Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineTime to pounce on small cap defensive earner

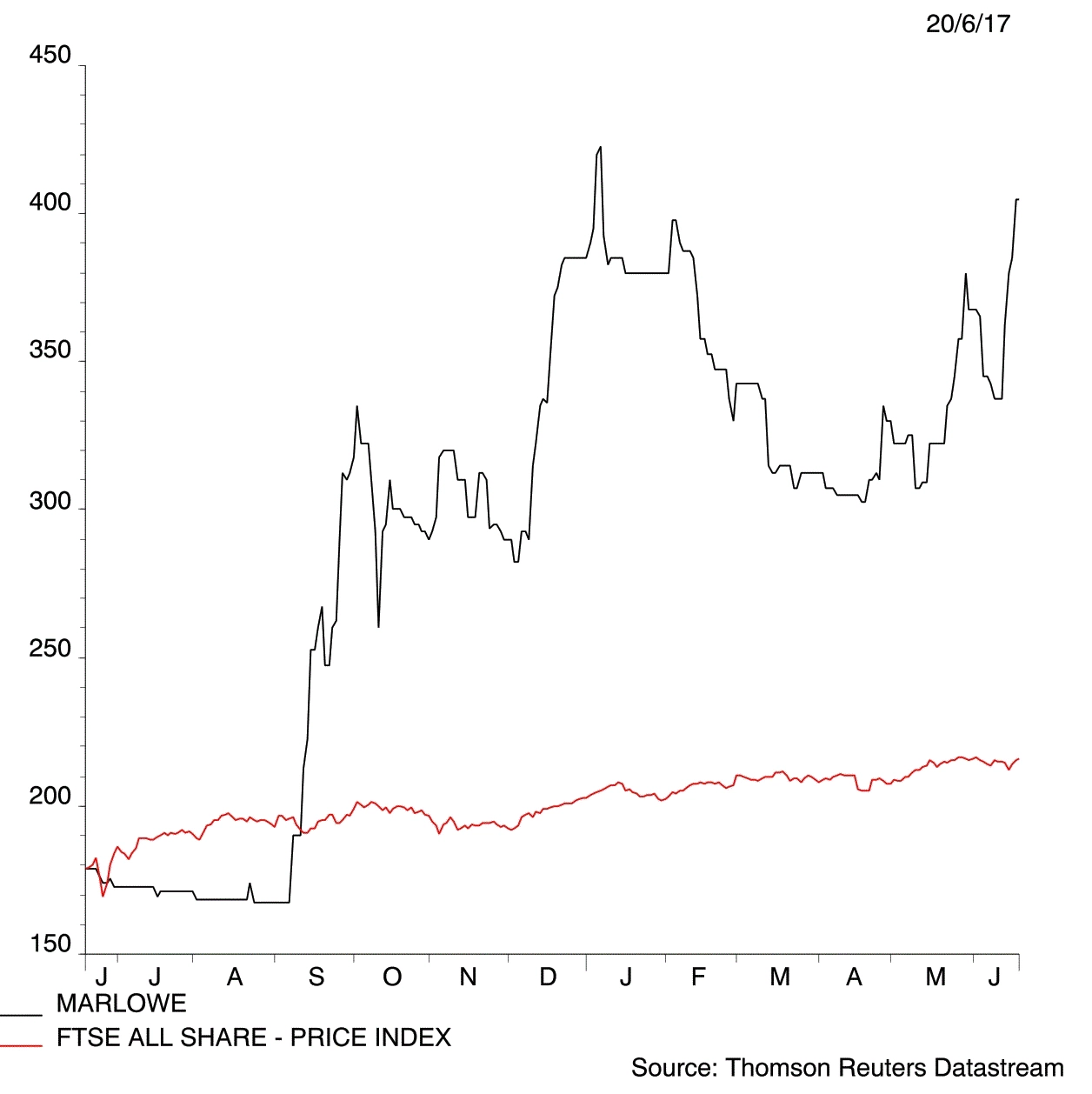

The 25% decline in fire and water services group Marlowe (MRL:AIM) to 310p over the past few months puts the stock at a much more attractive level for new investors, in our opinion.

Regulated markets

Marlowe is buying small businesses that serve heavily-regulated markets. Companies and organisations ranging from hotels and shops to universities and hospitals face very large fines if they don’t take measures to ensure people on their premises are safe.

Laws require property owners to regularly check their fire detection and fire alarm systems. On the water side, Marlowe helps to ensure third parties have clean water and check if areas such as showers in hotels or offices are harbouring waterborne diseases.

Marlowe operates in an area of non-discretionary spend. It also enjoys significant levels of repeat business as well as having some contracts lasting three to five years.

Of the eight acquisitions made so far, the average customer length is eight years in fire and seven years in water, says chief executive Alex Dacre.

Marlowe’s strategy is to create a national presence, improve operating profit and grow faster than the underlying market by taking business off rivals. It also wants to cross-sell additional services.

Off to the races

This plan is working. Dacre says the fire and safety services market is growing at about 2% to 3% a year. He claims Marlowe is achieving 8% to 9% organic growth, partially because the large service providers are too sleepy and slow to get anything done.

The company raised £10m last September at 170p per share to buy more businesses. It could have raised four times this amount judging by the orders from institutional investors.

A further £10m was raised in December at 290p, also oversubscribed. That’s a really interesting point; large investors clearly felt 290p was a great price at which to buy more shares – and the current price is only a fraction above this level, so get in now.

Dacre says many of the businesses being acquired by Marlowe have 10% operating margin. The company’s target is 15% operating margin, which the CEO claims is achievable through having more efficient operations and better IT support.

He claims Marlowe is buying companies fairly cheaply, typically paying four to six times earnings. ‘Many of these businesses were set up by entrepreneurs in the 70s and 80s. They’ve now reached the age where they want to sell and there aren’t many buyers in the market apart from us.’

He hopes to add a third leg to the business in the coming year, keeping the focus on critical asset maintenance.

Stockbroker Cenkos forecasts a maiden pre-tax profit of £3m for the year to 31 March 2017, rising to £4.8m a year later. (DC)

Marlowe (MRL:AIM) 310p

Stop loss: 217p

Market value: £95.8m

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- 888 comes up trumps

- Argos saves the day for Sainsbury’s

- The fund which can help you beat inflation

- Setting the course for Brexit

- Has Royal Mail delivered for investors?

- Investor makes £2bn move on Anglo

- Watch NHS risk with Medica

- AstraZeneca to take a dose of Circassia

- Cheap mortgages could free up cash for investing

Editor's View

Great Ideas Update

Investment Trusts

Larger Companies

Main Feature

Smaller Companies

Story In Numbers

- 1.01%: BEST RATE FOR CASH ISA

- UK Media Companies

- FTSE 100 Stocks - Best Performing

- 2.1%: House price growth in East Midlands in top form

- $23 billion: Behemoth created by Vodafone India merger

- Hansteen disposal worth more than its market cap

- 15%: Rights issue might not solve Tullow’s debt problem

- 22%: Recruiter enjoys strong growth in Asia