Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineLowland plays the waiting game

Run by experienced fund manager James Henderson for the best part of 30 years, Lowland Investment Company (LWI) has an approach of investing across the market cap spectrum on both AIM (London’s junior market) and the Main Market. This allows it to pick from a universe of upwards of 1,000 stocks.

But, as his co-manager Laura Foll explains, even with this level of choice it is becoming increasingly difficult to find opportunities. Foll notes Lowland is reducing gearing – like all investment trusts Lowland can use borrowed money to invest – from around 13% down to 7% and says the direction of travel is ‘gently down’.

It is achieving this by scaling back its holdings in some of the good quality mid and small cap names in its portfolio which have already rerated, i.e. moved to a higher price-to-earnings (PE) ratio. PE is a popular ratio used to value a company’s shares. It is calculated by dividing the current share price by its earnings per share.

Foll elaborates: ‘It’s not necessarily a top down call on the market, it’s more in stock picking terms we are finding more than sell opportunities than buy opportunities.

Scaling back holdings

‘One of the companies where we’ve been selling a long-held position is safety barrier specialist Hill & Smith (HILS) – which has caught people’s imagination thanks to its exposure to roadbuilding in the UK and a potential infrastructure programme in the US. It’s a good quality company with excellent management but that is reflected in a high teens (PE) multiple.’

The trust has also been selling two companies which are subject to takeover approaches in insurer Novae (NVA) and industrial services provider Cape (CIU). Novae agreed a £468m takeover from Bermuda-based Axis Capital in July and Cape has received a £332m bid from French rival Altrad.

Foll says: ‘Another one we have been reducing is Conviviality (CVR:AIM) – it’s a good team which have managed it really well but a multiple in the mid-teens is quite high for a distributor. Ultimately, we’d be happier if we didn’t have to reduce our holding.’

Simple approach to valuation

Lowland applies quite simple valuation metrics including the PE ratio, enterprise value (encompassing a company’s market value alongside any debt) to sales and price to book or net asset value (NAV). Price to book looks at the share price relative to the value of the company’s assets per share.

Foll explains the investment trust also looks closely at the management teams of small and mid-cap companies but considers this to be a less important factor for large cap firms.

Although Foll says Lowland has been quite cautious on initial public offerings (IPO) of late, it did participate in the IPO of kettle safety controls specialist Strix (KETL:AIM), attracted by the cash generative outfit’s ability to pay generous dividends. Analyst forecasts imply a 7% dividend yield. An IPO is the first time a company sells its shares to the public market.

Another recent addition to the portfolio is a modest position in pharmaceutical giant AstraZeneca (AZN) after it endured the worst ever one-day share price performance (down 15%) on the failure of a key drugs trial (27 Jul).

Foll says she would happily add back some of the companies where Lowland has been reducing its holdings if their valuations were to fall from the current elevated levels.

‘Investing for income isn’t really working, neither is value investing – it’s all about earnings momentum and that’s why parts of the market are looking quite stretched,’ Foll says.

Cautious on domestic UK names

The investment trust has limited exposure to the retail sector. ‘There has been some debate over whether domestic UK names are undervalued but we are generally quite cautious on the domestic UK, we don’t have much exposure to retail and we are reluctant to add to our domestic exposure.’

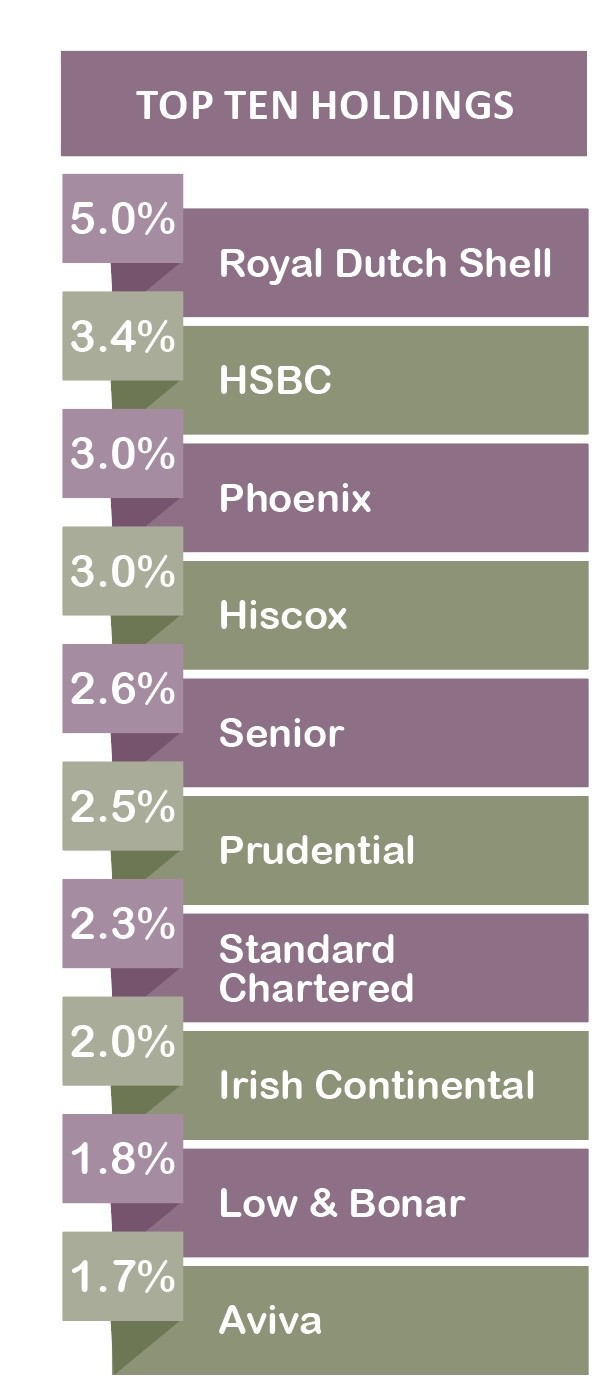

Although its portfolio includes the international-facing banks HSBC (HSBA) and Standard Chartered (STAN), it is not invested in the likes of Lloyds (LLOY) and Royal Bank of Scotland (RBS).

Another domestic sector it is avoiding is the housebuilders which Foll recognises look cheap based on their PEs and dividend yields but not, crucially, based on price to NAV. ‘It’s price to book which we find off-putting,’ she adds.

Although the mandate allows 20% of the fund to be invested overseas, Foll says it is unlikely this will be fully exploited. ‘There are plenty of companies with an international focus among the small and mid-caps,’ she says. ‘We don’t want to confuse the investment mandate.’

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- Big news in the banking sector

- Gambling stocks in focus ahead of Government review

- Cobham appoints former Airbus UK chief

- MJ Gleeson is one of our top picks among housebuilders

- What next for investors after German elections?

- Central Asia Metals’ zinc move makes the stock higher risk

- UK hotel growth to decline in 2018