Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineEurope in a world of ‘alternative facts’

These are interesting times. Suddenly everything is different – populism has become protectionism under the mantra of ‘Make America Great Again’ and Brexit is set to lead the UK to sunnier climes. A few minor details, such as the interconnected nature of global supply chains and the relationships between companies and regions, are being forgotten for now.

Europe is in many ways now in the eye of the storm. The UK is stumbling along an undefined and unknown path towards Brexit, with the government promising no damage to the economy and full access to European trade, while not paying any bills. A few nervous dissenters, quickly shouted down by a partisan, right-wing press, are quietly asking ‘how?’

Pragmatism still dominates European politics

The political backdrop in Europe outside the UK continues to make everyone nervous. The Netherlands will be first to the polls in 2017, and the Far Right party of Geert Wilders will, like all European ‘alt-right’ parties at present, likely poll a significant number of votes on an anti-immigration bill. But Wilders will likely not be included in a coalition government when it comes to running the country.

As an aside, if there is a referendum in the Netherlands, the Dutch have made it quite clear that it would be advisory only. It is a pity that now ex-Prime Minister Cameron did not think through the potential risks of the UK referendum in June 2016. This was a point made by the Supreme Court in a recent ruling over how the UK government can start the process to leave the EU (Article 50).

France faces a key election in April and May, and there is a growing opinion that, even if Marine Le Pen of the extreme-right National Front party makes it through to the second round of voting in May, she is likely to lose out to either François Fillon (Republican) or Emmanuel Macron (Independent) in a repeat of the 2002 election, when her father lost convincingly to Jacques Chirac. Autumn sees the German elections, where it looks likely that Chancellor Merkel will be re-elected.

Is regional recovery taking hold?

The suggestion is that populism will not overthrow the European path of ‘boring but reliable’ economic progress. That may enable investors to look again at out of favour European markets and the improving trend in profits. Given that Europe’s gross domestic product (GDP) is expected to grow by about 1.5% in 2017, and that an improving economic climate is leading to more relaxed government spending, there is every reason to hope that Europe is now in a virtuous, rather than vicious, circle.

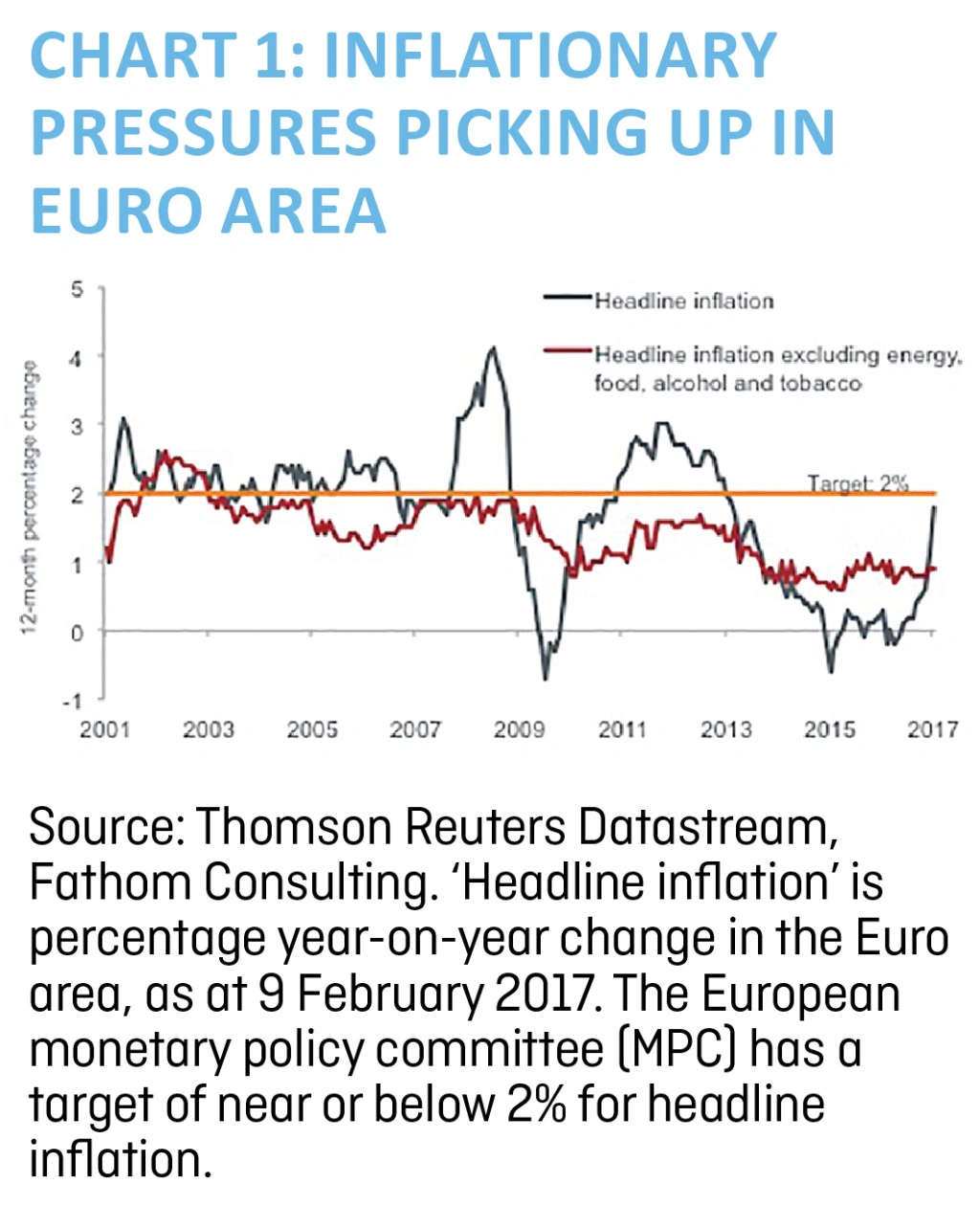

With a combination of better growth and emerging inflationary pressures (Chart 1), yields on 10-year bonds have risen to over 0.3% in Germany and over 2.3% in the US, as at 8 February 2017. This has major implications for banks and recovery names. It is clear that, regardless of intense global political uncertainty, the market has chosen to believe in the hope of economic recovery.

It remains to be seen how strong this recovery turns out to be, or how long it lasts, but it would be wrong to ignore it.

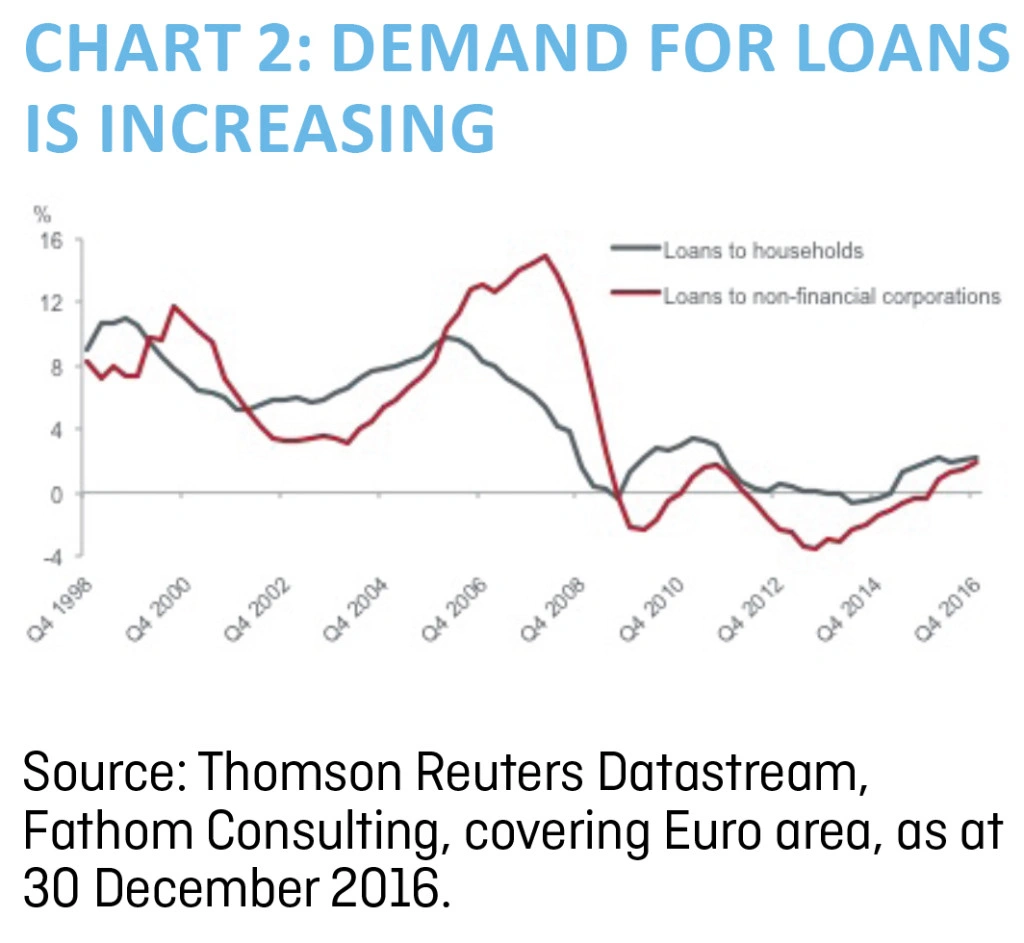

Companies more sensitive to changes in the background economy, such as Atlas Copco in Sweden and Siemens in Germany, are seeing an improvement in many areas related to higher consumer spending. Banks are seeing a widening net interest margin (the difference between the income generated from loans and the interest paid out to depositors), albeit a gradual one, and increasing demand for loans, as Chart 2 shows.

Markets have seen a rapid move out of ‘growth’, and into ‘value’. This is an over-simplification, but one that gives a reasonable gist of what is happening. This switch has pushed up the price of ‘value’ stocks to beyond their ten-year average, while valuations on growth stocks have fallen below theirs. This trend may have further to run, but the key to 2017 will be signs that the shift towards value has gone far enough, given the reality that growth in our ‘mature, low growth world’ cannot be conjured into existence like a magic trick.

There are significant hurdles ahead, but they are not yet visible. We are keeping a wary eye open, while looking for outstanding companies that have been penalised far too harshly by the market. We accept that it looks too early to make a significant move back into ‘growth’ yet, but that may well be the direction of travel on a six- to nine-month view.

THIS IS AN ADVERTISING PROMOTION - WRITTEN BY HENDERSON.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

Editor's View

Great Ideas Update

Investment Trusts

Larger Companies

Smaller Companies

Story In Numbers

- £24.3bn: Personal pension contributions break new record

- 15.7% jump in UK remortgage approvals in January

- Real Estate Investment Trusts

- FTSE All-Share Sectors

- 66%: Potential jump in IMI’s 2017 earnings per share

- 24%: US worst offender for cyber-attacks

- $6.47bn: Warren Buffett’s costly mistake

- 10 years: First dividend growth in a decade from Intu