Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineShare pick for 2019: Rolls-Royce

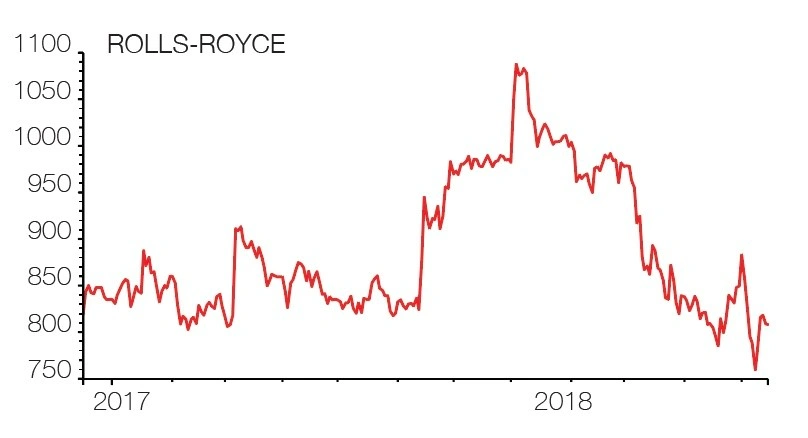

It may have been a testing year for Rolls-Royce (RR.) thanks to a series of engine inspection issues yet this remains a global champion now trading at a rare discount. It comes as no surprise to Shares that long-term growth funds run by the likes of Baillie Gifford and activist investor ValueAct Capital are shareholders.

Forget luxury cars, and soon ships (the Marine division is being sold), the future is all about planes, trains and power systems.

Aero engines, both commercial and defence, make up three quarters of revenue and Rolls has grown to become the senior player in an effective global duopoly (ahead of rival General Electric) in civil aviation. This area is worth more than half of its total sales.

While this is a highly technical and cutting edge science-based business, the model is easy to understand. It builds engines, often selling them at cost, and then enjoys substantial profit over the typical 25-year engine lifecycle from servicing.

Get more engines on more planes that fly more air miles and you’ve got a virtuous cycle of bumper cash flow long into the future. That cash should then underpin a growing stream of dividends.

Rolls has enjoyed prolonged spells of growth over the years, and we believe it is on the cusp of a new growth leg that will push the share price higher. For example, in the 10 years between 2003 and 2013 Rolls-Royce’s stock increased more than 10-fold to nearly £13.00.

Since then life hasn’t been as easy. There has been a corruption scandal and multiple profit warnings which nearly saw the company fold, according to its current chief executive Warren East. But the former boss of UK chip design champion ARM is making real headway in putting the pieces back together again.

Efficiency improvement and sharper execution lie at the heart of East’s plan, as well as vastly improved free cash flow. This restructuring will see 4,600 jobs go at its state-of-the-art facility in Derbyshire but they will largely come from bloated admin and middle management layers, so core engineering capacity should not be damaged.

Expectations for 2018 were pared back to reflect the major operational upheaval; the longer-term prospects are getting much brighter. Investors should expect £1bn of free cash flow by 2020 and similar pre-tax profit. Dividends are also set to start climbing again, with 11.7p per share in 2017 expected to increase to 17.4p by 2020.

So while the near term-term price-to-earnings valuation metric looks expensive (29.5-times for 2019), investors are really buying the potential rapid recovery. The 2020 PE falls to 18.7-times. We expect the share price to break back above £10.00 in 2019.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Aequitas

Big News

Editor's View

Feature

Great Ideas

- Share pick for 2019: Hollywood Bowl

- Share pick for 2019: Rolls-Royce

- Share pick for 2019: GB Group

- Share pick for 2019: Euromoney

- Share pick for 2019: Next

- Share pick for 2019: Renishaw

- Share pick for 2019: Fevertree Drinks

- Share pick for 2019: Keystone Law

- Share pick for 2019: On The Beach

- Share pick for 2019: Coats