Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineThe smaller housebuilder with really big potential

The majority of housebuilders on the London Stock Exchange are large companies, some even big enough to be in the FTSE 100 index.

Many investors tend to focus on the top players, yet in doing so we believe they are missing out on interesting opportunities further down the market cap spectrum.

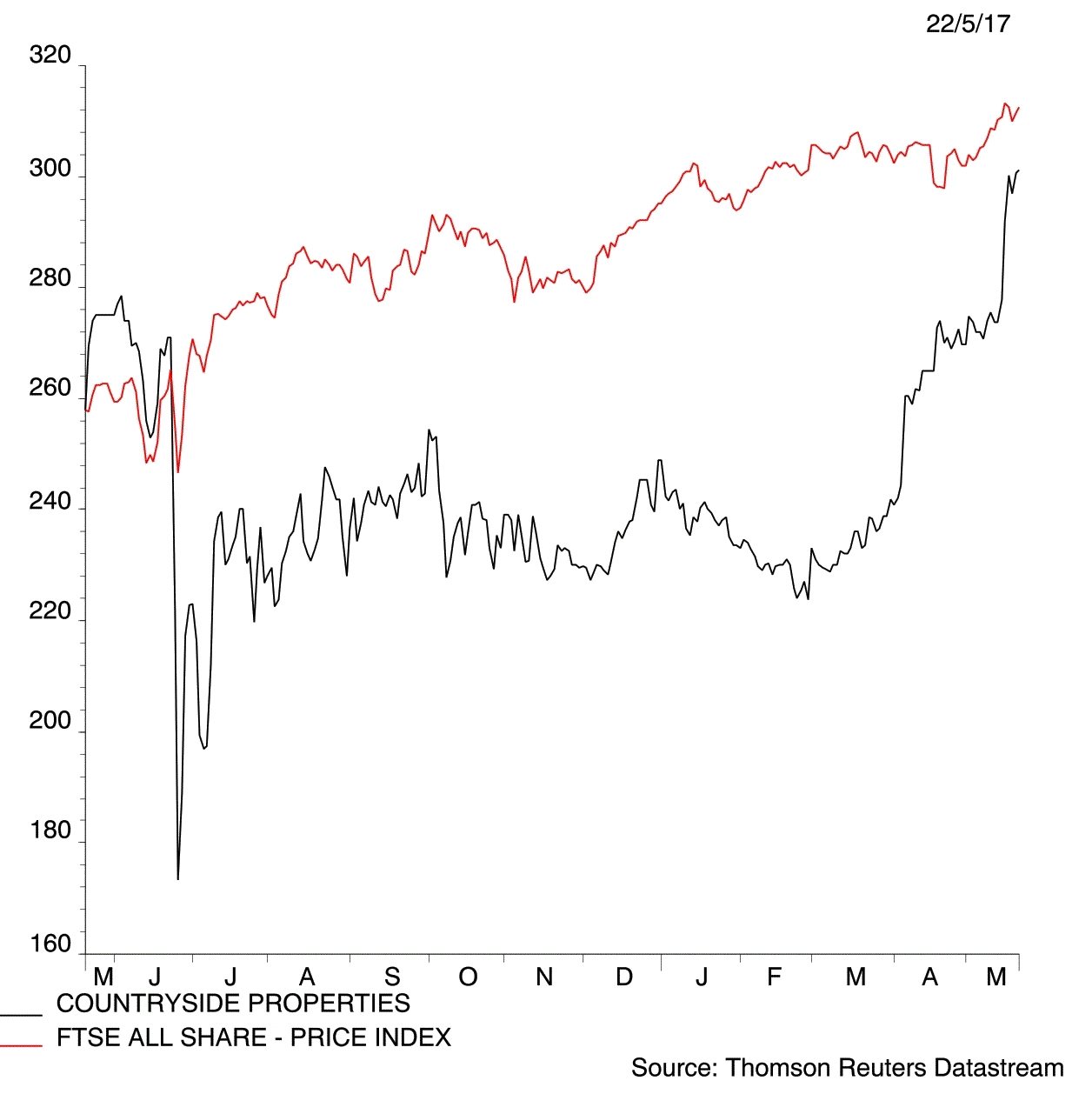

One example is FTSE 250 constituent Countryside Properties (CSP) which trades at a material discount to the sector despite brighter growth prospects and a business model which should limit downside if the housing market goes into reverse.

At 301.2p the shares trade on 8.8 times investment bank Berenberg’s 2018 earnings per share forecast of 34.1p, some way behind the sector average of 9.7 times.

Dynamic market

We think the dynamics behind the housebuilding market remain positive for now.

Although there are some signs of house prices softening, demand for houses is still running ahead of supply, mortgage availability remains high and political support remains strong.

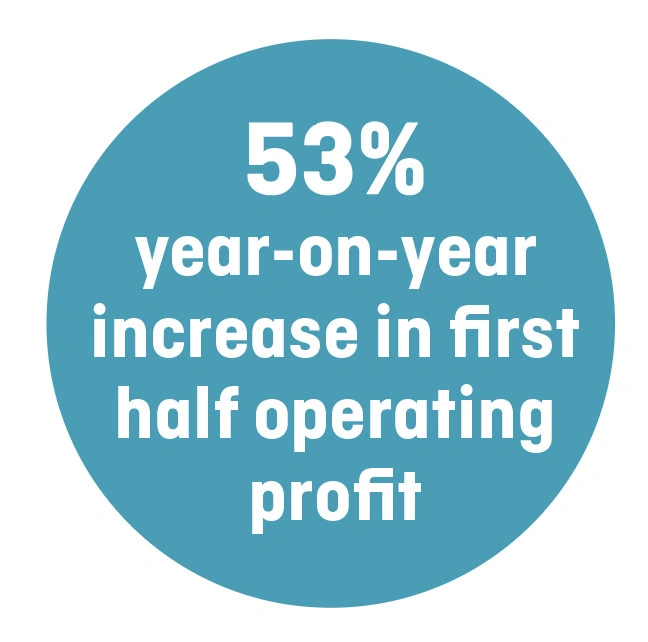

Countryside’s half year results on 17 May saw completions jump by a third to 1,437. As a result, its adjusted operating profit was up from £50.8m a year ago to £70.4m.

Reported revenue was up almost a quarter (23%) at £351.1m and reported operating profit rose by 53%

to £53.2m.

The company splits its operations into two key divisions. One is the so-called ‘normal’ housebuilding, which includes its eponymous Countryside franchise and high end Millgate brand. The other is its partnerships division which was a big driver of its impressive first half performance.

Better together

The latter operation, which sets it apart from the majority of its peers, services landowners that want to develop land and build residential houses and whom need partners to achieve it.

A typical customer will be a local authority with land which is run down and potentially contaminated, and which has a mandated housing supply need to meet.

This activity is very profitable for Countryside as it can often gain advantageous terms on the purchase of this land.

It should also hold up well if the UK economy takes a turn for the worse, as Berenberg notes: ‘Since local authorities were restricted from new housebuilding in the early 1980s they have continued to supply new housing at a low level.

Peel Hunt forecasts Countryside will increase its housebuilding volumes by 70% in the three financial years to September 2019 to 4,595 units.

The broker has a 395p price target for the shares, implying 31% upside over the next 12 months. Countryside also has a 3.4% prospective dividend yield. (TS)

Countryside Properties (CSP) 301.2p

Stop loss: 210p

Market value: £1.36bn

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.