Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineSearching for small cap value

There have been some very successful small cap stocks in recent years, rewarding shareholders with returns equal to three or more times their original investment. The ability to make significant gains is a key factor behind investors risking their money in smaller companies.

We believe there could soon be a shift in investor appetite as a result of sky-high valuations. Many small cap fund managers are already taking profit on successful stocks including Fevertree (FEVR:AIM), Gear4Music (GFM:AIM) and Blue Prism (PRSM:AIM) as they see better value elsewhere in the market. Should you do the same?

In this article we explain why some fund managers are reducing exposure to these types of stocks and where they are reinvesting their profit. We talk to other managers about why they aren’t tempted by super-high growth stories and we reveal the secrets of their stock picking success.

Finally, we profile five stocks tipped by some of the leading small cap fund managers as among their brightest hopes for making money in the future.

Why are fund managers taking profit on successful stocks?

The problem lies with valuation rather than anything wrong with the actual companies. Many fund managers are sitting on significant paper profits and they feel it is prudent to crystallise some of those gains while the equity valuations are high.

Other fund managers have point blank ignored the rapid growth small caps – which includes the likes of BooHoo.com (BOO:AIM) and Purplebricks (PURP:AIM) – saying their valuations were too expensive even before share prices surged.

‘I can’t get my head round it,’ says Downing small cap fund manager Judith MacKenzie. ‘They are good companies but the valuation doesn’t make sense. Small cap ratings in general are too high. They are the most expensive I’ve seen in fifteen-plus years.’

Richard Powers, head of quoted smaller companies at asset manager Octopus, goes as far as calling some small cap valuations ‘scary’.

To give you an idea of current valuations, Gear4Music and BooHoo are both trading on 76 times forecast earnings for the current financial year; and Fevertree is on 62 times forward earnings.

In general, most investors prefer to buy decent companies on sub-20 times earnings. Some people, however, would be prepared to buy stocks on a higher rating if they demonstrate rapid growth – such as has been the case over the past few years with some of the companies mentioned in this article.

Purplebricks isn’t forecast to be profitable until 2019 so you cannot calculate a PE ratio on the current year’s metrics. However, you can work out that it trades on 12.8 times forecast sales for the year to April 2018.

As a comparison, traditional estate agent Foxtons (FOXT) trades on 2.1 times forecast sales for its current financial year which is more than six times cheaper than Purplebricks.

Powers at Octopus says he has recently taken some profit in Gear4Music and Blue Prism, although he insists both companies remain attractive. Old Mutual has selling down stakes in Gear4Music and Fevertree; Kames has also taken profit on the latter stock. BlackRock has been selling Keywords Studios (KWS:AIM).

It is important to stress that elevated valuations do not apply to the entire small cap sector; far from it. Fund managers are still finding plenty of opportunities, as we will discuss in this article.

Richard Bullas, who co-manages Franklin UK Smaller Companies Fund (GB00B45G7D25), says the FTSE Small Cap index trades on 12.7 times forward earnings, compared to the FTSE All-Share on 14.3 times. He believes the former rating is more in line with the longer term average.

‘Small caps were trading at a 25% discount to the market last summer. That discount has narrowed to about 10%. I wouldn’t say small caps are overvalued, neither would I say they are cheap. It is all about being selective when picking stocks in this area.’

We spoke to numerous small cap fund managers for this article and many said they were now looking at companies valued at less than £400m, some even preferring the sub-£100m bracket. Interestingly, the majority of people we interviewed expressed a preference for companies that generate cash and make a profit.

Many investors have become excited about companies trying to disrupt markets with new technologies or innovative business models, such as robotics firm Blue Prism whose share price has increased 11-fold in 16 months.

Bullas says he isn’t tempted by such firms as many are loss making and are likely to continue to require additional funding. ‘I prefer companies that have reached a tipping point with profitability. Some of the high growth stocks can give you amazing returns but they are very difficult to value.’

The fund manager says he doesn’t want to pay something like 80-times earnings as that would be pricing in considerable success, which isn’t guaranteed. ‘I’d rather wait for demonstration of profit, even if it means giving up some of the share price upside.’

Downing’s MacKenzie says she always looks at the potential downside to an investment case, hence why she prefers backing companies with positive free cash flow and profit, as something to fall back on.

You might think these more conservative approaches will result in only backing slow growth businesses, but that isn’t necessarily the case. Many of the small cap fund managers we interviewed say they are still able to find firms with the potential to be much bigger in the future at a decent price.

For example, David Stevenson, who co-runs TB Amati UK Smaller Companies Fund (GB00B2NG4R39), says he has a strict selection process which favours companies which can convert a high proportion of their profit into cash, and which are appropriately financed for the ‘nature, maturity and future growth of their business’.

Such criteria might not favour the super-fast growth companies which constantly need more cash, yet this process did previously identify some of the current star performers on the market, hence why he has stakes in Fevertree and Gear4Music.

The Amati fund’s latest monthly investment report says some profit has been taken in various ‘high flying stocks’. Stevenson confirms this group includes Fevertree, Keyword Studios, DotDigital (DOTD:AIM), GB Group (GBG:AIM) and among the large caps, Just Eat (JE.).

‘We’ve taken some profit on these stocks but still retain material holdings in each as we still feel valuations are justified given the growth outlook for these companies,’ he comments.

‘This was a pre-emptive measure, as there has been a noticeable shift in UK market dynamics recently, with growth stocks losing leadership as investors lock in some gains.

‘We feel this is linked to the step-up in bond yields, as capital markets anticipate an approaching inflection point in central bank stimulus, and leadership passes to financials which are likely to benefit from increasing market rates.’

You have to consider that many fund managers may have originally bought the star performers at much cheaper valuations than at present, so owning them now doesn’t necessarily mean they overpaid for the stocks.

The key challenge is when to sell – is the current rate of growth sustainable or could it accelerate? Is there a risk that the pace of growth could slow? The answer would have a bearing on justifying the current valuation and whether to hold or sell.

Stevenson explains his approach: ‘Our investment research effort targets high quality, robust businesses which have the potential to grow over the longer term at rates faster than the stock market average.

‘One current example would be Quixant (QXT:AIM), the designer/manufacturer of hardware and software solutions for the global gaming and slot machine industry. This is a highly regulated activity, and Quixant is a key service provider to a diverse range of mid-tier customers, but the largest targets are yet to outsource.’

At 410p, Quixant presently trades on 24 times forecast earnings for 2018. That’s a fairly punchy rating, although nowhere near as high as the likes of Fevertree and BooHoo.

Richard Power at Octopus is another fund manager excited by the stock. He says Quixant has the potential to be a much bigger company. ‘Getting a few more tier 1 customers will be transformational for the business. There are also regulatory developments in Brazil and Japan that will open up new markets for them,’ he says.

There is a similar valuation debate for radiology specialist Medica (MGP:AIM), a stock flagged to us by Jeff Harris, fund manager at Strategic Equity Capital (SEC), who says it ticks a lot of the right boxes for what he desires in a small cap business.

At 230p, it trades on 26.7 times forecast earnings for 2018. Investec has a 253p price target (based on a discounted cash flow model), which doesn’t imply much upside from the current level. Therefore investors buying today have to put a lot of faith in the business to deliver decent growth for years to come.

Harris bought at the float price of 135p in March 2017 and has already enjoyed 70% valuation uplift on his investment. Nonetheless, his enthusiasm implies this is a stock that has much further to run.

‘It is the UK market leader and enables hospital radiology departments to send CT scans and X-rays to a Medica (NHS qualified) radiologist to remotely interpret the scan,’ says the fund manager.

‘It has grown strongly due to the growth in scanning activity driven by demographics and healthcare guidelines alongside the shortage of radiologists in A&E departments.

‘We performed significant primary diligence, speaking to healthcare professionals in the UK and the US where the market is more mature and believe the prospects are good.

He adds: ‘It is higher growth than (one of our) typical investments but we believe the business is very high quality with many long term structural growth drivers and has the possibility to move into other therapeutic areas.’

Jonathan Brown, who manages the Invesco Perpetual Smaller Companies (GB0033030528) fund, says he looks for growing businesses which can be twice as large over a five year period. ‘We like companies that have good profit margins and returns on capital which indicate they have something special about their business.’

The Invesco portfolio currently includes IT consultant FDM (FDM) and textile rental provider Johnson Service (JSG:AIM).

Harris at Strategic Equity Capital says he doesn’t seek ‘supernormal’ growth when trying to spot new small cap investments. Instead, he prefers ‘longer term sustainable growth driven by high IP (intellectual property) and durable business models’.

The fund’s current holdings include industrial automation software provider Servelec (SERV:AIM), education technology firm Tribal (TRB:AIM) and financial adviser IFG (IFP).

Harris says he focuses on the ‘four drivers of equity returns’. First is growth in operating cash flow. Second is re-rating potential.

‘The public market derivative of earnings per share is the PE (price to earnings) ratio. We consider this, but do detailed cash flow analysis and use a cash flow based valuation metric,’ he explains. ‘This is operating cash flow less maintenance capex over enterprise value, which takes into account the capital structure.’

The third driver is corporate activity, both as a buyer and as a target. ‘There is empirical evidence that transaction values are a better gauge of fair value over the long term. We assess precedent transactions and use our network to understand “real world multiples”.

‘We look to avoid companies with impediment to take-out such as a large pension scheme or blocking shareholder.’

The fourth driver is de-gearing and a detailed analysis of cash flow to assess the potential transfer of value from debt to equity holders.

Harris believes public markets don’t place enough value or emphasis on cash flow, focusing a lot on dividends, which are often paid out of debt.

‘We look at dividends but also the ability to pay down debt from free cash flow. We believe that by focusing on all four drivers rather than growth or value in isolation, it gives the best chance of achieving our desired returns.’

Takeover potential is something that’s also integral to Livingbridge’s investment process. You may have heard the advice ‘never buy a stock purely as a bid candidate’; however, an important part of small cap investing is being able to identify a future exit.

Small cap stocks can be very illiquid, so fund managers need to be confident they won’t be stuck holding a large chunk of a business that they can’t sell in the future. One exit route is a takeover.

‘Our style is seeking growth at a reasonable price. Livingbridge has a private equity arm, so we are well plugged into the corporate finance community,’ says Ken Wotton who manages CF Livingbridge UK Micro Cap Fund (GB00B55S9X98), formerly called Wood Street Microcap Investment Fund.

‘That side of the business buys and sells companies regularly, so we’ve learnt the importance when considering an investment, of finding out who the potential corporate buyers might be and what they are looking for in acquisitions.’

Livingbridge is clearly very good at spotting future takeover candidates. Wotton says 23% of the holdings in the micro-cap fund since inception have been taken over, either when it held an investment or later on after it had sold out.

Examples include Kalibrate Technologies (KLBT:AIM) which is in a bid situation now; and System C Healthcare which was on AIM until being bought by US pharmaceutical distribution giant McKesson.

‘We originally invested in System C as one of our colleagues in the private equity side of Livingbridge had done research into the sub-sector which identified the business as a strategic asset in that industry,’ he reveals.

The fund’s largest holdings, as of 30 June, include deep fat fryer cleaner Filta (FLTA:AIM) which floated on AIM in November 2016; corporate foreign exchange specialist Alpha FX (AFX:AIM) which joined AIM in April 2017; and energy procurement services group Inspired Energy (INSE:AIM).

The downside of takeovers is that a fund manager needs to redeploy the cash proceeds and rebuild their portfolio by adding something new or increasing a stake in an existing holding.

Investing in small caps often requires patience, so a fund doing well one year thanks to a number of takeovers may not necessarily do as well the following year as a result of new holdings taking time to come to fruition.

‘While we typically like to run our winners, we may sell a stock if a company reaches an unjustifiably and unsustainably high valuation,’ says Charles Montanaro, fund manager of Montanaro UK Smaller Companies Fund (MTU). ‘It is also worth pointing out that companies do leave the portfolio due to takeovers.

‘In 2006 we lost no less than twenty of our holdings for this reason. While this is often exciting – particularly if the premium is high – it can be frustrating to lose a company that we had hoped to hold for decades.

‘We would far rather enjoy steady, conservative returns over the long-term through holding a company and management team we know well and trust.’

FIVE STOCKS MAKING FUND MANAGERS EXCITED

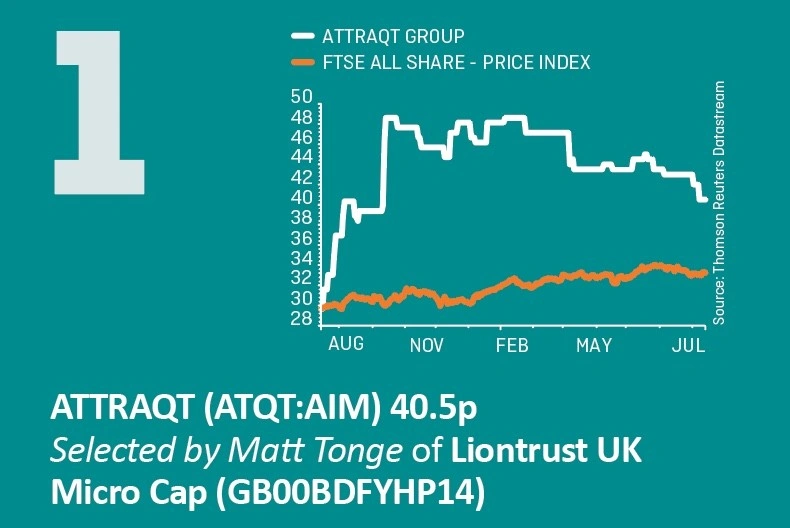

Attraqt sells website search, visual merchandising and personalised product recommendation software to online retailers.

‘For example, if ASOS (ASC:AIM) sends an email to a customer with an offer and that customer clicks on a link, the Attraqt software will personalise what appears on the landing page, offering those products the customer is most likely to buy,’ says Tonge.

‘The company has intellectual property in the software code. It enjoys embedded distribution network strength as customers come to rely increasingly on the product to drive improved conversion of “clicks” to sales. It also sells its products on a monthly recurring software-as-a-service subscription basis, meaning around 90% of revenues are recurring.

‘Attraqt has a fantastic referenceable customer base in a structurally growing market. Furthermore the valuation versus similar listed companies leaves room for upside.’

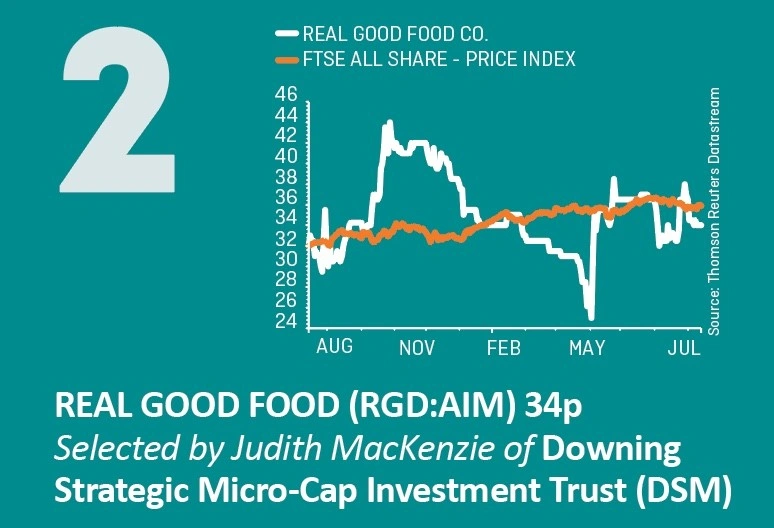

Funds managed by Downing struck a deal in June to invest £11.5m in loan notes and equity in Real Good Food, best known for cake decoration. Fund manager MacKenzie is also taking a seat on the board of directors.

Unlike many small caps which tap the market for funding just to keep going, Real Good Food has raised new money because of growing demand for its products and services.

‘The expansion capital is coming off the back of contracts and demand. Confidence in the top line is strong; it’s now all about execution,’ says the fund manager.

The company has a double digit margin sugar paste operation and runs in-store bakeries for the likes of Waitrose and Marks & Spencer (MKS), says MacKenzie.

She believes Downing’s equity investment (it has taken a 10% stake in the business) could increase by at least three or four times in value over time.

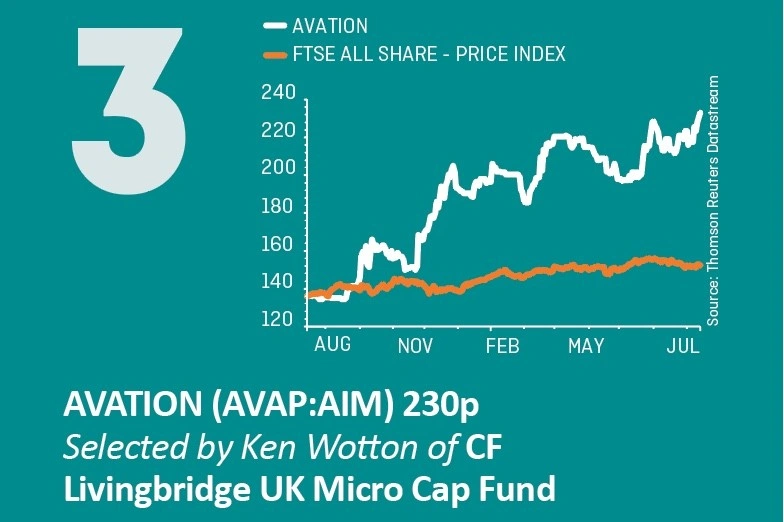

The commercial passenger aircraft leasing company has some well-known customers include Virgin Australia, Air France and Thomas Cook (TCG).

Ken Wotton at Livingbridge says Avation ‘is in a nice position with really good visibility of earnings’. He adds: ‘It buys aircraft and leases them on long-term contracts. It focuses on a few types of planes used by mid-range airlines. It also has options to purchase planes quite far into the future.

‘These are very popular planes and it is quite competitive to get them new. Avation could trade its options if it so wished.’

The fund manager says Avation has exciting potential with good earnings and a route to expand its fleet. ‘It trades on a cheap multiple and pays dividends.’

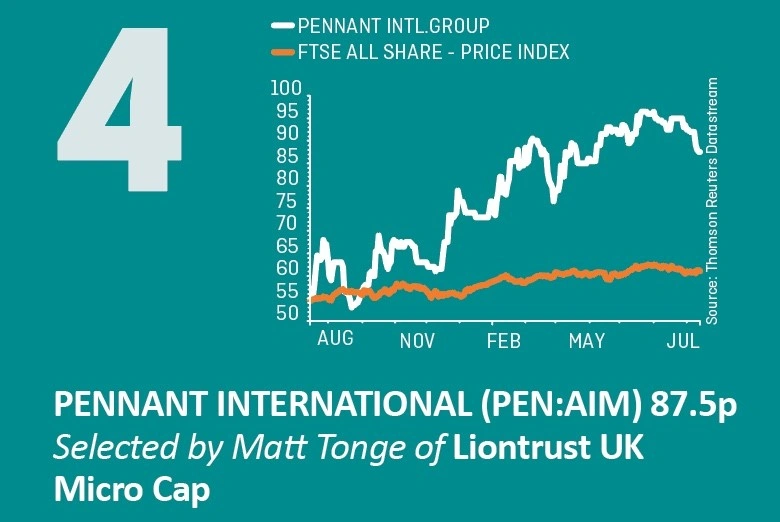

The Liontrust fund manager likes Pennant, a Gloucestershire-headquartered firm which provides equipment to the defence industry.

‘Its main products are highly realistic simulators of pieces of capital equipment (such as tanks) which military colleges and departments of defence use in training programs,’ says Tonge.

‘Pennant possesses skills in hardware and software engineering. It has requisite security clearance to be allowed to see the blueprints of the systems it emulates; and once installed these systems can generate service revenues for many years.

‘For example, it’s been providing training on the AgustaWestland helicopter for over thirty years. It’s rich in intellectual property, has very strong customer relationships and operates in an industry with high barriers to entry.’

FFI is the world leader in providing completion contracts to financiers of the global film and TV industry, according to Stevenson. It recently joined the stock market (30 June 2017) at 150p and has subsequently risen in price to 157.5p.

‘Its contracts give insurance against cost and time budget overruns,’ says Stevenson. ‘FFI has a history going back to the 1950s and a dominant market share.

‘Although the bulk of the risk is sold down to conventional insurance companies, FFI’s specialist knowledge still generates significant margins.’

By Daniel Coatsworth and David Stevenson*

*No relation to the Amati fund manager with the same name mentioned in this article

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- Brexit puts squeeze on consumers and businesses

- Pressure on Blancco Technology

- Keep toasting cash-generative Conviviality

- Yu Group to beat forecasts

- Weir seeing North American shale recovery

- Carillion bailed out by HS2

- What will McCall do at ITV?

- Sage to sidestep HMRC’s digital delay

- EasyJet reveals post-Brexit plans as CEO departs