Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

“For the second time in a row, silicon chip specialist NVIDIA has hugely outstripped analysts’ expectations for quarterly earnings and raised guidance for the next three months to levels that also exceeded forecasts, as the artificial intelligence (AI) and machine learning boom continues,” says AJ Bell Investment Director Russ Mould.

“Given the scale of the upside surprise on both counts – guidance for the next quarter’s sales and profits are a fifth higher than the consensus before the release of the figures on Wednesday night – shareholders could almost be forgiven for being disappointed with the ‘mere’ 10% jump in the share price in after-hours trading. However, the shares are up by more than 50% since May’s first-quarter results and the company now has a market cap of $1.1 trillion, a lofty price tag that means expectations for growth are already extremely high indeed.

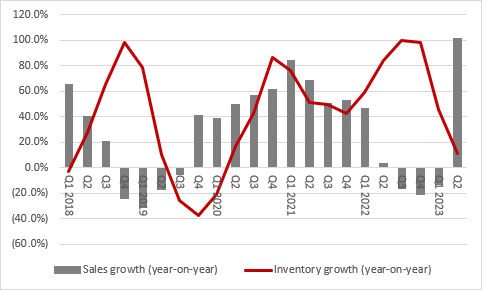

“Last year’s share price slump after a profit warning, a slowdown in demand for graphics card sales and a surge in inventory all seem like a distant memory after another incredibly strong three months of trading and chief executive Jensen Huang is still flagging AI as a key driver of increased demand.

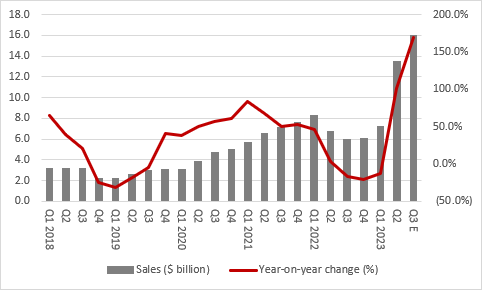

“Second-quarter sales came in at $13.5 billion, up from $7.2 billion in Q1 and ahead of the consensus forecast of $11 billion.

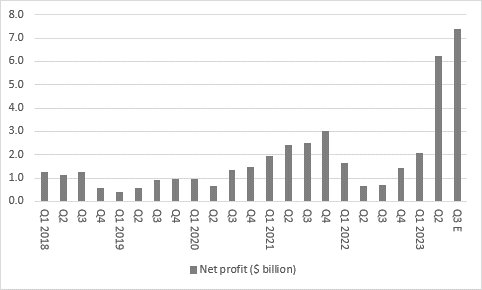

“Net income reached $6.1 billion, up from $2.0 billion in Q1 and comfortably ahead of Mr Huang’s own guidance back in May for a figure around $5 billion.

“Bulls of the stock could also draw encouragement from how inventory dropped by another $300 million to $4.3 billion, to bolster the argument that 2022’s slowdown in sales and surge in unsold product was just a blip. Revenue growth is easily exceeding the increase in inventory once more.

Source: Company accounts

“That helped to take inventory days down to 97 from 165 at NVIDIA, which designs its chips but then outsources the manufacturing process, primarily to Taiwan’s TSMC, the world’s leading semiconductor foundry.

Source: Company accounts

“That is much more in line with recent norms and helps to set the scene for the third quarter, as demand surges thanks to the shift towards generative AI and accelerated computing, whereby core control remains on the central processing unit (CPU) and data-intensive tasks are managed by a separate acceleration device.

“NVIDIA is guiding Q3 sales to $16 billion, miles above the consensus of $11.9 billion and the $5.9 billion achieved in the same three-month period a year ago.

Source: Company accounts, Zack’s, NASDAQ, analysts’ consensus forecasts, company guidance

“Mr Huang’s guidance for cost of goods, operating expenses, interest expense and tax imply a net profit of some $7.4 billion, a figure that comfortably exceeds the quarterly record of $3 billion chalked up in the final quarter of 2021.

Source: Company accounts, Zack’s, NASDAQ, analysts’ consensus forecasts, company guidance

“The monster market capitalisation – which before the latest, inevitable round of upgrades left the stock trading on 25 times forecast sales and 70 times estimated profits for the year to January 2024 – needs this sort of momentum so it can be justified. Those lofty multiples explain why such a huge upside surprise for Q2, and 20%-plus upgrade to estimates for Q3, translated into ‘just’ a 10% jump in the shares after hours (although that is still another $100 billion or so in market value).

“For the moment, though, the AI hype-train is not only rolling but delivering, as far as NVIDIA is concerned. Momentum investors seem happy to pile in, although value seekers are likely to be more reticent, given those valuation multiples which leave little room for error.

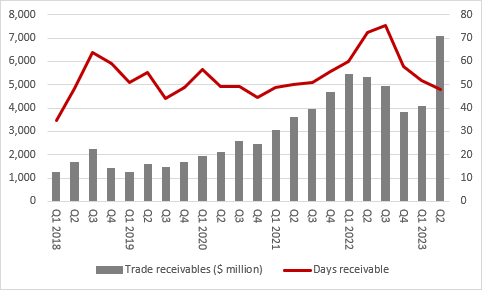

“Bears have little to chew upon, and the only thing that may offer sceptics some scope to cavil is a jump in trade receivables, as this implies that NVIDIA booked revenues on chips which it had shipped but for which it had not been paid.

Source: Company accounts

“Sceptics may also view a bulge in receivables as suspicious, as it could represent channel stuffing or some other accounting sleight of hand to make or beat a quarterly target.

“Bulls will simply assert that demand is red hot, and NVIDIA is having to do all it can to ease bottlenecks and get product to customers who seem desperate for it. The drop in days receivable would seem to support this argument.”

These articles are for information purposes only and are not a personal recommendation or advice.

Related content

- Wed, 01/05/2024 - 18:32

- Wed, 24/04/2024 - 10:37

- Thu, 18/04/2024 - 12:13

- Thu, 11/04/2024 - 15:01

- Wed, 03/04/2024 - 10:06