Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineCraneware’s niche health solutions will see it grow rapidly for years to come

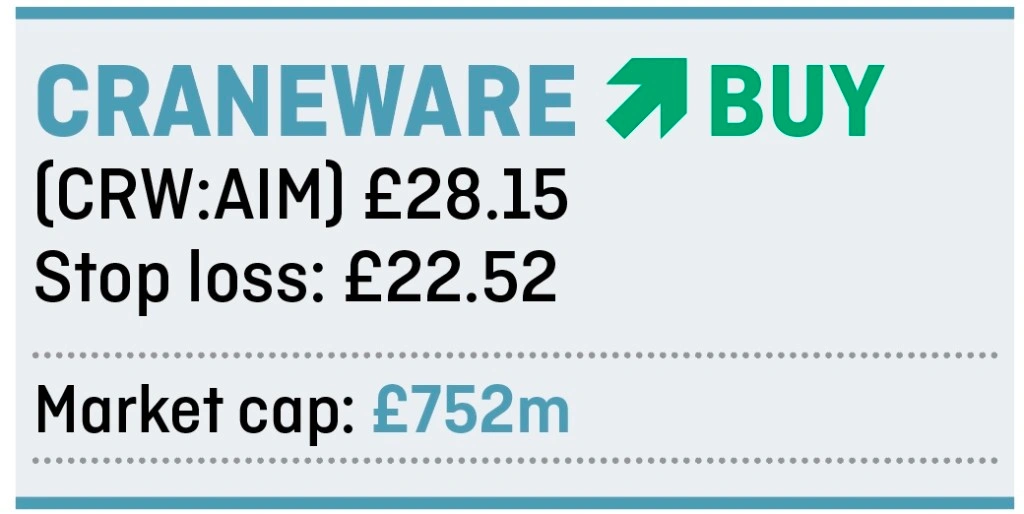

Scotland’s Craneware (CRW:AIM) supplies innovative financial analysis, performance and monitoring tools to hospitals and other healthcare providers.

It may seem something of a curiosity to many investors since nearly all of its business is in the US despite the company being based in Edinburgh. That stems from the private healthcare system across the pond.

What is most important for investors to understand is that this is a fast growing business concentrated on a niche which is itself only starting to embrace new automated technologies, especially important as patient outcomes becomes the benchmark for performance.

Founded in 1999 by Keith Neilson and Gordon Craig, Craneware provides technology solutions through its Chargemaster and Pricing Analyser toolkits that help hospitals and other healthcare providers more effectively price, code, charge and retain earned revenue for patient care services and supplies. Keith Neilson remains the chief executive officer and main driving force.

Today Craneware employs 300 staff, and provides solutions to almost one third of the hospitals in the US. These are significant numbers. Research suggests that the average 350-bed hospital misses out on $22m in revenue capture opportunities every year.

This is where Craneware can help, identifying new income opportunities to healthcare management as well has highlighting operational and financial risks.

TIME TO SHINE

One area where it shines is automating the authorisation code journey. This ensures that each patient gets tracked right through the treatment process, gets the help they need from doctors and healthcare professionals, and vitally for the hospital, ensures that accurate charges are billed to a patient’s insurance company.

If that sounds labour intensive, it is. Yet amazingly, today most of that work is still done by admin staff using spreadsheets. That’s a lot of human resource hours with massive scope for mistakes to creep in.

Craneware has been busy adding extra tools and services to its platform which should help bolster already sticky customers. This is opening up a vast pharmacies market through its fairly new Pharmacy ChargeLink toolkit.

About 85% of the firm’s annual revenue is of a recurring nature while its niche solutions and deep integration into the financial running of a hospital would make it very difficult for existing healthcare providers to ditch Craneware’s solutions for an alternative.

Analysts anticipate 18% revenue growth a year going forward with $79m pencilled in this year to 30 June 2019. That implies pre-tax profit in excess of $24m. It reported $18.9m last year, so 28% growth. But the point is, Craneware looks likely to continue to put up those sort of high teens to 20% growth numbers for years to come.

That it is a highly cash-generative model bolsters the long-run growth appeal. It is already paying dividends, albeit, modest ones right now. The shares have slumped nearly 20% during the recent sell-off yet little has changed in terms of Craneware as a fast growth, high quality investment story. (SF)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.