Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineFTSE 100 earnings estimates on the rise despite correction

The FTSE 100 may be under pressure once more, as it fights to hold on to the 7,000 mark, but the good news is that aggregate earnings forecasts for the UK’s benchmark index continue to rise, if only steadily.

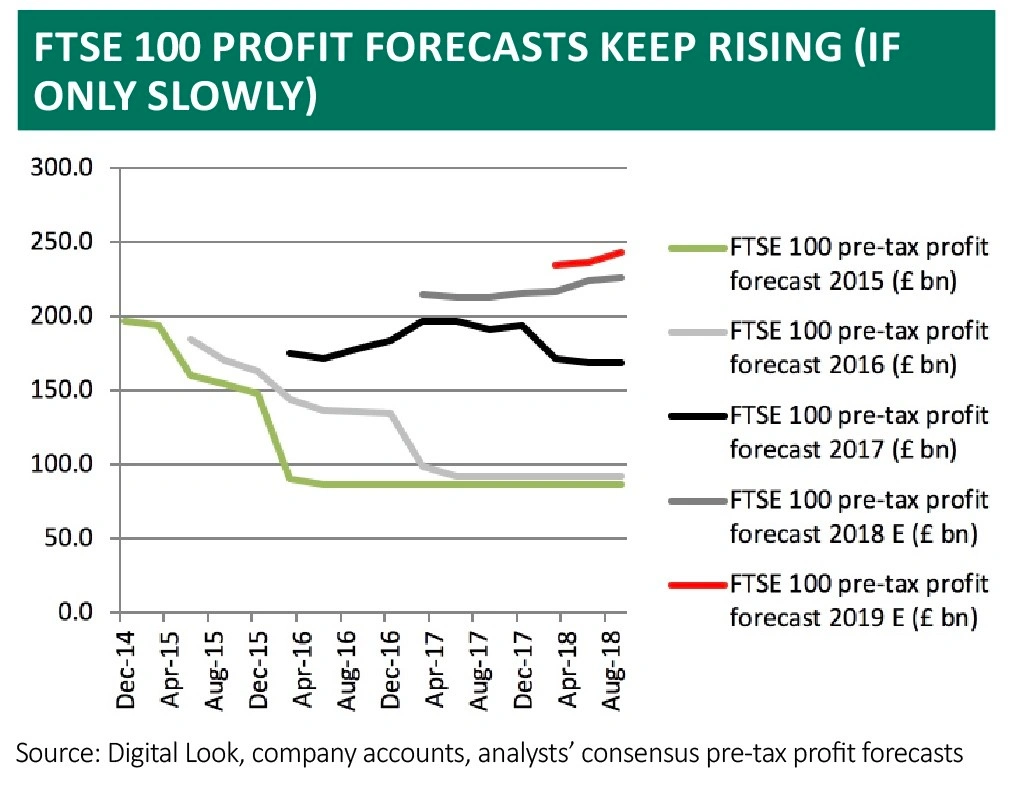

Pre-tax profit forecasts for 2018 now stand at total of £225.8 billion, some 6% higher than they were a year ago, while estimates for 2019 are also showing positive momentum with a fourth straight annual increase to £242.9 billion the current analysts’ expectation.

With the FTSE 100 index having fallen by 4% while profit estimates have advanced 6% over the past 12 months the benchmark has become cheaper. Based on consensus forecasts the benchmark now trades on just 13.5 times earnings for 2018 and 12.4 times for 2019 (compared the 18 times and 16 times multiples currently afforded to America’s S&P 500).

Dividend forecasts also continue to rise, rather than fall, so the FTSE 100 now offers a 4.3% yield for 2018 and 4.5% yield for 2019, assuming that analysts’ forecasts prove correct.

This suggests that the unloved UK equity market – regularly flagged as an ‘underweight’ among fund managers in the surveys such as that carried out by Bank of America Merrill Lynch – could be offering some contrarian value, at a time when value seems hard to find.

LOOKING FOR A TRIGGER

The tricky bit is finding what could act as a catalyst that could persuade investors to reassess the case for UK equities and unlock that value.

Merger and acquisition activity has yet to convince the doubters, despite a series of bids for FTSE 100 and FTSE 250 firms, including GKN, Sky (SKY), Shire (SHP) and a failed approach for Smurfit Kappa (SKG), which suggest that overseas trade buyers see value in the UK even if financial buyers do not.

Nor is the absence of net profit downgrades proving enough, even if it compares favourably to 2014, 2015, 2016 and also 2017, when more write-downs and conduct costs at the banks dragged the final total down right at the end.

It is possible that investors remain concerned over the mix of the FTSE 100’s earnings progress, which remains reliant upon oils, financials (notably banks) and miners in particular, all sectors that cannot be described hand-on-heart as inherently reliable or easy to predict.

BANKING ON THE BANKS

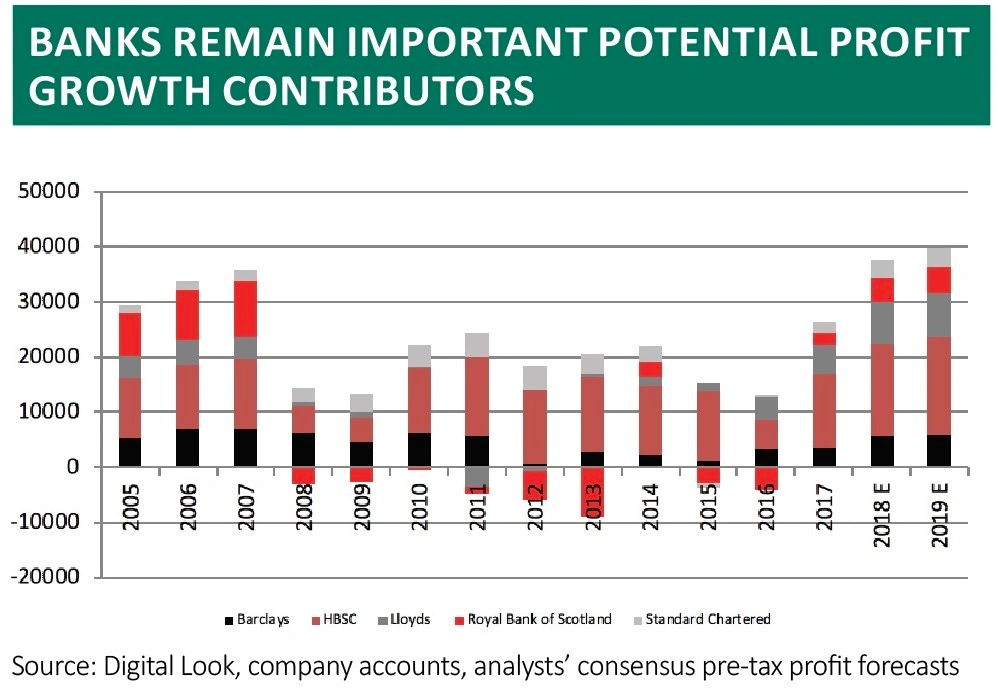

The banks remain particularly important.

For the umpteenth year in the row, analysts are expecting the big five banks to generate profits that match the pre-crisis peak of £36bn.

Although such forecasts have proved inaccurate for the past several years, the good news at the moment is the profit estimates for the big lenders are rising, not falling. In June, analysts expected the big five to rack up aggregate pre-tax profits of £36.4bn and that figure has now reached £37.5bn.

However, it is in the second half of the year, and especially the fourth quarter, that the banks tend to book the bulk of any bad loans, asset write-downs, regulatory costs and restructuring charges so nothing can be taken for granted just yet.

The imminent third-quarter reporting season for the banks, which kicks off on 24 October with Barclays (BARC) and ends on 31 October with Standard Chartered (STAN), should prove informative.

Poor share price performance in the sector also suggests that investors are not entirely convinced that the banks’ earnings forecasts are wholly reliable, because perhaps because of fresh worries over Italian banks’ health, even if rising interest rates and bond yields are in theory positive for the lenders’ net interest margins.

RISK ON, RISK OFF

The reliance on cyclical sectors like banks and miners also leaves the FTSE 100 susceptible to the kind of switch towards ‘risk-off’ sentiment which currently seems to be affecting global stock markets, especially as the Brexit situation remains unclear.

It may therefore be that UK equities will struggle until markets have a clearer picture of how Brexit will look and how it could impact specific stocks and sectors or the British economy more generally.

But with the pound depressed and equity valuations looking tempting contrarians might like to start doing their research on certain companies or sectors, especially if they think a Brexit deal is possible or that even a hard Brexit may not have as big an impact as those in the Remain camp will argue.

In truth, no-one knows. But it can be argued that valuations are at least pricing in some degree of uncertainty and a negative outcome, although if the oil and metals prices retreat and the wider economy slows, to the detriment of the banks’ earnings, then FTSE 100 could profit estimates could prove too optimistic – and then the index would have to fall a lot further for it to look cheap on an earnings basis.

By Russ Mould, investment director, AJ Bell

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.