Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineHot questions for 2017

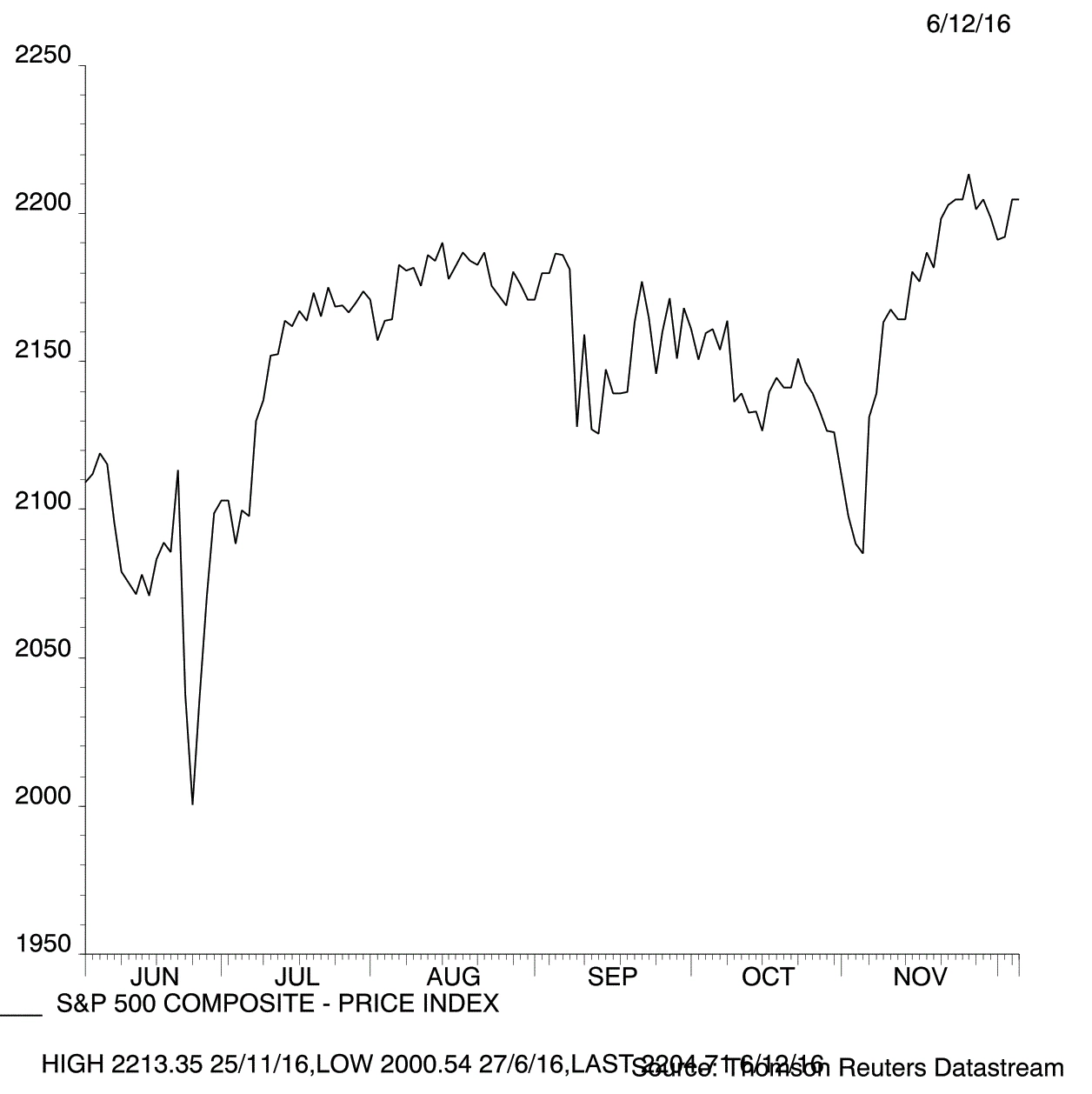

On balance we believe global stock markets will have a good year in 2017 despite plenty of big political events which could cause bouts of volatility.

Economic data is positive in the US, Eurozone and China in particular and corporate earnings are forecast to improve over the coming year. Investment bank Morgan Stanley believes the latter point should drive outperformance from value stocks and large caps.

The biggest unknown for UK investors is how the triggering of Article 50 (officially starting the Brexit process) will impact the London stock market. We have a feeling it could set off another bout of weakness in UK domestic companies and benefit the overseas earners on the FTSE 100.

To help you stay abreast of events, we now discuss the big issues facing the market in 2017 including Trump’s first 100 days in power, where next for commodity prices and whether the European elections really matter to UK investors.

What happens when the Brexit process begins?

Prime Minister Theresa May is expected to invoke Article 50 sometime in 2017 and trigger the UK’s two-year countdown to a European Union exit.

A pledge to declare the UK’s intention to leave the trading bloc by 31 March 2017 looks ambitious given legal challenges against parliament’s authority to use centuries-old executive powers originally granted to the monarchy to deliver on the promise.

Parliament may be needed to approve the move. Members of the House of Lords have also suggested progress through the upper chamber will not be straightforward.

A general election remains a possibility if the Conservative Government is hamstrung by opponents and feels the best way to gain a mandate is via the ballot box.

What does this mean to investors?

Investors should take nothing for granted. It is worth remembering that while there were a lot of political and economic surprises in 2016, the UK stock market gained for nine months in a row from February through October and looks likely to end the year higher than a year earlier.

Analysts are grudgingly starting to nudge up UK GDP forecasts following savage cuts after the 23 June referendum.

Retail spending has propped up the economy, the jobs market, while weaker, is not as chronic as feared and third quarter GDP at 0.5% was well above consensus.

But business investment intentions are softening, say analysts at Bank of America-Merrill Lynch. ‘Firms’ decisions seem to have been affected by uncertainty,’ writes BAML UK economist Robert Wood.

‘Job gains have slowed, jobless claims have risen and investment intentions dropped. The official employment rate fell again in September but for bad reasons (because people left the labour force rather than strong job gains). The news has not been all good since June.

Consumer confidence to fade?

Wood believes retail spending strength will fade next year as inflation squeezes spending power.

‘Consumer confidence has been supported by groups that favoured Brexit. Inflation will likely squeeze most of those people on fixed incomes.

‘If productivity continues to flatline and immigration slows then UK trend growth will be weak. It may just be a blip but we think it is worth noting that the total workforce fell in October. We need to keep a close eye on immigration flows.’

The economist says a ‘hard Brexit’ in which UK and EU governments engage in tit-for-tat disputes around key bargaining points remains his central scenario.

Since the publication of his research note on 23 November, the Government’s chief Brexit negotiator David Davis said payments into the EU budget might continue after the UK’s departure from the EU.

That prompted a rally in sterling as markets factored in a smoother and more amicable settlement between trading partners either side of the Channel.

Such a situation still looks a long way off at present and investors should probably avoid making investment calls based purely on winners and losers from the EU negotiations given the uncertainty. (WC)

Should UK investors care about European elections?

The last 12 months have seen considerable political upheaval and 2017 could offer more of the same as voters in the two remaining big European Union (EU) powers go to the polls.

Populist wave

The failure of many pollsters to predict a vote for Brexit in June and Donald Trump in the US presidential elections in November make it very difficult for markets to price in these events ahead of time and, as such, there is scope for considerable volatility.

The French presidential election is up first in the spring, followed by a federal election in Germany in the autumn. Of the two respective incumbents, president François Hollande and chancellor Angela Merkel, the former says he won’t stand for a second term. Merkel remains popular despite the impact of the refugee crisis.

France decides

The nature of the German system means it is unlikely any party will command an outright majority. Merkel and her Christian Democrats should therefore be able to form a coalition to hold off any challenge from the right wing populist Alternative for Germany party led by Frauke Petry and Jörg Meuthen.

The France election looks set to be a fight between the expected centre right candidate François Fillon and the leader of the far right National Front Marine Le Pen. The ultimate risk of a Le Pen presidency is that she would successfully lead France out of the EU, leaving the whole European project in tatters.

Stock implications

Viktor Nossek, director of research at ETF provider WisdomTree Europe, says such a situation would have all kinds of ramifications for all asset classes, starting with the euro and reverberating negatively into the banks.

If banks are most exposed to the systemic risks associated with any political shocks in 2017, which sectors could do well? Nossek thinks large technology and consumer discretionary stocks could continue to prosper thanks to their strong balance sheets and international horizons.

Matt Siddle, fund manager of Fidelity European Growth (LU0346388373), sees opportunities in the energy sector. ‘Many large cap energy stocks are trading at close to 60-year lows, while fundamentals continue to improve,’ he says. (TS)

What can trump deliver in his first 100 days?

US president-elect Donald Trump’s inauguration day is 20 January 2017. We expect his first 100 days in office to be closely watched by global stock markets.

Priorities may include pulling out of the Trans-Pacific Partnership, promoting production and innovation and loosening environmental restrictions to boost shale and clean coal industries.

Significantly, Trump’s victory has landed the Republican Party ongoing control of Congress, paving the way for major fiscal, monetary and regulatory changes with profound implications for sectors, the economy and the environment.

A ‘fiscal bazooka’ would boost growth and lead to higher inflation and faster rate rises, with Trump expected to prioritise tax cuts and spending increases, mainly for infrastructure.

What should we expect first?

One quick win in the first 100 days would be to rip up trade agreements with China in order to appease rust belt voters.

Marc Pullen, senior equity analyst at Canaccord Genuity Wealth Management, comments: ‘Which if any of his campaign promises Trump will implement is anybody’s guess, however presumably putting tariffs on Chinese imports and starting a tit for tat trade war will be far easier and a quicker win than building a wall across the Mexican border and deporting thousands of immigrants.’

Pullen says losers would be US companies with sales exposure to the Asia Pacific region (a proxy for China), while winners would be UK and European companies with sales exposure to Asia Pacific (filling the void left by the US). Potential winners might include Unilever (ULVR) over Procter & Gamble (PG:NYSE).

Shifting exposure

Michael Stanes, investment director at Heartwood Investment Management, says his focus is tilting portfolios towards a value bias.

He expects a Trump presidency will have a meaningful impact on sectors where he has stated ambitions: infrastructure, industrials, defensives and energy.

‘We therefore expect to shift exposure into these areas within our US equity allocation. With the support of a Republican Congress, Trump has a clear mandate to target growth through tax cuts and infrastructure spending.

‘Our portfolios have been focused on highly liquid US large caps, but we expect a Trump presidency to take on a more domestically-focused agenda and this could benefit US smaller companies. Over the medium-term, therefore, we have been recalibrating some of our US equity market-cap bias towards smaller companies.’

Geir Lode, head of global equities at Hermes Investment Management, sees Trumponomics as a further positive catalyst for banks, hurting since the financial crisis as ultra-low rates have eaten away at their top line.

Hermes believes higher rates will improve margins in a number of core banking services and lead to stronger earnings. ‘Furthermore, the recent rally of US banks also reflects the hope that the Republicans will cut red tape around regulations allowing banks to release greater amounts of capital or increase levels of lending.’ (JC)

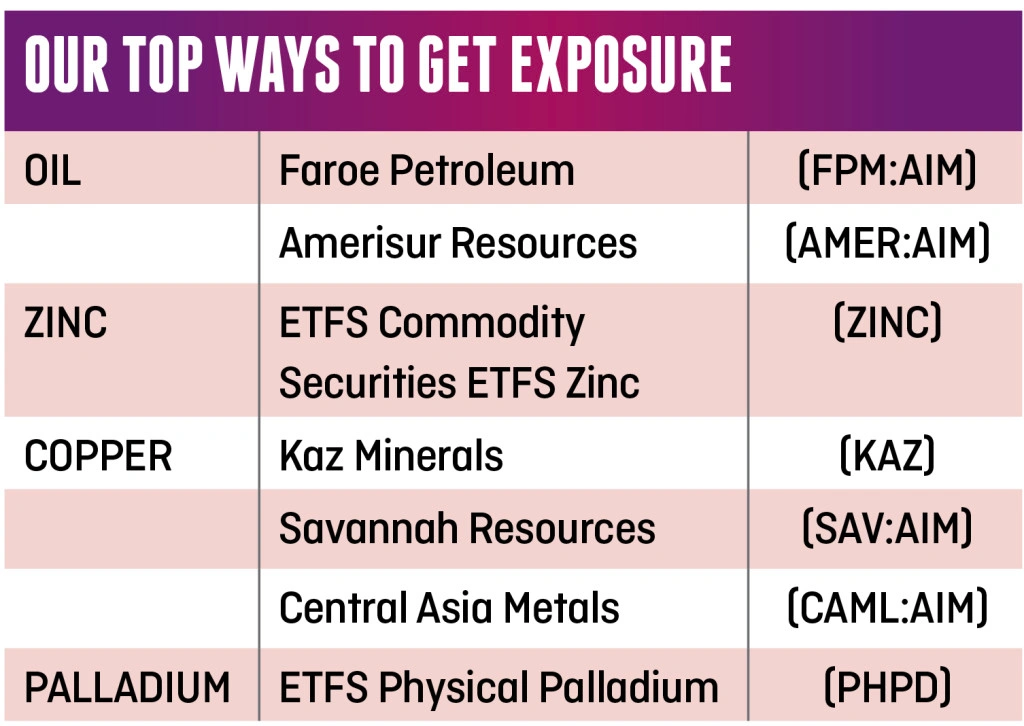

Will commodity prices have another strong year?

Oil, copper, zinc, nickel and palladium stand out as the best placed commodities for 2017, based on our analysis of various research notes.

We’re making the bold call that commodities – and therefore stocks in mining, oil and gas companies – will next year be a good place in which to invest. That is as long as China doesn’t destabilise the world economy by seeing its debt bubble burst.

There have been growing concerns in 2016 that China’s economy is on the brink of a large debt crisis. Even the Bank of England has publicly commented on the matter. In September, it said: ‘Credit growth in China continues to materially outpace GDP growth, and the level and growth of credit relative to GDP in China are very high by international standards.’

Positive signs

Mining stocks soared in 2016 on the back of good commodity prices gains. They’ve reaped the benefits of leaner business models, sterling weakness and hopes for resurgent demand.

Inflation is expected to rise next year in many parts of the world. Such economic conditions have traditionally pushed up commodity prices.

A recent acceleration in global PMI data also suggests demand is strengthening for commodities. PMI is an index that represents activity by purchasing managers across a range of businesses. PMI data is a reliable lead indicator of economic activity.

China and Euro Area manufacturing PMI data has been getting stronger every month since August, according to Markit Economics. Manufacturing activity in the US has displayed the same upwards trend since September, according to Markit PMI figures.

Goldman Sachs says commodity returns don’t depend so much on the rate of economic growth as they do on the level of demand relative to supply.

‘So while property-related demand growth in China is slowing, the level of demand is still very high requiring a high level of supply even if growth slows,’ it comments.

Bright spots

The oil price should benefit from production cutbacks as well as global economic growth.

Zinc is in a deficit position; however we would be more cautious on the metal pricing if the big producers like Glencore (GLEN) start to reopen mines previously suspended amid lower commodity prices. Copper is also forecast to be in deficit.

A pickup in industrial activity should support palladium. Demand is expected to outweigh supply in 2017 in what would be the sixth year of deficit in a row, according to industry expert Johnson Matthey (JMAT). It says tighter legislation should boost auto consumption, even if Chinese car sales slow.

‘Demand for palladium in auto catalysts, which turn noxious gasses into less harmful substances, is growing – due to rising sales of light and heavy-duty vehicle sales in China and Europe, and tighter emissions standards,’ says UBS. (DC)

Hot themes for 2017

Monetary policy vs fiscal spend

In 2017 the pendulum looks set to swing from the central bankers to politicians as monetary stimulus gives way to fiscal spending. Since the financial crisis, developed countries have adopted austerity policies and relied on interest rate cuts and so-called quantitative easing, aimed at boosting the supply of money, to boost ailing economies.

Now the focus has switched to tax cuts and increased expenditure on large scale projects, partly as a corollary of the populist revolt witnessed on both sides of the Atlantic.

Spending splurge

President-elect Donald Trump has pledged to spend at least $500bn on US infrastructure and lower corporation taxes. In the Autumn Statement UK Chancellor Philip Hammond announced a £23bn innovation and infrastructure fund.

At a stock market level this could be good news for stocks with exposure to government spending, specifically infrastructure specialists like Ashtead (AHT), CRH (CRH) and Hill & Smith (HILS).

It is potentially bad news for so-called ‘bond proxies’ in the utilities and consumer staples sectors if interest rates have to be hiked to counter any inflation brought on by the fiscal splurge.

Rising interest rates would be good news for the banking sector but this could be outweighed by the impact of political instability next year. (TS)

Can emerging markets regain strength?

Emerging markets were enjoying a major resurgence in 2016 until Trump's election. That's soured sentiment thanks to his trade protectionism and anti-immigration measures and uncertainty in terms of foreign policy.

Yet not all countries are dependent on trade with the US, such as India and Brazil.

A lot of people think emerging markets are very reliant on exports. That’s a common misconception, says investment bank Credit Suisse. It claims large domestic populations across Asia and Latin America, plus fast-growing middle classes, allows for substantial growth from within.

This is all macroeconomic stuff and not necessarily meaningful to smart stock pickers, such as Nitin Bajaj, who runs Fidelity Asian Values (FAS) fund. For him it’s all about keeping investment simple and buying good businesses with good management in the Warren Buffett vein. (SF).

MORE HOT THEMES FOR 2017

China debt bubble

China’s debt shot up from 154% of GDP in 2008 to nearly 250% of GDP in 2015. ‘The worry now is that this debt load is unsustainable, and will lead to a collapse in China’s FX reserves, massive defaults, capital flight and a financial meltdown,’ says Lombard Odier chief investment strategist Salman Ahmed.

‘Considering the size of China’s economy and its integration with the rest of the global economy, such a “hard landing” would be felt around the world.’

It’s easy to see why many investors are worried about China. Ahmed isn’t one of them. He believes China is rare in that its authorities have ‘enormous influence’ over the way markets function and plenty of tools to maintain stability.

We expect China’s debt situation to move higher up the news agenda in 2017 and wouldn’t be surprised to see a few bouts of negative stock market performance around the world as investors speculate over the country’s next move. (DC)

Inflation is back

Rising inflation precipitated by sterling weakness will be among the key themes in 2017 and could come down on average households like a ton of bricks.

Rising inflation could trigger interest rates hikes. It would also threaten retailers since consumers may feel less confident to spend money.

Investments suitable for an inflationary environment may include gold, commodity producers and real estate.

We’d also look for businesses with pricing power. Such companies can pass on extra input costs to customers by raising prices without denting demand and will be able to generate the profits and cash to fund progressive dividends that can not only match, but outpace the so-called ‘cruellest tax’. (JC)

Financial results to show more benefits of currency tailwinds

Expect some fairly punchy double digit revenue and profit growth numbers to be posted in early 2017 by a range of companies which earn most of their sales overseas.

Benefits to earnings from weaker sterling will be more apparent after the turn of the year when companies report year-over-year growth rates in the first quarter and first six months of the year.

Companies still need to be delivering decent underlying growth to enjoy decent share price performance around results, however, so investors should careful not to overpay for companies delivering growth which is mainly a result of currency moves. (WC)

Expect a further shift from defensives to cyclicals

There is a definite shift in investor appetite from high quality companies with pedestrian but semi-reliable growth, to stocks which could see rapid earnings growth if there is an improvement in economic conditions.

We noted this trend in 24 November issue of Shares – and it has become even more apparent going into December. On one hand this is bringing new life to some of the lower quality companies on the market; it is also making the high quality businesses a lot cheaper.

The challenge is whether to start snapping up the defensive companies now – or wait until they get even cheaper. Their downwards trends look strong at present, so we’d hold off in favour of finding better ‘bargains’ in the quality space later on. (DC)

SECTOR WINNERS AND LOSERS IN 2017

TECHNOLOGY - WINNER

It will be another exciting year for technological breakthroughs and advancement in 2017.

In 2016 we saw Elon Musk’s SpaceX launch and land the world’s first reuseable rocket. Cars started to park themselves; and Amazon (AMZN:NDQ) gave us Alexa, an in-home talking, music-playing, encyclopaedic assistant.

The next 12 months will see increasingly smarter stuff plus the acceleration of trends already disrupting consumers, businesses and governments.

Cyber security will be even hotter

Peel Hunt technology analyst Paraag Amin says data is a major theme for next year. He believes data is the ‘primary driver of business models, and the key to higher returns on investment,’ both inside and out of the technology sector.

Cyber security will be even more in demand in order to keep that data safe. Ali Unwin, manager of Neptune Global Technology Fund (GB00BYXZ5N79), says threats are changing every day.

‘One thing that Hillary Clinton and Donald Trump agreed on during the US election was more cyber security spending,’ Unwin points out.

New regulations during the next 12 months in the US and across the EU should force corporates and public organisations to address the multiple weaknesses in their operations, bolstering the opportunity for cyber security suppliers.

Unwin says to look at companies with high gross margins as one good measure of a quality business. We note GB Group (GBG:AIM) and Sophos (SOPH), both current top stock picks in Shares, run on attractive gross margins in the region of 77%.

More trips to the cloud

The Neptune fund manager believes more companies will move software services to the cloud. Suppliers should enjoy predictable cash flows and improved quality of earnings.

This chimes with the outsourcing theme flagged by Peel Hunt technology analyst Paraag Amin. ‘Where companies used to run things themselves (IT projects and system implementations, for example), now they are looking for specialist partners,’ Amin says.

That’s the sort of niche that Iomart (IOM:AIM) has been filling for several years. We would also expect 2017 to spark a recovery at network services group Redcentric (RCN:AIM) after its recent accounting issues.

Get ready for more takeovers

Mergers and acquisitions should be big news next year. Unwin says he has been told by industry contacts there is more private equity ‘dry powder’ on the sidelines than there’s ever been, referring to available cash that needs to find a home.

Hot targets are tech firms with solid overseas earnings from quality products or intellectual property (IP), strong cash generation and limited debt. Could this be the year someone buys ticketing technology specialist Accesso (ACSO:AIM)? (SF)

OIL SERVICES - WINNER

The impact of under-investment over several years could lead to a gradual rebalancing of the oil market in 2017. This would be beneficial to oil services stocks as prices recover and spending begins to ramp up.

The likes of Hunting (HTG), Weir (WEIR) and Wood Group (WG.) could also benefit from their exposure to a US shale sector bolstered by a newly supportive administration in the White House. True to form, the market has already started to price this in, reflected in a sector price to earnings ratio of 17.9 times. However, these estimates are likely to be pitched at conservative levels after a long spell of disappointing operational performance. (TS)

ENGINEERING - WINNER

Weaker sterling should provide a rare boost to the UK manufacturing and engineering sectors in 2017.

After decades of struggles with higher costs at home, many have developed offshore production centres which would tend to reduce the benefit received from the currency drop.

Renold (RNO) is one such company; while it generates much of its sales abroad, production is now based all around the world. It will still benefit from the weaker currency though less so than if it produced products in the UK.

Hayward Tyler (HAYT:AIM)

is another; a new manufacturing facility in Luton might provide it more flexibility to take advantage of a more cost competitive UK export market in 2017. We’d also flag Castings (CGS).

Longer term, there are risks to manufacturing and export sectors more generally in the UK if it goes down a free trade post-Brexit route as EU protectionist tariffs versus the rest of the world are scaled back. (WC)

RETAIL - LOSER

June’s vote for Brexit only compounds the problems facing the retail sector, which Shares expects will have a tough time in 2017. Weak sterling and the prospect of a return to falling real incomes are set to sap UK demand.

Over-capacity on the high street is endemic and the need to embrace omni-channel retailing only adds to the costs of shopkeepers whose margins are being squeezed by business rates, higher wage bills and a further expected decline in the pound.

Higher inflation on the horizon will be a challenge for retailers in 2017, since the spending power of consumers will change.

On the positive side, weak sterling could attract more tourists so retailers may get some relief from increased spending by overseas visitors.

Lower consumer confidence or financial distress may drive people towards domestic holidaying which could be another boost for many UK retailers. (JC)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.