Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineLoopUp bats off Amazon threat

Remote meetings specialist LoopUp (LOOP:AIM) has brushed aside emerging competition from Amazon Chime, the new video and audio conferencing platform being launched by the US technology giant.

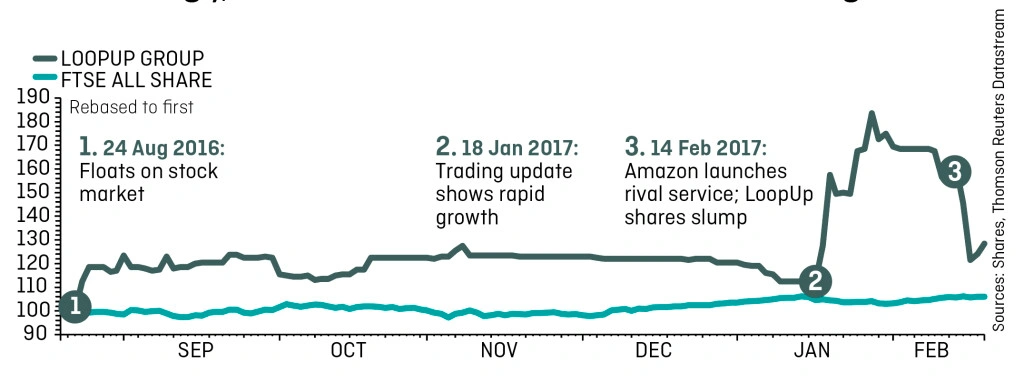

LoopUp’s share price fell by 25% in the three days following Amazon’s announcement that it was entering the market (14 Feb). Unusually for a listed company, LoopUp didn’t issue a statement to the stock market commenting on the share price slump.

We’ve spoken exclusively to the company to get its thoughts on the matter.

Is the company worried or relaxed?

LoopUp’s chief executive Steve Flavell sees Amazon’s development as no more than business as usual.

He insists that experience quality remains the key to addressing the vast enterprise market that LoopUp is targeting. We translate that comment as LoopUp believing its system is better quality than others.

Amazon is renowned for pouring huge investment into niche growth markets it feels it can eventually dominate. This reputation has clearly put the fear into LoopUp shareholders, worried that the US technology company’s deep pockets may spell the end for the UK small cap firm.

Flavell remains resolute and relaxed. He says there is ‘nothing new about big companies coming in’ to the remote conferencing sector. He adds: ‘we’ve been competing for many years against rivals with enormous funding resources.’

Rivals include Microsoft’s Skype for Business, Google Hangouts, Cisco’s WebEx, Adobe and AT&T. More recent start-ups include GoToMeeting, JoinMe and the UK’s Powwownow.

There has always been competition

Large competitors have been around for as long as ‘we’ve been in for the market, and we have still grown strongly,’ says Flavell, adding that LoopUp has consistently grown during the past three years.

His confidence springs from the fundamental problems that have hamstrung remote conferencing for decades: platform reliability and experience quality.

Most existing platforms either require users to dial-in or piggyback voice over internet protocol (VoIP).

In the latter case it typically means poor sound quality and a propensity for the call to drop out. In the former instance, you often require endless introductions because you can’t tell who is on the conference or not. In either case the experience becomes time consuming and frustratingly tiresome.

Why is LoopUp's platform different?

LoopUp’s platform is a genuinely 21st Century digital streamlined option for hosts and participants that not only works well, but is intuitive and easy to use.

This last point is crucial to Flavell because it makes the platform accessible for even relatively technophobic users. The CEO even admits resisting some bells and whistles extras requested by some clients because it may add an unwelcome layer of complexity that will not suit everyone.

Interestingly, the Amazon Chime announcement did not come out of the blue. Flavell had wind that a new product launch was on the cards ever since Amazon’s reported $2.9bn acquisition of California-based conferencing and messaging start-up Biba Systems in 2016, a company he had long followed.

Flavell says he feels very strongly that LoopUp is protected from competitors. It has several registered patents including the call start alert that is sent to all participants as soon as the first person joins the conference.

Does LoopUp make any money?

LoopUp joined the AIM stock market on 24 August 2016, raising gross proceeds of £8.5m at 100p per share. That gave the company a market capitalisation of £40.8m at the time. The story has clearly excited investors with stock demand sending the share price soaring to a record 182p at the end of January 2017. You can now buy the shares at the much cheaper price of 127.7p, thanks to the Amazon panic.

The business remains at an early stage in its growth phase but it is already profitable. The company has delivered compound average growth of 36% a year since 2013 and it has been EBITDA (earnings before interest, tax, depreciation and amortisation) profitable since the last quarter of 2013.

Full year results to 31 December 2016 are due on 8 March 2017. They will show a modest acceleration on that compound growth figure. The company is due to report £2.1m EBITDA on £12.8m revenue. Gross profit margins run in excess of 80%.

This is a huge potential market, worth around £5bn according to Flavell’s information. The prize for success is enormous, especially for a business of LoopUp’s relatively small scale.

The estimated enterprise value of roughly £48m looks like a rich valuation even after the recent stock plunge. Investors thinking about adding this stock to their ISA or SIPP (self-invested personal pension) may wish to wait for the results to be published before making the decision whether to buy or not.

It is one of those tricky situations where small companies can regularly trade on expensive ratings if they have rapid growth – such as is the case with LoopUp. We will keep a close eye on the results and will firm up our view on the investment case soon. (SF)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

Editor's View

Great Ideas Update

Larger Companies

Main Feature

Money Matters

Smaller Companies

Story In Numbers

- UK Banking Shares Performance

- General Retailers Shares Performance

- Story In Numbers - Fishing Republic

- 37%

- Five profit warnings in 15 months

- 1st time in 12 months: Investors give bullish signal with fund inflows

- From $17m to zero: Kenmare Resources’ earnings up in smoke

- $205.2bn: The value of failed takeover deals so far in 2017