Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazinePortfolio protection

Despite geopolitical tensions in the Korean peninsula, an unstable US President and the looming threat posed by Brexit, global markets continue to charge ahead. Earlier this month the US Dow Jones Industrial Average marked its 40th record close of 2017.

Even the UK’s flagship index – the FTSE 100 – remains firmly above the psychologically important 7,000 mark.

The big question is whether the bull-run in so many stock markets around the world can keep going. Markets have historically undergone corrections (10% decline or more) fairly regularly and it seems we are long overdue another one.

In this article, we talk to market experts about whether we have reached the market peak, the potential obstacles to further market gains and what you should do to prepare for any potential correction.

What is the current level of investor sentiment?

Across the Atlantic retail investors have never been more hopeful of further stock market gains. The University of Michigan survey for September showed a record 65% expected probability that stocks would rise in the next year. Its data goes back to 2002.

Famously Joseph P. Kennedy, father of US president John F. Kennedy, sold all the stocks he owned just before the 1929 Wall Street Crash after a bellboy in a hotel began offering him stock tips.

He decided if the bellboy was buying stock then it would be difficult to find someone who was below this lowly position to buy shares and keep the stock market momentum going.

At this stage in the proceedings, investors are often not focused on the possibility of losing money or the strengths and weaknesses of individual listed companies and instead fret about missing out on a potential opportunity.

We don’t believe we’re at this stage yet… but it might not be too far away.

Are stocks expensive or cheap at present?

The valuation of equities (also known as stocks and shares) in developed markets looks stretched. According to research published this summer by private equity firm STAR Capital they trade on an average price-to-earnings ratio of 21, significantly higher than the long-term average.

Against this backdrop, any bit of news which falls short of high expectations could act as the trigger for relevant companies to experience sharp declines in their share price.

An acceleration of this trend could start to weigh on investor sentiment and cause people to start reducing their exposure to the higher valued parts of the market.

CENTRAL BANKS

CENTRAL BANKS

Central banks in Europe and the US are at different stages of scaling back quantitative easing (QE) and returning interest rates to more normal levels.

QE involves central banks buying assets, usually government bonds, from investors such as banks or pension funds with money they have created electronically. This increases the amount of money in the financial system, thereby enabling financial institutions to lend more to businesses and individuals and hopefully stimulate economic activity.

The US is further along in the process of taking its economy off QE ‘life support’. The country halted its QE programme in October 2014 and started raising interest rates in December 2016.

In contrast, the European Central Bank (ECB) has extended its own QE programme until the end of 2017.

There is now discussion over when the US Federal Reserve will start selling back assets purchased during QE.

WHAT DOES ALL THIS MEAN?

There are several implications for financial markets but arguably the bigger impact is likely to be felt by fixed income or bond investors.

Invesco Powershares says investment returns will be lowered if central banks are not buying assets. It adds: ‘There is some evidence to suggest this may be the case and we suspect those assets that have been the most distorted by QE policies (fixed income, in our opinion) will be the worst affected when QE stops or is reversed.

‘This is an important factor behind our preference for equities and real estate over fixed income.

‘Even the US equity market, the valuation of which worries us, tends to keep rising until the Fed stops raising rates, which usually happens around the time that unemployment bottoms out.’

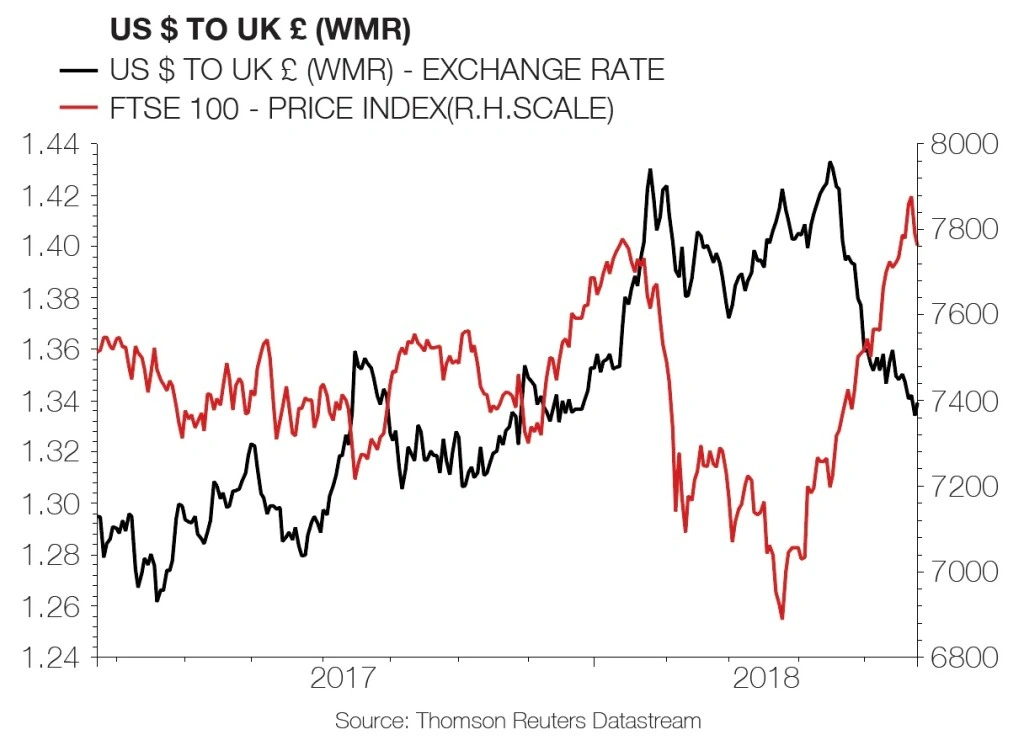

As the Bank of England increases interest rates, it could have further implications due to the impact on the pound and the relationship of the UK currency with the FTSE 100.

Higher rates will typically increase the value of a country’s currency. The increased return on offer attracts foreign investment, inflating demand and the value of the home country’s currency.

And as JP Morgan Asset Management’s global market strategist Nandini Ramakrishnan explains: ‘The price of sterling affects the revenue streams of the FTSE 100 companies in the UK quite significantly.

‘The lower the pound gets, the more attractive these multinational large cap companies’ exports appear to the rest of the world (because large caps are selling globally rather than to UK consumers). If sterling strengthens, we would expect small and mid-cap UK stocks to outperform the FTSE 100.’

That’s already in play as we speak with the FTSE 250 index up 7.5% year to date versus 1.8% gain from the FTSE 100. Sterling is currently staging a comeback against the dollar with approximately 15% appreciation so far this year.

EARNINGS THREAT

A weaker pound last year increased the relative value of earnings from outside the UK, which account for 70% of the total earnings from the FTSE 100.

The current reversal of this trend could lead to earnings downgrades as analysts adjust their currency expectations. Indeed, stalling earnings momentum is one reason why the FTSE 100 has slipped from record levels in recent weeks.

‘The spring’s march to a fresh record peak above 7,500 coincided with strong increases to analysts’ consensus earnings expectations, themselves the result of the slide in the pound following the June 2016 EU referendum vote,’ says AJ Bell investment director Russ Mould.

‘While the pound inched lower over the summer, analysts have stopped nudging their forecasts higher – and actually started cutting them, at least for 2017.’

Mould notes that following increases to FTSE 100 pre-tax income forecasts for 2017 in the second, third and fourth quarter of last year and the first quarter of this year, estimates flattened out in the second quarter and then slid by 3% in the third quarter.

He adds that estimates for 2018 profit have been flat at around £213bn for the last two quarters. And that is not just due to currency.

Profit warnings from WPP (WPP) and Provident Financial (PFG) will not have helped but they represent less than 1.5% of the FTSE 100’s aggregate earnings.

There appear to be three bigger factors at work:

The accompanying table shows the dominance of banks, oil and gas companies and miners in terms of earnings delivered by the FTSE 100.

Investors in products such as exchange-traded funds which track the FTSE 100 need to ensure they are comfortable with their disproportionate exposure to these sectors.

DEBT WARNING

Another cause for concern regarding the health of the stock market and investor sentiment is consumer debt in the UK which has hit pre-credit crunch levels.

The head of the Financial Conduct Authority Andrew Bailey has sounded the alarm on the £200bn in unsecured consumer credit amassed by UK households. The Money Advice Service says there are now 8.3m people in the UK living with problem debts.

This has implications for consumer facing stocks if Britons feel compelled to tighten their belts – something we’ve discussed in Shares many times this year.

The risk to the wider market is from some form of contagion from these mounting debts. However, warnings on car financing personal contract plans (PCP) being comparable with the subprime housing bubble are far-fetched.

And financial institutions and the corporate sector as a whole have stronger balance sheets than they did in 2007.

More concerning is the dependence of the Chinese economy on debt. The International Monetary Fund says: ‘International experience suggests that China’s current credit trajectory is dangerous with increasing risks of a disruptive adjustment and/or a marked growth slowdown.’ This could have a more material impact on stock markets around the world.

Ben Kumar, Investment Manager, 7IM:

‘We haven’t seen a US-led slump for some years, and it may cause investors some concern. Ultimately, the global growth train will keep going, but we believe that now is a sensible time to be pulling back from expensive equity markets and keeping some cash ready to invest on a meaningful pullback.

‘At the same time, we maintain an allocation to the high growth regions such as emerging markets. If we are wrong about a US wobble occurring, companies in the less developed regions should continue to appreciate strongly.’

Richard Champion, Deputy Chief Investment Officer, Canaccord Genuity Wealth Management:

‘It’s a very long lasting bull market whether you take the last time the market fell by more than 10% or the aftermath of the global financial crisis as the starting point.

‘For UK-based investors, returns look like they are going over the top thanks to sterling rallying sharply in the last few weeks.

‘Sterling depreciation last year gave the UK a good push up. The UK market as a whole is being impacted more than usual by currency moves. From a world stock market view, I don’t see much evidence of markets topping off.’

James Dowey, Chief Economist and Chief Investment Officer, Neptune:

‘This bull market is underpinned by a lot of support from central banks, who have bought huge amounts of financial assets. If the bull market is to continue, central banks must withdraw this support very slowly and carefully indeed.

‘If they do that, then corporate earnings growth can do the day-to-day work of gradually pushing up the level of the stock market over time.

‘The central banks do not want a bear market, so problems will only arise if the gradual removal of support comes into conflict with higher priority concerns, i.e. if inflation picked up very strongly or if lending started to look reckless again.’

John Bilton, global head of multi-asset strategy, JPMorgan Asset Management

‘Investors should remember that while valuation matters a great deal over a long-term horizon (10 to 15 years), in the short term (under a year) valuation is not an especially strong determinant of returns.

‘So in sum, are valuations rich? Yes, a little. Are we expressly concerned as a result? No, because although corrections can happen during equity bull markets, we see limited risk of a recession over the next 12 to 18 months and so would view any dip in markets as a potential buying opportunity.’

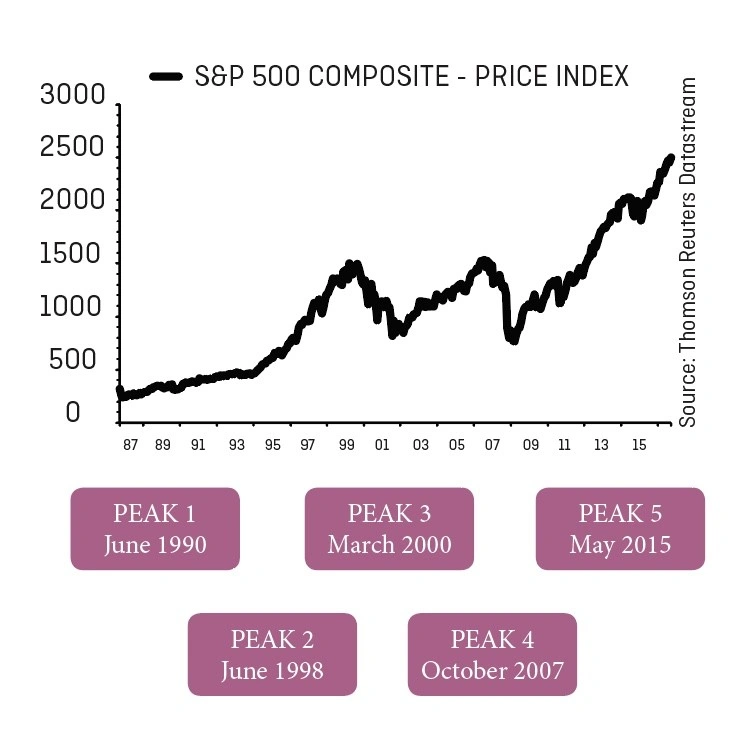

John Lonski, chief economist at Moody’s Capital Markets Research, says: ‘The equity market’s five other episodes of at least a 10% drop from the relevant record high followed peaks that were established in May 2015, October 2007, March 2000, June 1998, and June 1990.

‘Two of the deep declines did not occur in the context of a recession, namely the most recent correction of 2015-2016 and the brief, but severe, setback of 1998’s second half.

‘Compared to their previous highs, the market value of common stock sank by -12.9% before bottoming in February 2016 and fell by -13.7% before bottoming in September 1998.

‘In addition, 15 months passed before the equity market set a new record high in August 2016, while it took only five months for equities to establish a new high in December 1998.’

THE STEPS TO TAKE

By Patrick Connolly, head of communications at financial planning firm Chase de Vere

1. Multi asset approach

Nobody can consistently call or time stock markets. Those who try may well have expected markets to fall following the EU referendum result or after the election of Donald Trump, but they kept going up.

It is therefore important that investors don't try to be too clever.

You should spread your money across different assets such as equities, fixed interest, commercial property and cash. Make sure this is in the right proportions to meet your objectives and attitude to risk. This can be achieved by investing in a diversified range of investment funds or even a single multi asset fund.

2. Stay calm and rational

It is really important to stay calm and rational.

Investors will achieve better long-term returns and ride through the difficult times by staying calm, adopting a long-term strategy and sticking to it without being distracted by all of the short-term noise.

This means that if your investment strategy was right for you before it is probably still right for you today.

3. Regular premiums

Investing money on a regular basis (rather than lump sums) is a sensible way to invest during difficult economic times or periods of stock market volatility.

This approach negates the risk of market timing and means that if investments fall in value then units are simply bought cheaper next time, bringing down the average purchase cost.

4. Rebalance regularly

To ensure that you don’t end up taking too much, or too little, risk, you should look to rebalance regularly. This involves selling some of your investments which have performed well and now represent a larger proportion of your portfolio and reinvesting into those which have performed poorly and are now a smaller amount of your portfolio. This will help to get you back to your starting position.

If one year ago you had invested £10,000 in each of Chinese equities, European equities, UK equities, UK corporate bond and UK gilt funds, you would now have £12,630 invested in China, £12,280 in Europe, £11,290 in UK equities, £10,170 in corporate bonds and £9,640 in UK gilts, changing the risk profile of your portfolio.

Not only does rebalancing ensure you don’t take too much risk, but by selling investments that have done well in favour of those that have done badly you are effectively selling at the top of the market and buying at the bottom. This is the holy grail of investing and something which very few investors consistently achieve.

By sticking to this method you can avoid the emotional input that leads to many investors buying or selling based on sentiment and probably getting these decisions wrong more than they get them right.

FUNDS FOR CAPITAL PRESERVATION

Investors concerned about the potential for market volatility could consider investing in funds whose priority is not to lose money.

Example include Jupiter Strategic Reserve (GB00B7KKF583) and JP Morgan Multi-Asset Income (GB00B4N20M25).

The Jupiter fund was launched in April 2012 and until recently was managed by the experienced Miles Geldard who had a track record of preserving capital through several market cycles.

Geldard is now stepping back to an advisory role with Lee Manzi taking over as manager.

The portfolio he inherits is spread across bonds, equities, convertibles, currencies and alternative assets and takes short and long positions to defend its capital position.

The JP Morgan fund aims to provide income by investing in a global portfolio of income generating securities such as shares, bonds and real estate investment trusts (REITs).

It looks to achieve the best possible risk-adjusted income, which can be taken monthly, quarterly or reinvested for growth.

The current yield is 3.6% and while income is the main objective, the fund also targets capital preservation and low volatility by investing in a diverse selection of around 1,500 underlying holdings.

THE CASE FOR REMAINING INVESTED

It is important not to overreact to what is happening in the wider market. You could cash in some of the higher risk investments in your portfolio and keep the proceeds to one side to take advantage of any opportunities created by a correction should one happen in the near future.

Having some cash at the ready looks a wise move, in our opinion. Just don’t be tempted to trade in and out of the market on a regular basis.

JP Morgan Asset Management’s global market strategist Nandini Ramakrishnan says: ‘Timing the market for those perfect sunny days is especially hard, given that some of those best days occur right after the worst days. The market is volatile, and jumping in and out of it has its costs.’

Research by asset manager BlackRock shows how a hypothetical £10,000 investment in the FTSE All Share would have been affected by missing best-performing days over a 20-year period from 1995 to 2015.

Missing just the five best days would have reduced the final pot from £45,519 to £31,316. Missing the best 15 days more than halves the hypothetical return and missing 25 days leaves you with just £13,506.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- Big news in the banking sector

- Gambling stocks in focus ahead of Government review

- Cobham appoints former Airbus UK chief

- MJ Gleeson is one of our top picks among housebuilders

- What next for investors after German elections?

- Central Asia Metals’ zinc move makes the stock higher risk

- UK hotel growth to decline in 2018