Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

- Even though they have more than doubled from 2022’s lows, shares in Netflix are pretty much flat over the past year and still 50% below their autumn 2021 peak.

- Bulls will argue the rally is justified because the initial fall was out of proportion to two quarters of missed subscriber growth estimates in the first half of 2022. They will also point to the rich catalogue of content and strong slate of shows, the launch of a new discounted ad-funded price package designed to win new subscribers and improved net customer additions in the second half of last year – Netflix added 7.7 million subs in Q4, well ahead of management’s guidance of 4.5 million.

- Bears will point to increased competition; the surging cost of content production; spotty cash flow; a balance sheet that carries not just $9.3 billion of net debt, but more than $2 billion in leases and nearly $22 billion in guaranteed content purchase obligations; and a $151 billion market cap that still puts the stock on around 30 times earnings for 2023, even though analysts believe earnings per share will grow at a low-teens percentage rate this year.

- The first number that analysts and shareholders will look for is net subscriber additions. After shedding 203,000 net subscribers in Q1 and 969,000 in Q2 (and that was much less than management’s forecast of an initial loss of two million), Netflix added a better-than-expected 2.4 million in Q3 and then a strong 7.7 million in Q4, to leave the company with 230.7 million paying subs at year end. Note that Europe, Middle East and Africa (76.7 million) and the combination of Asia and Latin America (79.7 million) were both bigger than the USA by the end of 2023.

Source: Company accounts

- Netflix no longer provides guidance for subscriber additions and focuses instead on revenues, operating margin and cashflow but the management team – executive chairman (and founder) Reed Hastings and co-chief executives Ted Sarandos and Greg Peters did suggest that paid adds growth would be “modest” in Q1, thanks in part to the strong Q4 and the possible impact of paid sharing, which management believes will lead to US, Asian and European cancellations, based on their experiences in the Latin American markets. Adds are expected to come in higher in Q2 than in Q1 (which would be unusual for the seasonality shown by the business to date).

Source: Company accounts, management guidance for Q4 alongside Q3 results

- Alongside the Q4s, management forecast the following for Q1:

- Revenue growth of 4% on a stated basis to $8.2 billion, and 8% higher adjusting for currency movements.

Source: Company accounts, management guidance alongside Q4 2022 results, Zack’s, NASDAQ, analysts’ consensus forecasts

- A first-quarter operating margin of 20%, compared to 25% in Q1 2022, thanks to investment in content and marketing spend. That implies an operating profit of around $1.6 billion, down from $2 billion in the equivalent quarter a year ago. The long-term goal remains an operating margin of 19% to 20% and management expects 18% to 20% for this year, taking into account currency movements.

Source: Company accounts, management guidance for Q1 2023 alongside Q4 2022 results

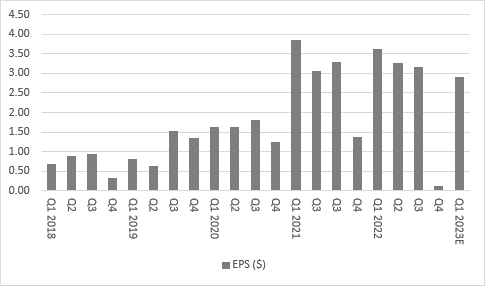

- In terms of the expected headline earnings per share (EPS) figure for Q1, the range of estimates is unusually narrow, at $2.72 to $2.84. The consensus is $2.81 compared to $3.53 a year ago. As if to reflect just how tight that consensus range is, there has been just one change to estimates in the past 60 days (and that was an upgrade), according to Zack’s.

Source: Company accounts, Zack’s, NASDAQ, analysts’ consensus forecasts

- Should management give any guidance for Q2 (and they usually do), then the current consensus forecasts are as follows:

- Sales of $8.4 billion (versus the consensus estimate of $8.2 billion in Q1 and $8.0 billion in Q2 2022)

- EPS of $2.93 (versus the consensus estimate of $2.81 in Q1 and $3.20 in Q2 2022)

Source: Company accounts, Zack’s, NASDAQ, consensus analysts’ forecasts

- Current consensus estimates for the whole of 2023 are:

- Sales of $34.2 billion (8% higher than 2022’s $31.6 billion)

- EPS of $11.28 (13% higher than 2022’s $9.95)

These articles are for information purposes only and are not a personal recommendation or advice.

Related content

IG Design’s full-year update paints a brighter picture

- Wed, 01/05/2024 - 18:32

- Wed, 01/05/2024 - 18:32

AB Foods serves up strong first-half results

- Wed, 24/04/2024 - 10:37

- Wed, 24/04/2024 - 10:37

ASOS looks to better times ahead

- Thu, 18/04/2024 - 12:13

- Thu, 18/04/2024 - 12:13

Is it time to start surfing the silver price?

- Thu, 11/04/2024 - 15:01

- Thu, 11/04/2024 - 15:01

How to choose a gold mining stock

- Wed, 03/04/2024 - 10:06

- Wed, 03/04/2024 - 10:06