Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

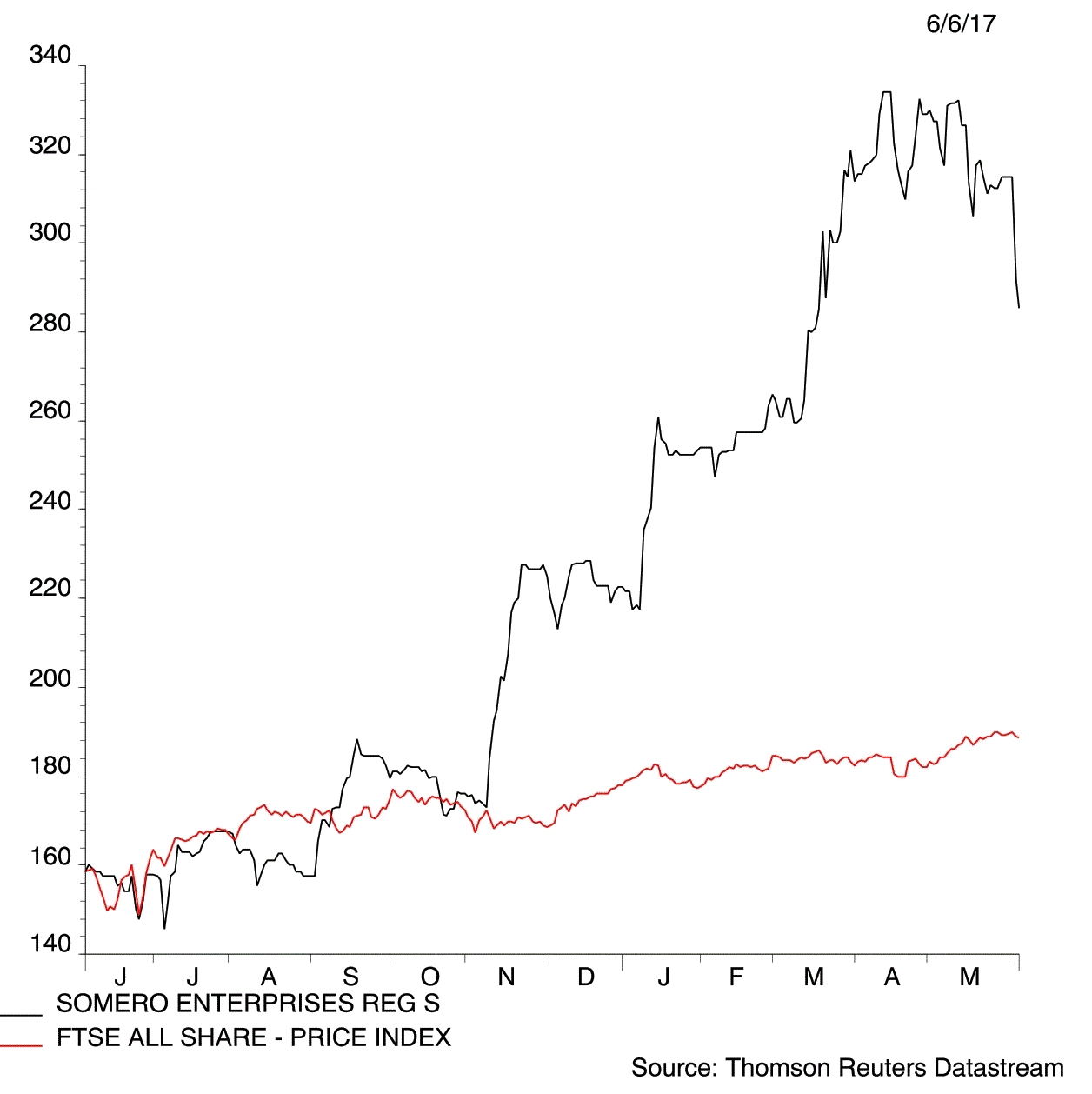

magazineSomero looks ripe for a takeover offer

Rising profit, elimination of debt, generous dividends and potential for an additional special dividend later this year; what’s not to like about Somero Enterprises (SOM:AIM)? We view it as a superb investment and a potential takeover target.

The concrete levelling equipment specialist sells into 93 countries. North America represented 71% of sales in 2016.

US President Donald Trump’s desire to improve the country’s infrastructure, stop relying on imports and reduce corporation tax could have a positive knock-on effect for domestic construction activity and therefore benefit Somero.

American companies could have more money to reinvest in their business such as building new factories or warehouses. A growing economy could also encourage more commercial real estate development.

Somero’s equipment is used entirely in the commercial non-residential sector. ‘Our kit is used when building new schools, offices, warehouses and retail outlets,’ says CEO Jack Cooney.

What does Somero do?

Its kit allows customers to install high-quality horizontal concrete floors faster, flatter and with fewer people. ‘Concrete is difficult; it sets in an hour and is a perishable. It is very expensive to move once set,’ says Cooney, explaining why customers need reliable equipment and good back-up support.

Growth isn’t restricted to the US. Investments have been made by Somero in China and India. Activity is picking up in Brazil and it says the outlook is good for the Middle East and Australia among other locations.

Healthy position

Pre-tax profit increased by 22% in 2016 to $21.3m. The business recently paid off its debt and it had a $20.2m net cash position three months ago. The balance sheet is particularly strong thanks to a large cash pile and plenty of property-backed assets.

The company has a policy to maintain at least $10m net cash position. Any additional cash will primarily be used for acquisitions or product development.

Cooney tells Shares that Somero has struggled to find suitable acquisition opportunities but it is trying. ‘We want something existing customers would use and that isn’t a commodity-type product.’

The board will meet in the first half of the year to assess spending requirements and decide whether to return some extra cash to shareholders as a special dividend in the second half of the year.

Somero isn’t risk-free as it serves cyclical markets. But as things stand today, a business with growing profit, excess cash, a strong balance sheet and operating in positive market conditions would be an obvious takeover target, in our view.

‘We have private equity firms poking around all the time,’ reveals Cooney. ‘We actually had takeover interest 15 years ago from a business that is now part of German equipment group Wacker Neuson.’ (DC)

Somero Enterprises (SOM:AIM) 285.62p

Market value: £160m

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- 888 comes up trumps

- Argos saves the day for Sainsbury’s

- The fund which can help you beat inflation

- Setting the course for Brexit

- Has Royal Mail delivered for investors?

- Investor makes £2bn move on Anglo

- Watch NHS risk with Medica

- AstraZeneca to take a dose of Circassia

- Cheap mortgages could free up cash for investing

Editor's View

Great Ideas Update

Investment Trusts

Larger Companies

Main Feature

Smaller Companies

Story In Numbers

- 1.01%: BEST RATE FOR CASH ISA

- UK Media Companies

- FTSE 100 Stocks - Best Performing

- 2.1%: House price growth in East Midlands in top form

- $23 billion: Behemoth created by Vodafone India merger

- Hansteen disposal worth more than its market cap

- 15%: Rights issue might not solve Tullow’s debt problem

- 22%: Recruiter enjoys strong growth in Asia