Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineBurberry’s earnings set for major boost

Luxury retailer Burberry (BRBY) has been a favourite of Shares since the Brexit vote because it boasts stunning profit sensitivity to the sterling exchange rate.

Results at the half-year stage proved this to be the case, with further benefits expected in 2017 if sterling remains around current levels.

Sterling weakness delivered a 9% boost to Burberry’s top line in the six months to 30 September 2016 and a 19% boost to adjusted operating profit.

Since the Brexit vote, shares in Burberry trade 28% higher at £14.18.

Key strengths

There is more to Burberry than a favourable exchange rate environment. It boasts a unique luxury brand, set up in 1856. Medium-term sales growth potential of 4% to 5% is appealing in a low growth economic environment and analysts argue the business can also deliver substantial margin improvements.

Brand strength is an intangible asset which is difficult to value objectively. Burberry’s heritage as a producer of high quality luxury outerwear and accessories is well established in the minds of its target audience and would take rivals many years and potentially hundreds of millions, if not billions of dollars, to replicate.

In an inflationary environment the cost of replicating a brand increases providing another weapon that Burberry has to fight off competitors.

Revenue and margins

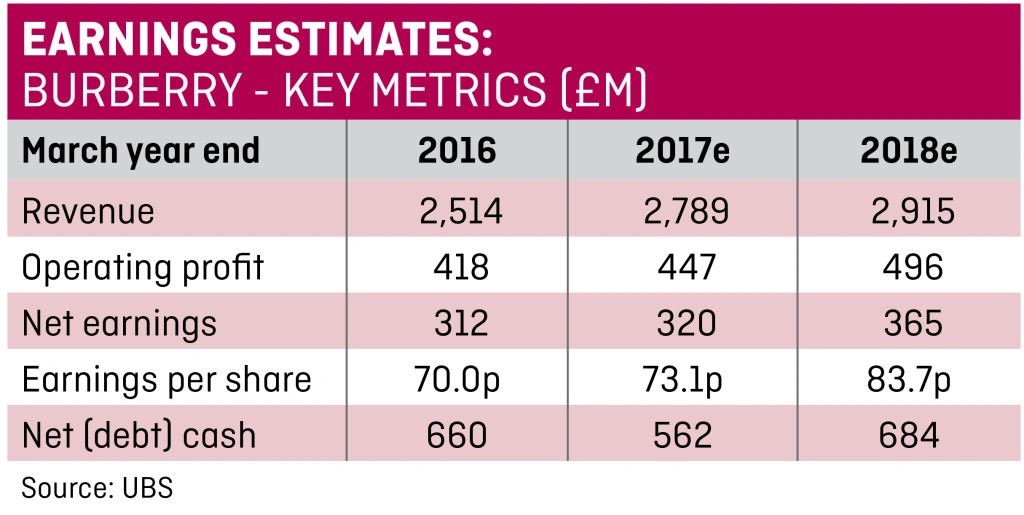

Analyst Helen Brand at investment bank UBS says same-store-sales growth at Burberry could approach 4% to 5% over time, with margins increasing from 15.4% at the last full-year to the region of 20%.

Investors looking at half-year results published 9 November may be struggling to square optimism on Burberry’s potential with its current operating performance. Revenue only gained because of foreign exchange tailwinds and margins declined.

Burberry is in the process of improving its cost base, which is high relative to peers, and this should provide a boost to profitability.

Key risks include deterioration in major luxury goods markets including Hong Kong and China, foreign exchange volatility and failure to deliver on cost savings. A rumoured merger with Coach or other rivals would be a negative development, in our view, as we believe a takeover would transfer too much value from Burberry shareholders to any successful bidder. (JC)

A unique asset on the UK stock market with bags of potential to improve performance.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.