Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

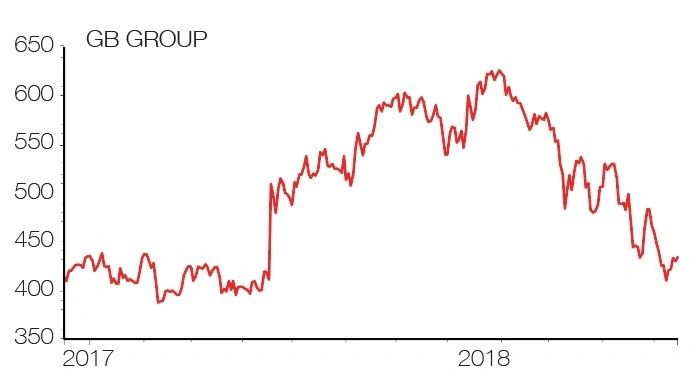

magazineShare pick for 2019: GB Group

It’s hard to escape talk of Brexit uncertainty and potential growth slowing on a global scale as we enter 2019. So a company at the top of its structurally growing market, one that is potentially insulated from economic wobbles and capable of expanding for years to come, should be attractive.

GB Group (GBG:AIM) is a rare British-made world leader at the heart of the digital transformation.

We all know that people are embracing the internet at a rapid pace, from the online shopping explosion to booking travel, buying services and much else. Chester-based GB provides identity data intelligence and location insight, essentially giving primarily business-to-consumer customers and government organisations the information required to decide who to trade with, who to block, and fraud prevention all within a compliance-friendly platform.

Divided into two divisions – Location and Customer Intelligence and Fraud, Risk and Compliance – the company has what some analysts have called unparalleled and compliant access to data from more than 500 different sources. These include areas like credit reference agencies, electoral rolls, passport and national ID registers, postal services, retail consumer data and social media.

Staffed by more than 800 people in 18 countries, GB now counts in excess of 18,000 customers for industries as diverse as financial services, gaming, travel and retail.

It remains largely a UK company with two thirds of last year’s £119.7m revenue earned in its own backyard. That is changing, partly through organic means but also via carefully selected acquisitions, such as Vix Verify in Australia in October.

Last year just 2% of revenue was earned in Australia and 10% from the vast US market, and it is this global expansion that represents the other core growth driver of the business beyond the consumer switch to online everything. Recent momentum along these lines has been encouraging.

GB doesn’t have the market to itself. Key competition comes from large credit checking agencies, such as UK-based Experian (EXPN) or Equifax in the US. GB’s view is that its deeply layered and international datasets, plus adaptable technology platform, give it a key edge.

The stock is also not cheap, a point that will put off some investors. The price-to-earnings multiple for the year to 31 March 2020 currently stands at 28-times.

Yet this is based on forecasts that analysts admit may be on the conservative side, with Numis saying earlier this month that it expects an acceleration on the high single-digit revenue growth and 19% operating margins currently forecast. It anticipates a 600p share price over the next year.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Aequitas

Big News

Editor's View

Feature

Great Ideas

- Share pick for 2019: Hollywood Bowl

- Share pick for 2019: Rolls-Royce

- Share pick for 2019: GB Group

- Share pick for 2019: Euromoney

- Share pick for 2019: Next

- Share pick for 2019: Renishaw

- Share pick for 2019: Fevertree Drinks

- Share pick for 2019: Keystone Law

- Share pick for 2019: On The Beach

- Share pick for 2019: Coats