However, while there are expectations for slowing growth across the Atlantic, recent releases suggest the economy remains in decent shape and a more patient approach from the US Federal Reserve on interest rates could help support business confidence.

Like many firms and industries, there has been speculation of a competitive threat from online retailer Amazon, however it would be difficult for an outfit like Amazon to replicate 4imprint’s personalised approach and attention to detail.

The company also has pension liabilities associated with its small UK operation but a series of large contributions since 2012 have seen the level of payments into its pension scheme now become more modest and predictable.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.