Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineHow can I invest in the earnings power of everyday necessities?

Rising interest rates designed to cool inflation are squeezing consumers’ disposable incomes around the globe with spending on big ticket and discretionary items coming under pressure.

Yet spending on everyday necessities, mass daily-use items that billions employ every day, is holding up rather well. That’s good news for the makers of mundane products which consumers trust and depend upon; think toothpastes, toilet rolls, razors, shampoos, deodorants, bleaches and headache tablets.

There is a theory that consumers are happy to part with their cash, even in the toughest of economic environments, to access recognisable personal care and household brands. In turn, this gives the companies that make and supply them predictable revenues, pricing power and in many cases, high profit margins, which they can sustain through hefty marketing and development spend.

However, the cost-of-living crisis is forcing shoppers to trade down to supermarket own-label products according to many of the UK’s biggest grocers. This means personal care and household goods specialists must tread a fine line between passing on high raw material and other costs to consumers through price hikes and not raising them too high that demand suffers.

Investors taking a long-term view with a stock may be able to look past a slowdown in near-term sales growth. Many experts believe any recession-like environment might only last for a short-term period and therefore consumers may return to the brands they love in time.

WHAT ARE THE IMPORTANT METRICS TO FOCUS ON?

Key metrics to study with personal care and household goods companies include like-for-like sales volumes, an indicator of rising or falling demand for their products, and also gross margin, calculated by dividing gross profit (revenue minus the cost of those sales) by revenue and multiplying the figure by 100 to get a percentage.

High gross margin companies have more of a buffer to handle rising costs as this usually means their wares are in demand and often essential to consumers, which gives them pricing power during inflationary periods.

Other sector metrics worth monitoring include free cash flow, a measure favoured by famous investors including Warren Buffett and Terry Smith, and return on capital employed.

Comparing key metrics

In terms of the major sector players’ metrics, Colgate-Palmolive has the highest five-year average return on capital employed at 32.5%, versus Unilever on 21.8% and Procter & Gamble on 16.2%, according to Stockopedia data.

A good rule of thumb is that a return on capital employed of 15% or more reflects a decent quality business and this is almost certain to mean it generates a return well above its weighted average cost of capital (a metric which is based on the expected return from a company’s shares and the interest cost on its debt).

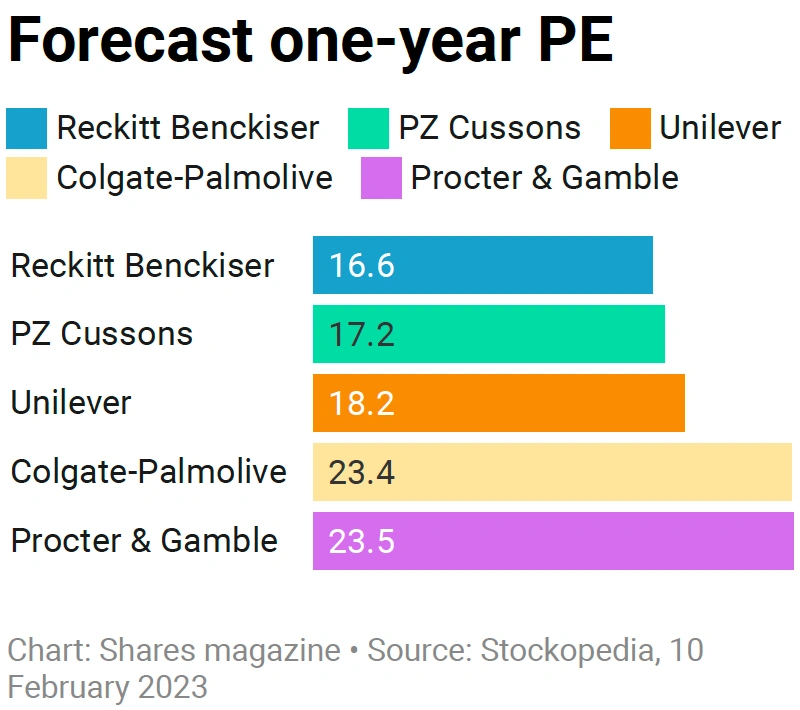

Colgate-Palmolive’s high return on capital employed perhaps explains why it commands the second highest rating in terms of its forecast one-year price to earnings or PE ratio, just behind Procter & Gamble.

Recent company-specific challenges leave Unilever and PZ Cussons trading at significant PE discounts to their US peers on 18.2-times and 17.2-times respectively, while Reckitt appears the cheapest on a forward PE basis, reflecting concerns over downtrading and last year’s shock resignation of well-regarded CEO Laxman Narasimhan, a departure that came at a time when investor confidence in Reckitt’s turnaround was improving.

WHICH COMPANIES CAN I INVEST IN?

The UK stock market is home to Unilever (ULVR), Reckitt (RKT), Haleon (HLN) and PZ Cussons (PZC) which all supply everyday essentials.

Unilever is famed for its food dressings and ice creams, but the FTSE 100 company is also a personal care, home care and beauty/wellbeing products powerhouse whose everyday brands span OMO (or Persil depending on where you live) and Domestos bleach to the Sunsilk hair brand, Sure deodorants and Comfort fabric conditioner.

Reckitt is a cash-generative, dividend-paying consumer goods group which supplies health and hygiene brands ranging from Nurofen, Strepsils and Durex to Dettol, Lysol, Harpic and Vanish.

Haleon (HLN) recently demerged from GSK (GSK) last summer and is behind a range of headache tablets and toothpaste products including Panadol, Sensodyne and Advil.

PZ Cussons owns trusted brands such as Carex hand wash, Morning Fresh washing up liquid, Imperial Leather soap and tanning product St. Tropez. Moving from a turnaround to a transformation phase under CEO Jonathan Myers, PZ Cussons’ latest half-year results broadly met expectations with adjusted pre-tax profit rising 8% to £34.5 million. While the halving of profitability in Europe and Americas wasn’t welcomed by the market, there is a clear path back to longer-term levels of profitability over the next 12 to 18 months.

Within the small cap ranks, there’s private label cleaning products maker McBride (MCB), a struggling distributor of everything from laundry detergents and dishwasher tablets to surface cleaners and aerosols that often finds itself squeezed between giant branded rivals and major retailers.

Theoretically, the £40 million business should benefit from consumers trading down from more expensive products, but indebted McBride has been impacted by high input cost inflation and the shares are down more than 50% over one year.

It’s still early days for its recovery story. McBride reported a return to profitability at the adjusted earnings before interest and tax level in the final two months of 2022.

Heading in the opposite direction with a 44% one-year share price gain is Accrol (ACRL:AIM), the toilet rolls, kitchen rolls and wet wipes supplier benefiting as the cost-of-living squeeze drives growth in its main market, the discount retailers, and private label products.

WHAT ABOUT RELEVANT STOCKS LISTED OVERSEAS?

US-listed options include Procter & Gamble (PG:NYSE), the world’s largest manufacturer and distributor of branded personal care and home care products whose brands include Gillette razors, Pampers nappies and Tide detergent.

While commodity inflation headwinds are easing and Procter & Gamble has seen limited consumer downtrading so far, volumes have deteriorated and investment bank Berenberg expects organic sales growth to slow to 3.3% in the financial year ending June 2024, the lowest since 2018.

Then there is Colgate-Palmolive (CL:NYSE), the household, personal care and pet nutrition products maker and world market leader in oral care, which accounts for nearly half of its sales.

Elsewhere, Kimberly Clark (KMB:NYSE) is relevant to the theme of everyday essential items. The tissue and hygiene products group owns brands such as Kleenex facial tissue, Andrex toilet paper and Huggies disposable nappies.

CAN I PLAY THE THEME THROUGH FUNDS?

There aren’t pureplay funds for this sector, but there are some which include it as part of a broader theme.

For example, tracker fund Xtrackers MSCI World Consumer Staples UCITS ETF (XDWS) has positions in Procter & Gamble and Unilever, representing 9.2% and 3.26% of the fund respectively, and charges 0.25% a year.

In the investment trust universe Nick Train’s Finsbury Growth & Income (FGT) has 9.4% of its assets in Unilever. Troy Income & Growth (TIGT) had 32% of its assets in consumer staples as of 31 December 2022, with Unilever the largest position at 7.9% of assets and Reckitt representing 5.7% of the portfolio.

Colgate-Palmolive remains one of the largest equity positions in Dan Loeb’s Third Point, the hedge fund UK investors can access through Third Point Investors (TPOU).

Third Point argues Colgate-Palmolive offers ‘defensive growth at a reasonable valuation’, while activist investor Loeb ‘continues to see the potential for shares to deliver an attractive risk-adjusted return over the coming years’ and believes Colgate is ‘on the road to delivering more predictable returns moving forward’.

Third Point notes organic growth remains strong and expects that to translate into earnings growth as execution improves, margins recover and external pressures ease.

TWO STOCKS TO BUY

Procter & Gamble

(PG:NYSE) $138.57

While second quarter results (19 January 2023) showed organic sales growth slowed to 5% from 7% in the previous quarter, Procter & Gamble still raised its sales growth outlook for fiscal 2023 and maintained its earnings per share growth guidance range despite citing ‘significant headwinds’.

The large cap consumer defensive has posted some of the best growth in the sector in the past few years and increased its dividend for 66 years in a row.

Behind everyday products ranging from Pampers and Pantene to Lenor, Oral-B, Vicks and Tide, the Cincinnati-headquartered sells products in 180 countries and it has the hallmarks of a high-quality company. It boasts robust operating margins, rising free cash flow per share and a return on capital employed north of 20-times, on a trailing 12-month average basis.

Trading on 23.5 times forecast earnings, investors are being asked to pay a premium rating to own the shares. However, its track record warrants this premium.

Analyst coverage collated by Stockopedia reveals that 14 brokers have a ‘buy’ rating on the stock, while 12 have a ‘hold’ and only one has a ‘sell’ recommendation.

Unilever

(ULVR) £41.09

Undemanding relative to history, Unilever’s prospective price to earnings ratio of 18.2 looks compelling for a business boasting wonderful brands, a strong emerging markets footprint and scope for big strategic, operational and financial improvements.

Its latest full-year results saw like-for-like sales grow by 9% as selling prices rose by 11.3% in response to input cost inflation, but volumes were down 2.1%, suggesting that Unilever needs to be careful not to raise prices too much higher without alienating its customer base.

Underlying sales growth at the firm’s ‘billion+ Euro brands’ such as OMO, Rexona and Sunsilk rose by an encouraging 10.9%. For the current year, Unilever is predicting further stiff price rises in the first half to offset higher input costs, and another fall in volumes as a result, but believes a more measured second half increase in prices should lead to underlying sales growth ‘in the upper half’ of its 3% to 5% medium-term target.

Hein Schumacher will join as the new chief executive in July and will be busy on day one, given Unilever’s falling margins, declining sales volumes and confused approach to strategy. Readers may wonder why the shares are worth buying given these negatives, but the key attraction is the ability to pick up the shares at a discount to many peers and to own as a ‘repair and improve’ story, led by the new CEO.

Schumacher has the support of activist shareholder Nelson Peltz who has been trying to drive change in recent months. The new CEO is likely to take a long hard look at Unilever’s portfolio of over 400 brands, with disposals sure to follow.

Fundsmith founder Terry Smith believes the company should improve what it already has, and only then think about acquisitions and disposals.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Feature

- How ChatGPT could change the world: Why it matters and ways to invest in artificial intelligence

- Discover the stocks that delivered positive returns – even in the bad years

- Why buying Ocado shares could be a more volatile ride than you think

- Why is Vanguard LifeStrategy so popular and is it a top performer?

Great Ideas

News

- Coca-Cola serves up revenue beat while faster growth is stirring at Keurig Dr Pepper

- AstraZeneca boasts record share price high with big plans to deliver new drugs

- Lyft in name only as quarterly loss stuns investors

- How an averted gas crisis could help Europe avoid a recession

- Risk-hungry investors drive Metro Bank shares to 12-month highs