Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineHealthy and wealthy: Pharma’s top league

We believe large pharmaceutical stocks are starting to look interesting again. Evolving drug pipelines, the approval of new treatments and greater confidence in future earnings growth all suggest investors should take another look at the sector.

We’re coming out of a tough few years for drug companies, rocked by political intervention with price cap threats and many firms losing patent protection on blockbuster drugs.

Although there continues to be the ongoing risk of drug development failure, we feel sentiment is starting to improve towards the really big companies.

The market fundamentals are still very positive. An increasingly ageing population around the world will need more care, plus growing middle class in emerging markets will drive additional demand for healthcare products.

No single company tackles every disease, so you may wish to create a portfolio of pharma stocks to provide diversification.

In this article we explore seven large cap pharma stocks and explain their areas of specialism.

We also talk to various investment managers about why they’ve invested in one or more of these stocks for their fund(s).

How to invest

Three of these companies are listed in London. The remainder trade on different stock markets such as the New York Stock Exchange. Most UK stockbrokers or investment platform providers will facilitate trading in these stocks.

We appreciate not everyone wants to directly invest in overseas-listed shares, so we’ve added information on funds available in the UK which invest in the seven large cap pharma stocks.

As a final introductory note, it is worth clarifying that there are many other large cap pharma stocks beyond the ones in our discussion. We don’t have the space to discuss everyone; instead, use this article as a platform to do your own further research if you find the sector interesting.

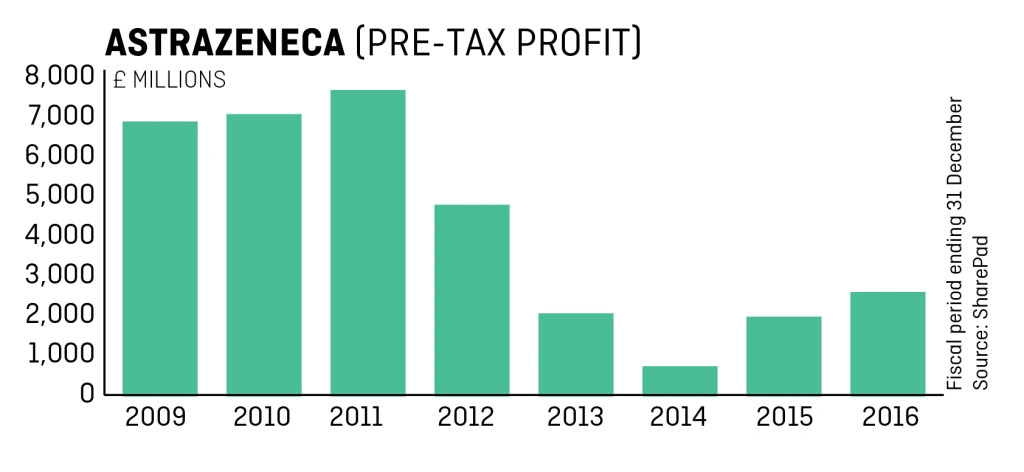

AstraZeneca (AZN) £51.44

AstraZeneca produces medicines to treat cancer, the nervous system, heart or blood vessels, as well as diseases affecting the stomach area.

A breakthrough for AstraZeneca’s lung cancer drug Imfinzi recently hit the national news headlines. The drug significantly reduced the risk of the disease intensifying or leading to death.

Berenberg analyst Alistair Campbell estimates US potential sales for Imfinzi of over $2bn, providing a blockbuster opportunity.

Making a comeback

M&G UK Income Distribution (GB0031107021) fund manager Hughes is impressed by AstraZeneca’s renewed focus as five years ago it suffered from poor management.

Then-CEO David Brennan focused on smaller acquisitions and licensing deals. He was also criticised for paying too much for MedImmune in 2007 ($15.6bn) and failing to replenishing AstraZeneca’s drug pipeline.

Under pressure from shareholders, Brennan quit in April 2012 and was replaced by former Roche chief operating officer Pascal Soriot.

Hughes says Soriot has worked hard to ‘reverse the previous CEO’s mistakes’ by focusing on developments in cardiology, cancer and neuroscience.

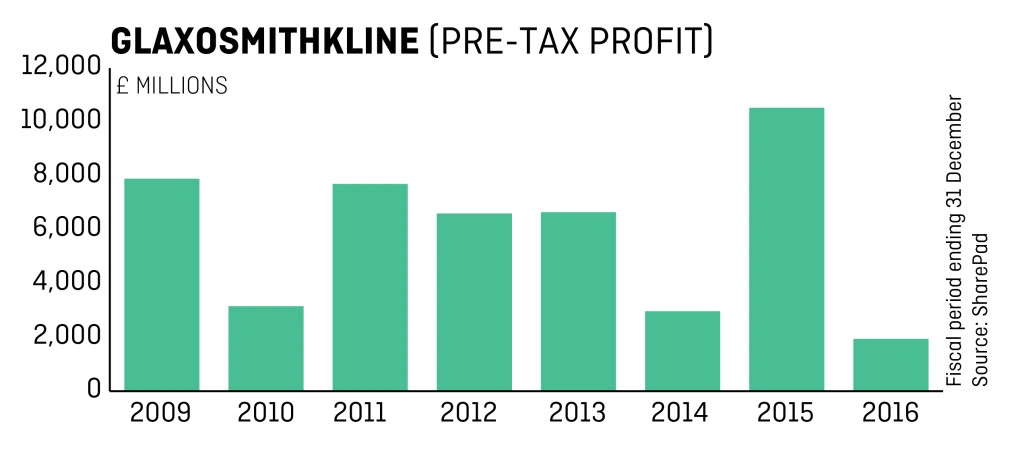

GlaxoSmithKline (GSK) £16.44

You may know of GlaxoSmithKline through its range of everyday products, whether you use Aquafresh toothpaste or Nicorette gum to kick that pesky smoking addiction.

The company also researches, develops and manufactures medicines to tackle cold sores or headaches, as well as vaccines to fight diseases such as meningitis.

Over the last three years, £9.8bn was pumped into research and development (R&D) and it generated £15.4bn in sales over the same period from existing products.

Liontrust Special Situations (GB00B57H4F11) fund manager Anthony Cross has been a long-term fan of GlaxoSmithKline. He likes the way it earns backs the cost of R&D, plus excess money on top, throughout the life of a drug which has patent protection.

‘Key examples in recent years include anti-ulcer medication Zantac and respiratory treatment Advair,’ he says.

The fund manager believes the market underestimates the cash flows accruing from R&D and subsequent product creation, even when the drugs in question lose their patent protection – something which is also known as ‘going off-patent’.

Pharma companies use patents to stop competitors from producing cheaper versions of their drugs for a specific amount of time.

After a patent expires, sales can drop sharply as a firm’s rivals release generic versions of its products for a lower price, which hits profit margins as the company has been forced to cut prices.

As for GlaxoSmithKline, Cross is confident in the pharma giant’s ability to generate plenty of cash from its broader portfolio of products.

Admittedly, risks are on the horizon for GlaxoSmithKline’s HIV division as it faces competition from US-listed Gilead. This is very important as this division has been one of the big growth drivers for the business in recent years.

Positive study data was released in February on Gilead’s Bictegravir to treat HIV and the company believes its drug could offer a new treatment option with a high barrier to resistance.

Generous dividends ... are they sustainable?

Many investors own GlaxoSmithKline for its generous dividends – it typically yields in the region of 5%.

M&G UK Income Distribution fund manager Richard Hughes claims the pharma firm is committed to its dividend and boasts a growing consumer division, which includes anti-fungal treatments.

He says Emma Walmsley’s recent appointment as GlaxoSmithKline’s chief executive officer is a welcome change and believes she is the right person to guide the company forward.

Walmsley has a wealth of experience as she led the consumer healthcare division, a joint venture between GlaxoSmithKline and Novartis, since 2010. She previously worked for French cosmetics firm L’Oreal for 17 years.

Not everyone shares Hughes’ optimism. Fund manager Neil Woodford recently sold his stake in GlaxoSmithKline due to concerns about the company’s drug pipeline, weak balance sheet and dividend sustainability.

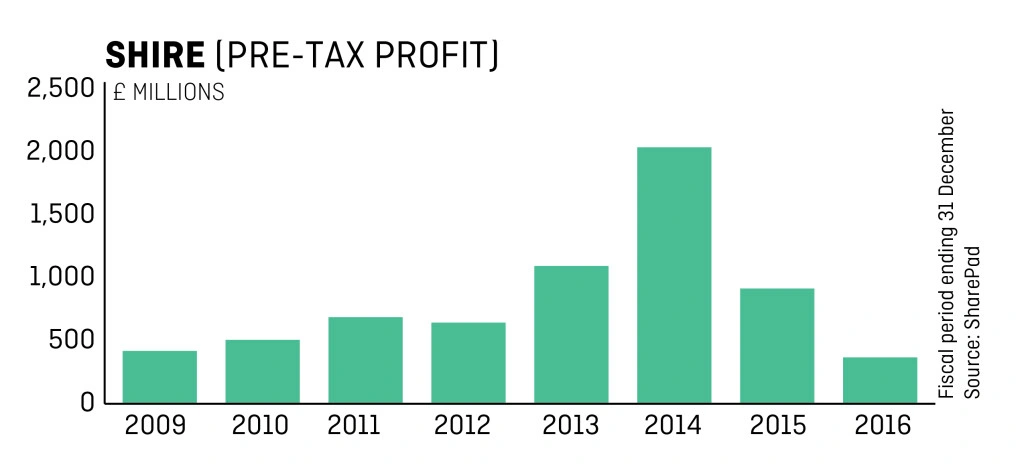

Shire (SHP) £48.19

Shire works in the rare diseases space, which targets a small number of patients – specifically less than five in 10,000 of the general population, according to the EU.

The stock features in several fund portfolios including Castlefield UK Opportunities (GB00B1XQN911). Fund manager Mark Elliott believes the market is undervaluing the company. ‘We feel that earnings will likely be much more resilient than many seem to anticipate.’

Shire’s share price was weak in the run up to the US election last year as investors worried about its high exposure to the country (it generates about 60% of revenue from the US). Presidential candidate Hillary Clinton had been particularly vocal about her desire to clamp down on high drug prices.

Donald Trump’s surprise election victory triggered a recovery in Shire’s share price – although it has been fairly volatile for much of 2017.

It received a boost in mid-May after saying its SHP643 drug for hereditary angioedema (HAE) had been successful in a late-stage study.

Bank of America Merrill Lynch analyst Graham Parry says the data confirms Shire’s best-in-class properties and potential to represent $2bn in sales for its HAE franchise in 2023.

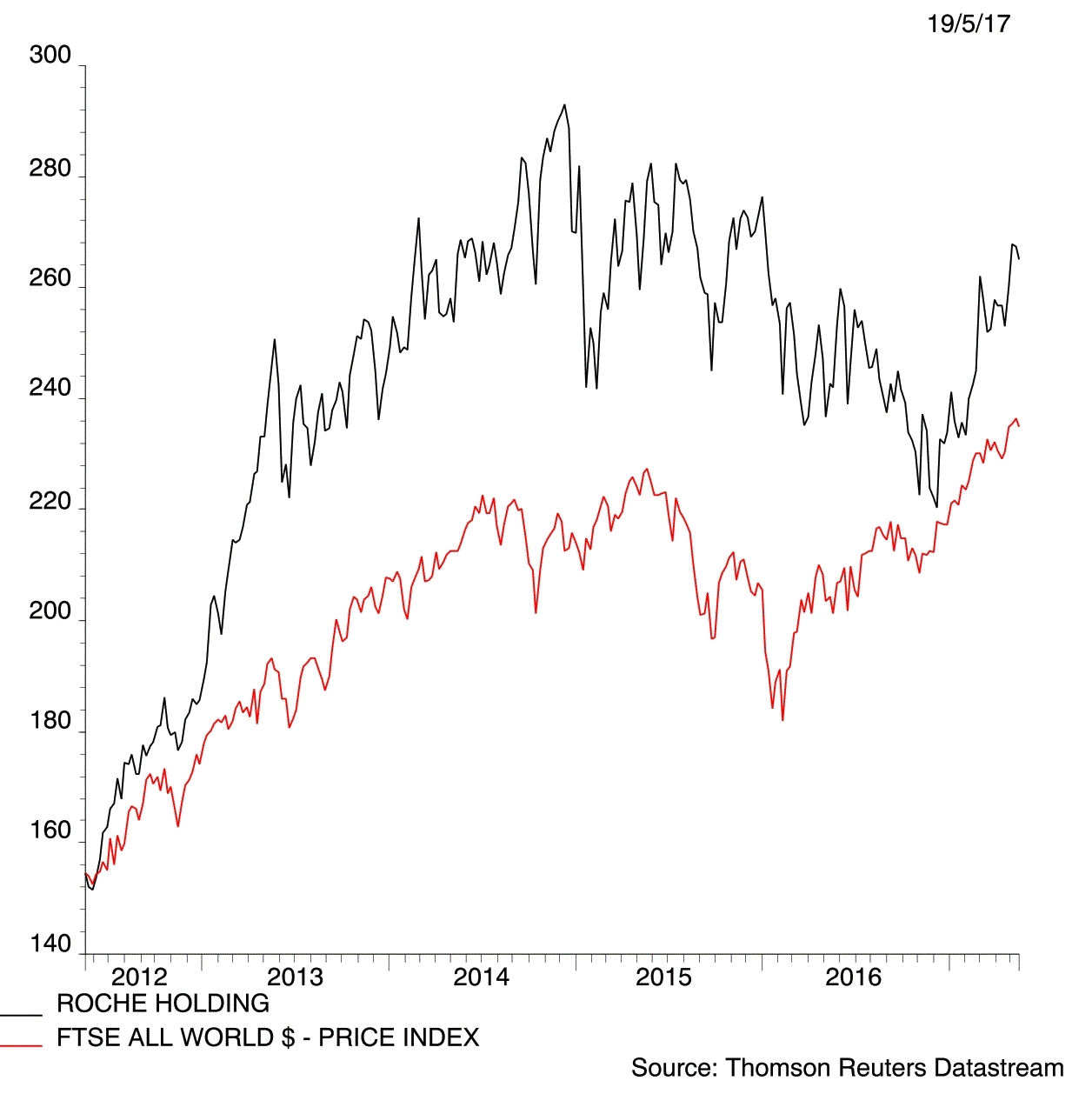

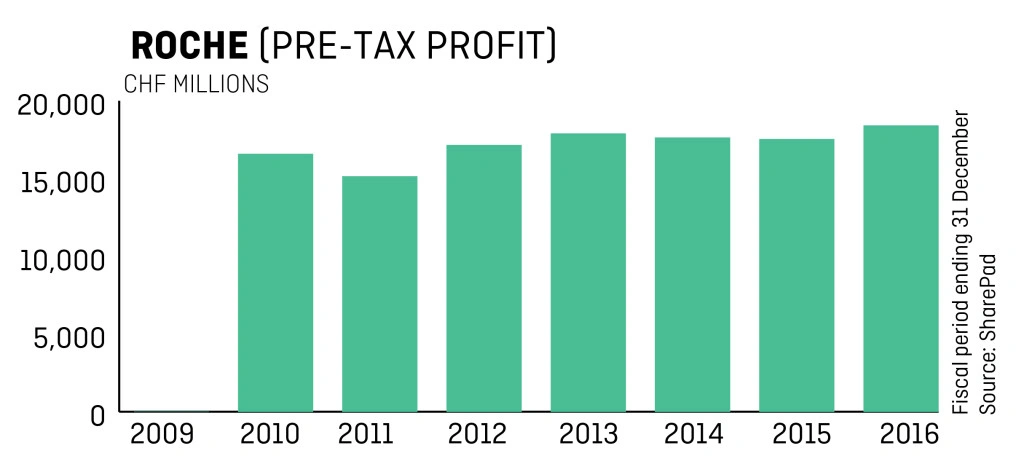

Roche (CHF) 267.2

Roche aims to tackle cancer, inflammation, diabetes and viral diseases such as chickenpox and flu through its pharmaceutical and diagnostic offerings.

Its diagnostic products include blood-based self-monitoring systems, while the division can identify specific types

of diseases.

Saracen Global Income and Growth (GB00B8MG4091) fund manager Graham Campbell likes Roche because of its good history of releasing new cancer drugs and a strong pipeline.

Roche is undervalued according to Campbell as investors are overlooking the sheer number of drugs and diseases it tackles, as well as its potential to generate billions in revenue.

Baillie Gifford Global Income Growth (GB0005772479) also has a holding in Roche as co-manager James Dow believes it has the best scientific team to tackle cancer. He is also confident in its ability to deliver growth and a new pipeline of drugs.

Sanofi €88.32

Sanofi is a global life sciences company that develops drugs to treat rare diseases, multiple sclerosis, cancer and diabetes.

Chris Hiorns runs EdenTree Amity European (GB0008448333) and is a fan of Sanofi thanks to its strong position in vaccines and diabetes.

For a pharma stock to reach his coveted top 10 holdings, they need decent valuation, a good balance sheet, strong dividend yields and cash generation, as well as a low price to earnings ratio. Sanofi ticks the right boxes.

Johnson & Johnson $126.58

You’ll probably know Johnson & Johnson for its baby wipes and Neutrogena face wipes. But the company is also a big player in the pharmaceutical world, aiming to treat cancer

and infectious diseases.

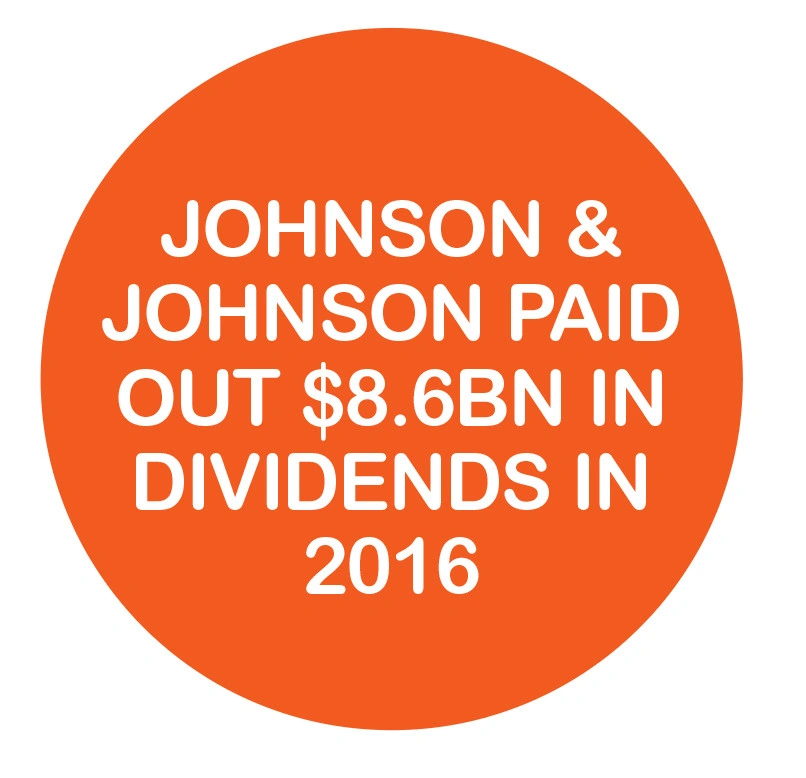

Baillie Gifford managers Dominic Neary and James Dow are enthusiastic about its outlook. Dow is confident that management are ‘genuinely committed to innovation’ rather than cost-cutting measures and mergers. He says: ‘Johnson & Johnson has a fantastic record of earnings and dividend growth – not all can do that.’

In 2009, the company paid $1.93 per share ($5.3bn in total) in dividends. The dividend had increased to $3.15 per share ($8.6bn) in 2016.

He thinks that Johnson & Johnson is suitable for investors looking for income and growth potential with a ‘moral compass’. Johnson & Johnson is driven by its credo of doing the right thing to support nurses, doctors and patients, instead of chasing profit.

By 2019, the company aims to have filed 10 new products for regulatory approval, all of which have the potential to exceed $1bn in sales according to investment experts.

Johnson & Johnson has already gained regulatory approval for three new drugs. These include active rheumatoid arthritis medicine Sirukumab and plaque psoriasis treatment Guselkumab.

Merck $63.76

Merck creates medicines, vaccines and animal health products. It is working with Pfizer to develop the antibody Avelumab to find and attack cancer cells.

Campbell at Saracen is optimistic that Merck’s prescription medicine Keytruda has huge potential to tackle a specific type of skin cancer called melanoma. The medicine generated approximately $1.4bn of sales in the year to 31 December 2016.

According to Campbell, the drug is expected to grow significantly with $6.5bn in revenue forecast over the next five years.

Hiorns at Amity is also keen on Merck, saying it is a diversified business that specialises in life sciences to provide solutions such as chemical reagents, as well as specialty chemicals for LCD TV screens.

INVESTING IN THESE STOCKS VIA FUNDS

The aforementioned large cap pharma stocks appear in many different funds available to UK investors.

For example, anyone wanting to own both AstraZeneca and GlaxoSmithKline could do so via Liontrust Special Situations or M&G UK Income Distribution.

The Liontrust fund has delivered 15.5% annualised returns over the last five years. It identifies companies with intangible assets that produce barriers so they can beat rivals and sustain higher profitability.

Alongside the two drug companies are stocks from various other sectors such as oil producer BP (BP.) and drinks giant Diageo (DGE).

If you don’t want the broad sector exposure, look for a more specialist fund. For example, Polar Capital Global Healthcare Growth and Income (PCGH) has Merck, Sanofi, Roche, GlaxoSmithKline and Johnson & Johnson in its top holdings.

Fund manager Dan Mahony looks for diversified companies with strong balance sheets, as well as free cash flow growth for dividends, share buybacks and acquisitions.

The fund has delivered 15.6% annualised total returns to shareholders over the past five years. (LMJ)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.