Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineSage confident ahead of new test

FTSE 100 software supplier Sage (SGE) remains convinced it can accelerate its pace of growth in the face of stiff competition.

The past 12 months were largely about transitioning many of the company’s thousands of small and medium-sized enterprise clients into the cloud. The next 12 months will see Sage invest in sales and marketing to boost customer numbers.

Sage has become one of the UK’s leading software and enterprise tools suppliers. Although best known for accounting services like payroll and tax processing, it also offers extra services for areas such as human resources and customer relationship management.

Chief executive Stephen Kelly has been trying to move clients to a software-as-a-service (SaaS) model without cannibalising its large installed licence buying base.

Slow and steady

Full year results to 30 September 2016 demonstrate the skill with which this task has been handled. Organic revenue growth marginally beat the 6% target (6.1% reported) to £1.57bn.

It also achieved a modest uptick in operating profit margins from 26.5% to 27.2%.

Sage reported a 10.4% increase in recurring revenues, its best in a decade, to £1.09bn largely driven by 32% growth in subscription income.

This was managed in the face of an expected but well-managed decline in perpetual licence revenues, down around 15%. This latter revenue stream now accounts for less than 9% of overall group sales.

Improving quality

‘Two things jump out from Sage’s results,’ says Angela Eager, analyst at the TechMarketView website. ‘The control and visibility it has regarding its business model transition, and that in terms of revenue, the quality is improving,’ she explains.

Kelly is steering the market towards another year of 6% organic revenue growth and for operating profit margins of ‘at least 27%’.

Numis analyst David Toms has trimmed back operating margin forecasts for this year and next to 27.5% and 28% respectively. The previous figures were 28% and 29%. ‘We see little to make us expect earnings outperformance on a 12-month view,’ comments Toms.

There is also intensifying competition in this space. Intuit’s Quickbooks has been spending heavily in a bid to take market share, while newer entrants such as Kashflow and New Zealand-based Xero are also active on the marketing front. (SF)

![]()

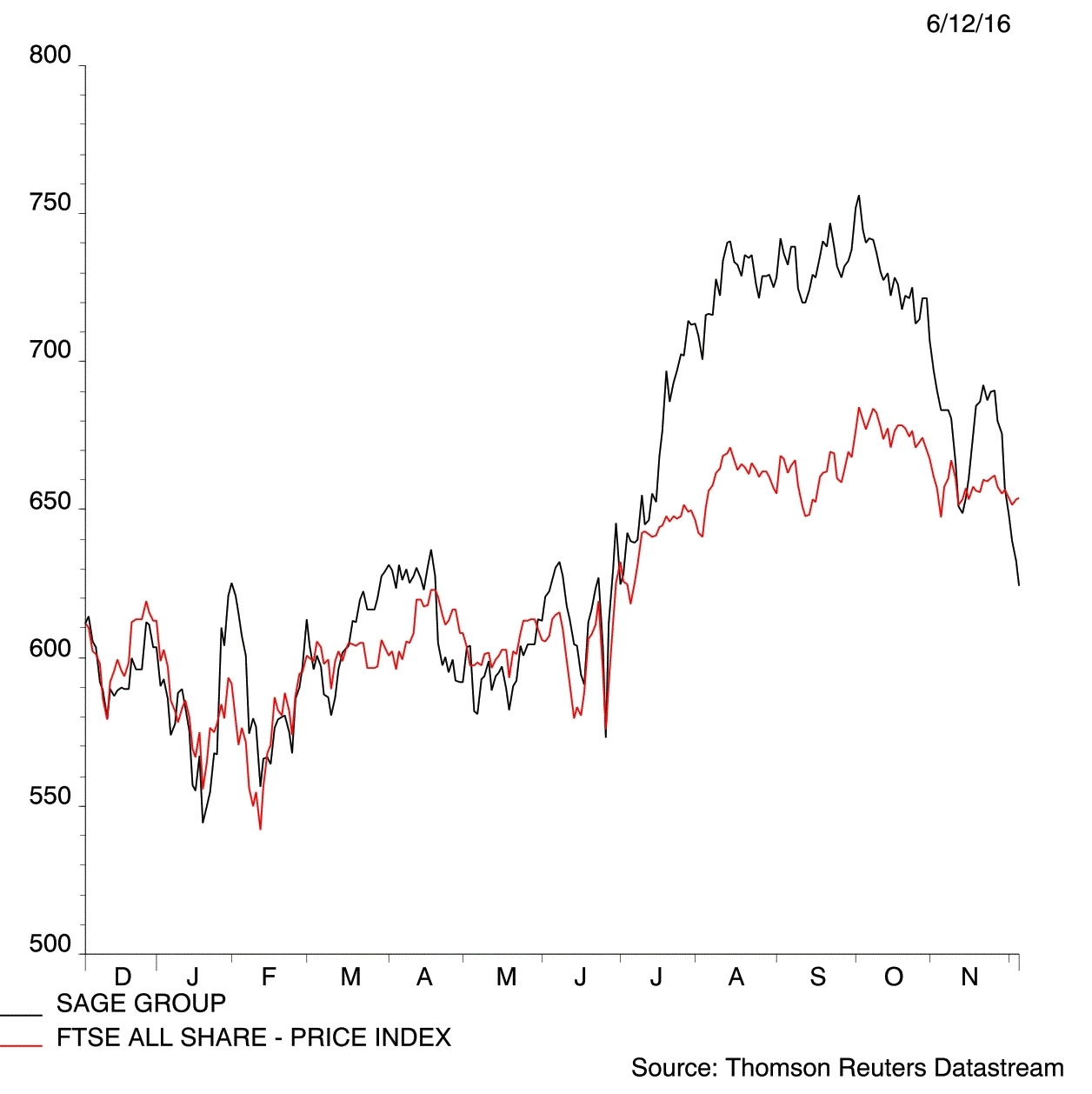

These latest figures were very solid but, as we cautioned in Shares on 3 November, there is not yet firm evidence of accelerating growth at Sage. The shares at 639p are trading on just below 20 times forecast earnings. That’s high enough for current events. We want to see Sage step up a gear before getting excited about the shares.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.