Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineDoes Royal Mail owner International Distributions Services hold a 'hidden store of value’?

Being a value manager often means taking a positive view on a stock which seems to be universally unloved and facing plenty of headwinds, which is certainly the true in the case of logistics firm International Distributions Services (IDS).

The FTSE 250 company, which recently changed its name from Royal Mail Group to emphasise its international scale, has delivered a string of profit warnings and is dealing with large-scale industrial action and a cybersecurity attack, so why on earth would investors be interested?

We look at the pros and cons of the business and talk valuation with one of its biggest shareholders.

HIGHS AND LOWS

It has been an odd few years for IDS, with revenues and earnings getting a big boost from the shift to e-commerce during the pandemic and the shares more than quadrupling from 124p in March 2020 to more than 600p by June 2021.

The good times didn’t last, sadly, and the shares have since lost 75% of their value after a series of earnings downgrades and repeated warnings the firm isn’t doing enough to reshape Royal Mail in light of the trend away from traditional UK delivery services, in particular the sending of letters.

Group results for the half-year to September showed a 4% drop in group revenues to £5.84 billion and an operating loss of £163 million against a profit of £311 million the previous year.

All the damage was due to Royal Mail, which posted a 10.5% decline in revenue to £3.65 billion and operating losses of £219 million against prior-year profits of £235 million ‘driven by weak parcel volumes, inability to deliver productivity improvements and impacts from industrial action’.

GLS, the international distribution business, reported a 9.5% increase in turnover to £2.2 billion and a slight drop in profits to £162 million due to rising costs.

In a 26 January trading update there was no change to the firm’s full-year profit guidance, which in some ways was a blessing as it meant no further downgrades. It said strikes had cost the business £200 million over nine months.

DAMAGED GOODS?

The reality is the group’s future profitability hangs on right-sizing Royal Mail and getting agreement with the unions over pay and working hours.

Repeated strikes over Christmas will undoubtedly have damaged the company’s franchise and seen some customers choose rival services to ensure delivery – winning them back will be an uphill task.

At stake is Royal Mail’s 30% share by value of the £15 billion a year UK parcel market, which Ibis Research estimates will keep growing at 5% per year between now and the end of 2027.

Challengers such as Evri, formerly Hermes, pitch themselves as ‘disruptors’, offering a cheaper service with late cut-off times for retailers, making it attractive for e-commerce customers, and contracting out last-mile delivery to ‘gig-economy’ drivers.

IDS’s reputation has been further damaged by a cyber incident which caused ‘severe disruption’ to Royal Mail’s export service meaning it was unable to send letters and parcels to overseas destinations.

The company had to ask customers temporarily to stop submitting export items into the network while it worked to resolve the issue, but the issue raises questions over the level of investment needed in its systems and security.

TAKING A LONG-TERM VIEW

Given the headwinds facing the business, it’s reasonable to ask why anyone would even think of buying shares in International Distributions Services.

The company seems to be in a perpetual state of turmoil, unable to satisfy the public or its employees, yet two big investors are prepared to ignore the noise and focus on what they see as the firm’s hidden value.

VESA, controlled by Czech investor Daniel Kretinsky, is not only the largest shareholder but has been steadily increasing its holding and now owns a 23.2% stake.

Redwheel, which manages Temple Bar (TEMPL) among other funds, owns 9.5% of IDS and shares the same vision for the firm as VESA.

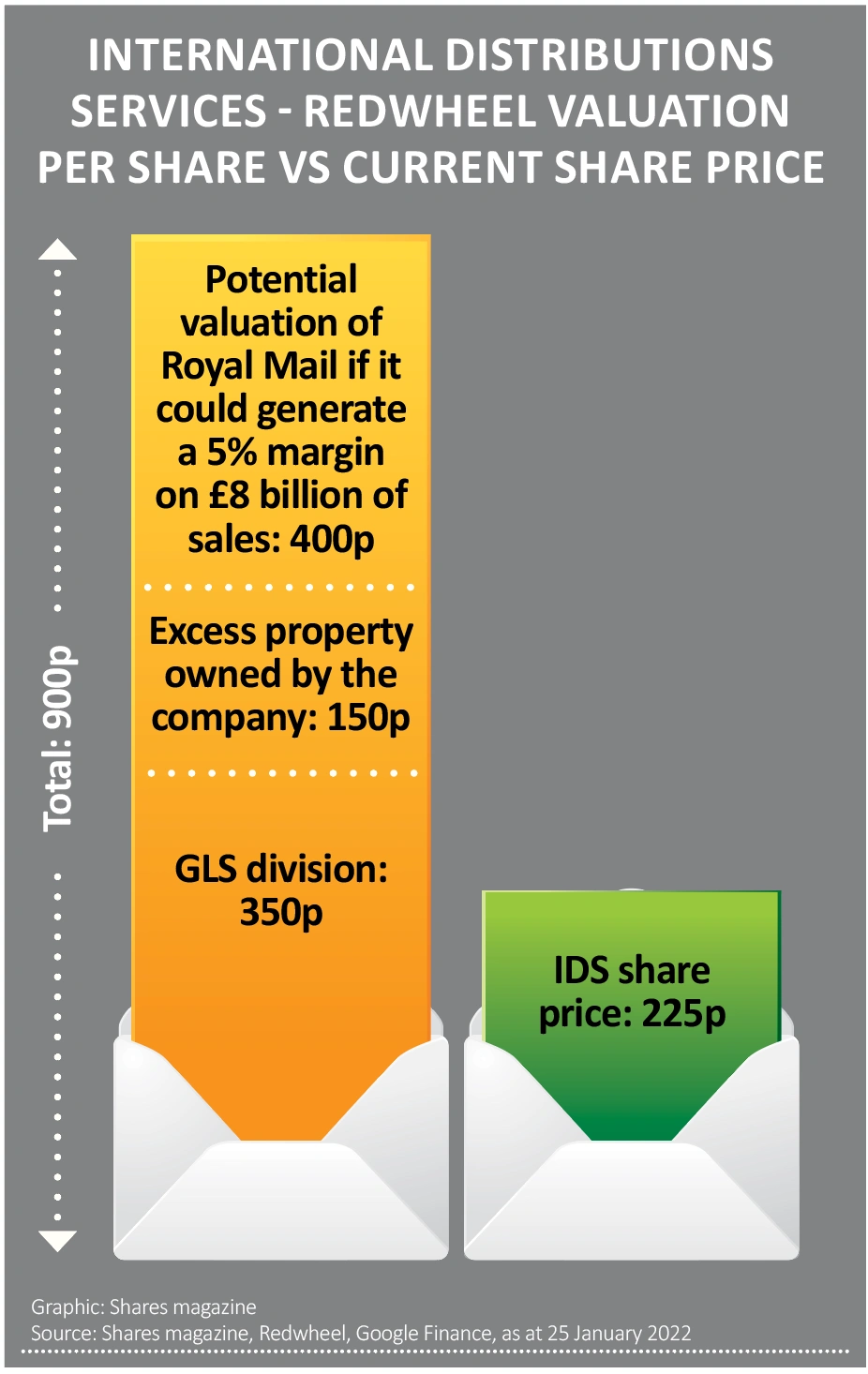

Ian Lance, co-head of the UK Value and Income team at Redwheel and co-manager of Temple Bar, believes the GLS division of IDS is ‘as good as any European logistics company’.

For the year to March, GLS is expected to make around £350 million of operating profits, which on a multiple of 10 times would mean a value of £3.5 billion or roughly 350p per share, argues Lance.

Royal Mail owns excess property worth another 150p per share, has little debt aside from leases and has a pension surplus, which takes the value of IDS shares to 500p even ascribing zero value to Royal Mail’s operations, against a current share price of 225p.

If, and admittedly it is a big if, Royal Mail turned a 5% margin on say £8 billion of annual sales, in theory it could be worth 400p per share.

‘The market is only looking at the next quarter, whereas we’re looking at the next five to seven years,’ says Lance, in which time he expects the company to be broken into two share classes with most investors preferring to own GLS while Royal Mail may offer ‘option value’.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Feature

- Terry Smith reveals one of his biggest mistakes with Fundsmith Equity Fund

- China versus India: What you need to know before you invest

- Why bonds are back, how to invest in them and our best pick

- Does Royal Mail owner International Distributions Services hold a 'hidden store of value’?

- Paying the bills: How to get £1,500 post-tax monthly income in retirement

Great Ideas

News

- Why Caterpillar's results are better news for wider economy than itself

- Why Alphabet should be afraid of Microsoft’s $10 billion investment into ChatGPT

- New boss has his say as Rolls-Royce stages big share price recovery

- Weakness in the chip industry could spell trouble for the whole tech sector

- Why British American Tobacco has run out of puff