Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhy infrastructure funds are flavour of the month

The UK Government’s Autumn Statement on 23 November is expected to signal a switch from monetary policy to fiscal stimulus. This would provide a much needed boost to the real economy and is likely to include more spending on infrastructure.

Infrastructure assets such as toll roads, airports, schools and hospitals are essential to the UK economy and the provision of these services is often contracted out to publicly listed companies. These heavily regulated businesses tend to generate steady earnings that rise in line with inflation.

Darius McDermott, managing director of Chelsea Financial Services, says the infrastructure sector tends to be less volatile that the wider stock market. ‘This is because infrastructure assets generate cash flows that are not dependent on wider economic conditions.

‘Earnings are typically resilient and predictable, so there is some protection from inflation – which has just started to pick up − and the yield can be very attractive, which is another important element at the moment.’

How to get exposure via funds

There are a number of funds that specialise in this area and many have built up globally diversified portfolios. Japan has already announced new major infrastructure initiatives and if the UK, the US and other countries follow suit it could provide a significant fillip to the sector.

Investment Trusts

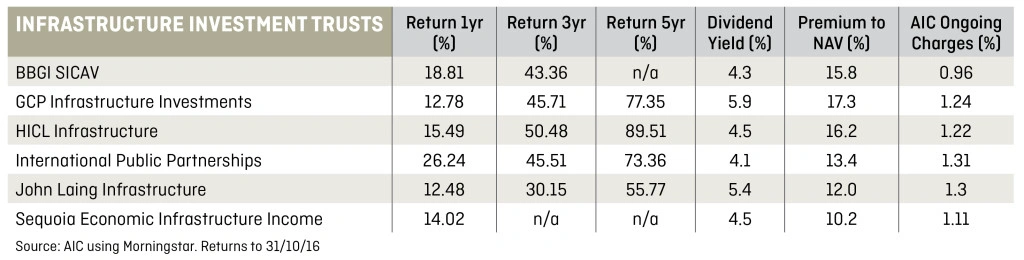

The closed-ended funds tend to invest in the actual infrastructure assets and are mostly trading at a 10% to 20% premium to their net asset value (NAV). This is probably due to the attractiveness of the steady returns and the high, inflation-linked yields that are typically in the range of 4% to 6%.

Alan Brierley, director of the investment companies team at Canaccord Genuity, says the investment bank’s core recommendation for a low risk exposure to the asset class is HICL Infrastructure (HICL).

‘Given superior long-term risk-adjusted returns, an ability to preserve capital and low correlation with other asset classes, HICL has proven strategic asset allocation qualities. In a lower-for-longer [interest rate] environment, these attractions are compounded by strong income characteristics.’

HICL invests in infrastructure projects at the lower end of the risk spectrum with holdings including: Home Office accommodation, the Dutch high speed rail link, the Queen Alexandria hospital and Highland schools. It is yielding 4.5% but trading on a 16.2% premium to NAV.

Open-Ended Funds

Open-ended funds like unit trusts and OEICs always trade in line with the NAV of the underlying portfolio. Rather than invest in the illiquid infrastructure assets, they hold the shares of listed infrastructure companies that can be bought and sold as and when required.

McDermott says that he likes First State Global Listed Infrastructure A Inc (GB00B24HJR07), which invests in infrastructure-related stocks all around the world and is one of the oldest of its type having been launched in 2007.

‘I also like Legg Mason RARE Global Infrastructure Income A Inc (GB00BZ01WP64). It has a target yield of 5% and invests globally. The 13-strong specialist investment team place a heavy emphasis on certainty of future revenues.’

Fund of Funds

VT UK Infrastructure Income C Inc (GB00BYVB3J98) is an open-ended fund that has about two-thirds of its portfolio in infrastructure investment trusts. It launched in January and only has £64m in assets under management, but it offers an attractive prospective yield of 5% with at least three-quarters of the dividend derived from UK Government-backed cash flows.

Stephen West, the fund manager, says that infrastructure assets are generally big and expensive and paying for their construction is usually contracted over long periods of time.

‘Banks and insurance companies have become increasingly reluctant to tie up their capital in these projects and so, over the last 10 years, closed-ended investment companies with access to “permanent” capital have invested heavily in the long-term ownership and financing of these projects.’

Exchange-Traded Funds

There are also several exchange-traded funds (ETFs) that provide exposure to this area. They are cheaper than the actively managed funds, but offer a purely passive exposure that is designed to track one of the global infrastructure indices.

A good example is the US-listed SPDR S&P Global Infrastructure ETF (GII:NYSE:ARCA), which tracks an index that includes 75 of the largest publicly listed infrastructure companies in the world such as Sydney Airport and the Transurban Group, which manages toll roads in Australia and America. It is yielding 3.1% with semi-annual dividends and has a gross expense ratio of 0.4%.

Patrick Connolly, a financial planner at Chase de Vere Independent Financial Advisers, says infrastructure investments can provide steady returns, which makes them well placed to outperform in difficult economic environments, but it’s wrong to assume they are without risk.

‘There can be risks related to the construction and operation of infrastructure assets and the potential of economic, regulatory or political risks, all of which could impact on the returns. Investing via a fund is likely to mean a higher correlation to equity markets, increased volatility and additional layers of cost.’

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.