Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

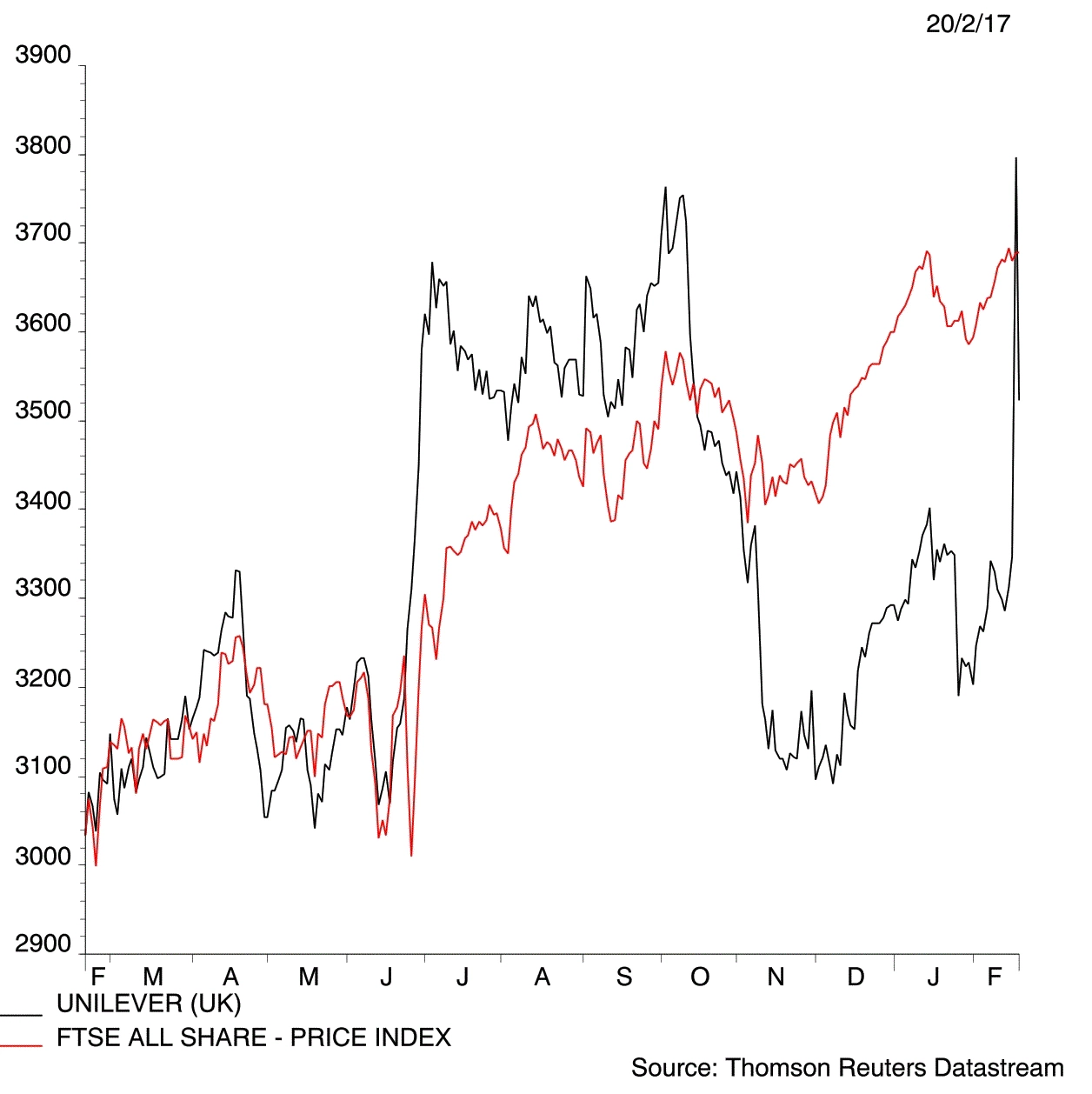

magazineIs Unilever worth buying after failed takeover bid?

Many investors are asking whether they should buy Unilever (ULVR) now that Kraft Heinz has given up on its $143bn mega-merger plan. The answer is ‘yes’, in our opinion.

We’re big fans of the company as it has reasonably predictable earnings, fantastic brands and global reach.

We view the situation a bit like former FTSE 100 British technology champion ARM Holdings, acquired by a Japanese suitor last year. We really miss the stock now it has gone, as there is nothing else similar on the market. The same would have applied to Unilever if Kraft had been successful.

‘Unilever has an unrivalled emerging market presence and generates more than half of its sales from those parts of the world expected to experience strong growth in demand for consumer goods,’ comments investment management group Patronus Partners.

‘Unilever generates strong cash flow and has consistently grown its dividend in real terms, making it a very attractive investment proposition.’

Cultural incompatibility, limited capacity for Kraft to raise the cash portion of the bid and anticipated resistance from Unilever shareholders are among the reasons why Kraft is thought to have walked away instead of ‘going hostile’.

What will Unilever do next?

Analysts have speculated that Unilever might respond to this episode by releasing some value to shareholders. Rattled management might respond with a major share buyback or a special dividend.

Could Unilever turn the tables and undertake a large ticket takeover itself of a rival (not Kraft)? It seems clear than investors are willing to back big deals, as evident by recent tie-ups in the form of British American Tobacco/Reynolds and Reckitt/Mead Johnson.

Although Kraft’s bid for Unilever highlights the pressure on brand owners to consolidate in the face of margin pressure and constrained organic growth, we remain big believers in large defensive businesses as superior, long-term investments.

Unilever’s entrenched global distribution networks and brands including PG Tips, Magnum, Marmite and Dove represent a wide economic moat. That’s a company’s ability to maintain competitive advantages over its rivals to protect long-term profits and market share from competing firms.

According to Morningstar, Unilever has a wide economic moat derived from two key sources. The first is its entrenchment in the supply chain of retailers. A broad portfolio of products across multiple categories and supermarket aisles creates a virtuous cycle of competitive advantages, including intangible assets that new market entrants couldn’t replicate.

Morningstar also says Unilever has one of the strongest cost advantages among its industry peers, being a fairly efficient manufacturer with one of the lowest costs per employee.

We continue to like Unilever as a fantastic long-term investment. Buy at £35.67. (JC)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

Editor's View

Great Ideas Update

Larger Companies

Main Feature

Money Matters

Smaller Companies

Story In Numbers

- UK Banking Shares Performance

- General Retailers Shares Performance

- Story In Numbers - Fishing Republic

- 37%

- Five profit warnings in 15 months

- 1st time in 12 months: Investors give bullish signal with fund inflows

- From $17m to zero: Kenmare Resources’ earnings up in smoke

- $205.2bn: The value of failed takeover deals so far in 2017