Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWill AO World ever make a profit?

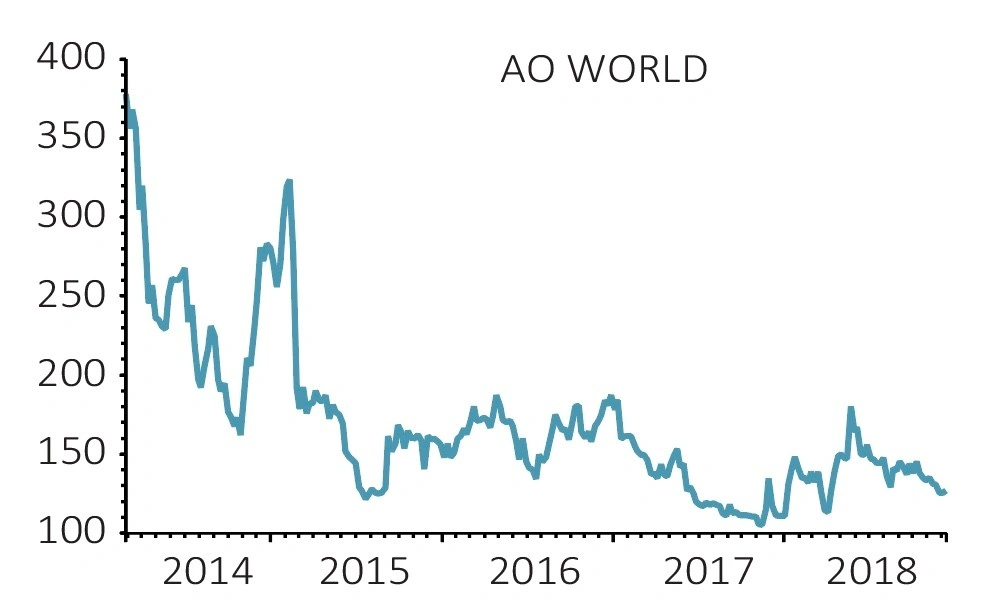

Shares in online electrical retailer AO World (AO.) have fallen by 56% in value since joining the stock market in 2014.

The compelling investment case outlined nearly five years ago was that AO World would disrupt the UK white goods market, yet according to brokerage Shore Capital, AO World is ‘in a perpetual downgrade cycle that, in our view, looks sustained’.

THE GOOD AND THE BAD

There is much to like about AO as a business, guided by a forthright, entrepreneurial management team and operating in the structurally advantaged online channel, meaning it is unencumbered by a physical store estate.

The Bolton-headquartered concern sells a vast, competitively priced range of goods and its standout customer proposition drives exceptional customer satisfaction and healthy repeat purchase metrics. AO is delivering against its purpose to ‘have the happiest customers by relentlessly striving for a better way’.

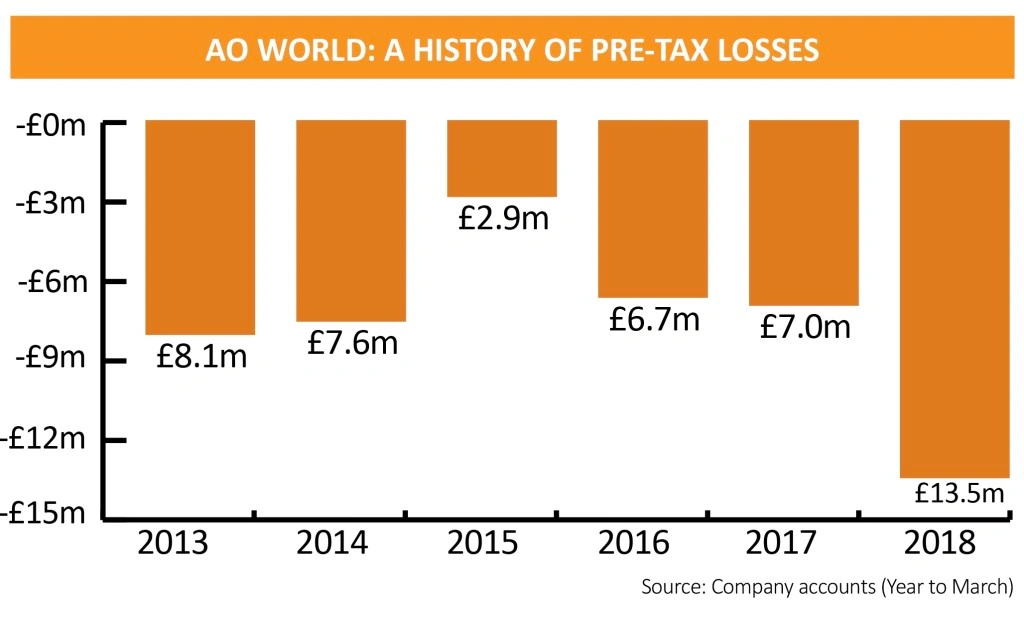

And yet the washing machines, TVs and laptops seller has consistently struggled to generate a profit at the all-important pre-tax line, reporting material losses for the past five years; a function of start-up costs and trading losses in Europe, some chunky marketing costs to raise brand awareness and fierce price competition.

Earnings downgrades remain the order of the day and group-level profit proves elusive. This stands in stark contrast to online pure play peers [ASOS (ASC:AIM) and Boohoo (BOO:AIM), albeit specialists in fast fashion, a duo which consistently deliver positive earnings.

THE BUSINESS HAS CHANGED

Since coming to the stock market, AO has become a more complex business too. It has transformed from a one country (UK), one category (domestic appliances) retailer into a multi-national, multi-category player, also selling audio-visual and computing products as well as mobile phones.

Indeed, the recent acquisition of online-only outfit Mobile Phones Direct has increased the scale and sophistication of AO’s mobile proposition.

AO also provides ancillary services such as installing new, and collecting old products, it offers product protection plans and customer finance and has a majority stake in AO Recycling, a waste electrical and electronic equipment processing facility

in the UK.

ON A RAZOR’S EDGE

The company operates on razor thin margins, having to source, sort and then deliver many big ticket items in a currently challenged domestic appliance market. Consumer uncertainty surrounding Brexit is impacting purchases of bigger ticket items, while competition in the electrical retail space remains ultra-competitive.

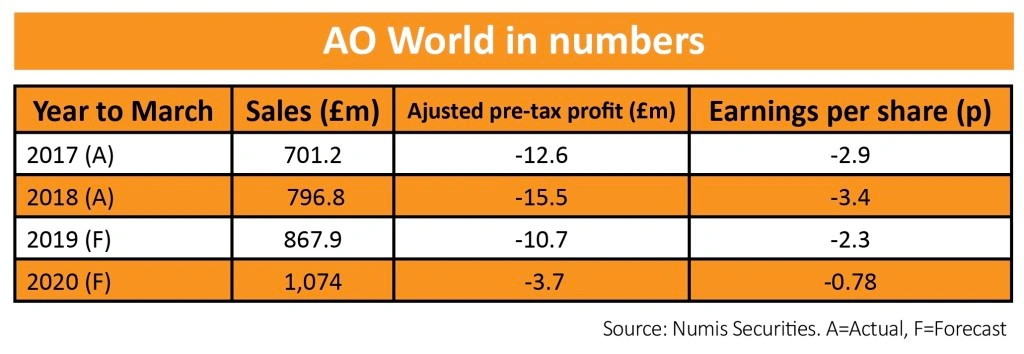

Half year results (20 Nov) revealed solid but not amazing group revenue growth, up 9.9% to £404m, amid tough macro conditions in Europe and a declining UK domestic appliance market.

The group’s adjusted EBITDA (earnings before interest, tax, depreciation and amortisation) loss of £5.4m showed improvement on the prior year’s £6.3m loss.

UK EBITDA edged back to £6.9m from £7.4m a year earlier, with growth slowing in the six months to 30 September; newer product categories generated lower margins and AO World’s higher admin costs crimped returns. Tellingly, the half year adjusted EBITDA margin for the more established UK arm was wafer-thin at just 2.1%.

While the UK operations are at least profitable, investment in scaling up the international business and general costs of running the business are keeping AO World in loss.

DOES EUROPE STILL EXCITE?

AO World hopes its European business will make a profit by 2021. Europe, the most exciting bit of the investment case, reduced its adjusted EBITDA loss to €13.8m (2017: €15.6m), reflecting product margin improvements and leverage in logistics and overheads.

However, revenue growth is also starting to slow in Europe. European revenue rose 35% to €78m, but growth was hampered by weaker German domestic appliance market conditions and changes to the German driver operating model following changes to the EU working time directive.

Numis Securities says: ‘AO’s UK challenges relate almost entirely to the downturn in the white goods market, which has resulted in the loss of high incremental margin revenue, fierce major domestic appliance price competition, and the need for investment in other growth areas.’

AO has it all to do over Christmas and we’ll get a better idea when the trading update is issued on 11 January.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Aequitas

Big News

Editor's View

Feature

Great Ideas

- Share pick for 2019: Hollywood Bowl

- Share pick for 2019: Rolls-Royce

- Share pick for 2019: GB Group

- Share pick for 2019: Euromoney

- Share pick for 2019: Next

- Share pick for 2019: Renishaw

- Share pick for 2019: Fevertree Drinks

- Share pick for 2019: Keystone Law

- Share pick for 2019: On The Beach

- Share pick for 2019: Coats