Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

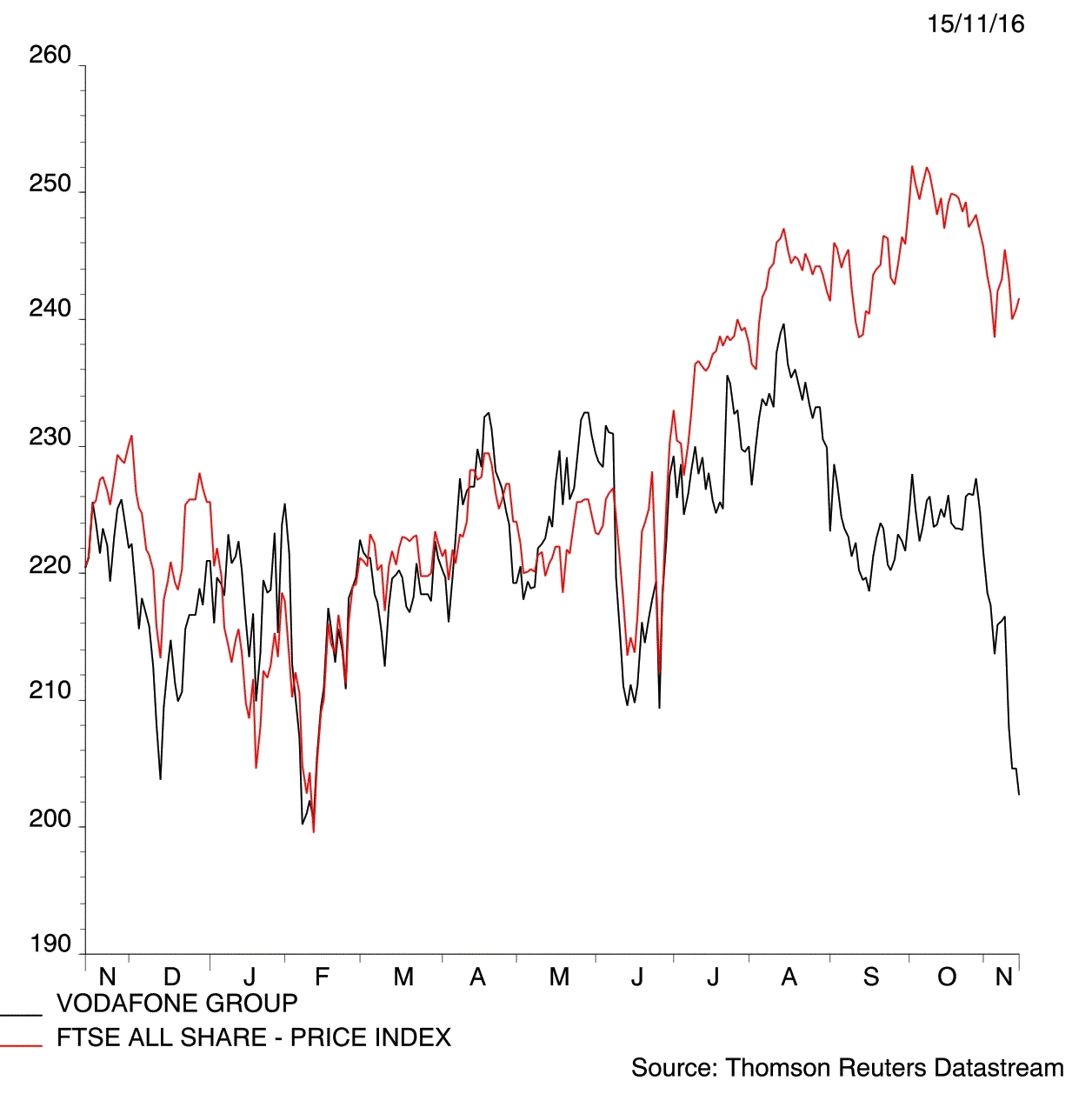

magazineVodafone retains income power

Better than expected half year results from Vodafone (VOD) makes us confident it can continue to pay an attractive dividend, currently yielding 6.2% on a prospective basis.

The telecoms giant raised its half year dividend by 1.9% to 4.74c. That implies 4.1p per share dividend at the current 0.867 euro/sterling conversion rate. It is worth noting that Vodafone now reports in euros.

Analyst consensus for the full year dividend stands at 12.6p, according to data supplied by Reuters.

Gaining strength in Europe

The main message from the half year results (15 Nov) was improving strength across much of Europe offsetting a declining UK, although the rate of reverse is encouragingly slowing.

Vodafone reported first half 2017 revenue and EBITDA (earnings before interest, tax, depreciation and amortisation) down 3.9% and 1.7% at €27.1bn and €7.9bn respectively, but up 1.7% and 4.3% on an organic constant currency basis.

‘The UK let the side down with EBITDA hit by the costs of the well-publicised billing issues, but at least revenue trends got less worse through the half, with second quarter revenues down 2.1% versus 3.2% in the first quarter,’ explains Philip Carse, analyst at IT analysis firm Megabuyte.

Investment bank Jefferies notes that despite a strong first quarter, service revenue growth is no longer expected in the second half of the year.

Competition in India is also biting. Vodafone has taken a €5bn write-down. It is expected to spin off the Indian business next year. (SF)

Vodafone is increasingly becoming a high yield utility. Reaffirmed free cash flow guidance of €4bn this year means the all-important dividend looks well defended. Buy at 204.3p.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.