Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

“Soft-drink maker AG Barr now expects its full-year pre-tax profit to exceed pre-pandemic levels but the Scottish firm’s shares still languish nearly 20% below where they were trading February 2020 as the virus first reached Western Europe and markets began to take its threat seriously,” says AJ Bell Investment Director Russ Mould.

“This may seem surprising when the company is also back on the dividend list and can point to a net cash balance sheet but analysts and investors could be worrying about pressure on profit margins, something that chief executive Roger White warned about alongside the first-half results back in September.

Source: Refinitiv data

“Boosted by improved demand from consumers ‘on the go’ and the hospitality industry, the maker of Irn-Bru now believes that sales for the full-year to January to reach £264 million and pre-tax profits to hit £41 million.

“Those numbers compare to the £256 million and £37.4 million achieved in the year to January 2020, before the pandemic hit home.

Source: Company accounts, management guidance for 2022E. Financial year to January.

“Given AG Barr has net cash on its balance sheet, that pre-tax profit forecast implies an operating profit for the year to January that is a little bit higher (but only a little bit, owing to record-low interest rates).

“But an operating profit of around £41.5 million for the full year to January compares to the £24.6 million racked up in the first half and implies a profit of around £17 million in the second. That in turn suggests the operating margin fell from 18.2% to just over 13% on the second.

Source: Company accounts, management guidance for H2 2022E. Financial year to January

“Management had flagged this as a possibility back in September, given how restocking by bars and restaurants and the phasing of marketing investment had boosted first-half profits by some £5 million.

“Investors will be reassured to some degree by Roger White’s comments that the company has overcome supply chain issues to meet volume demand, although they will note the warning about ‘ongoing cost pressures,’ given challenges such as the availability of both carbon dioxide and haulage capacity, as well as wider input cost pressure.

“An operating margin for the full year of more than 15.5% is hardly a disaster and it exceeds the 14.9% generated in the year to January 2020. This points to the power of AG Barr’s

well-nurtured range of brands, which includes not just Irn-Bru but Funkin’ and also Rubicon, which is launching a new range of energy drinks to attack that fast-growing market. Those brands, which survived the last carbon dioxide shortage three years ago, as well as the launch of the sugar tax in the same year, bring pricing power.

“That could be a very useful facet if input cost increases prove persistent not least because pricing power helps to generate and defend high profit margins and high returns on capital.

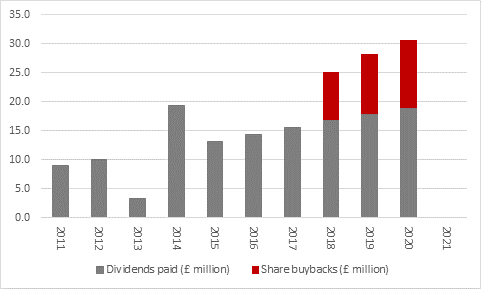

“Double-digit profit margins and returns on capital in turn help to support cash flow, which funds further investment in the business and those brands and then finally returns to shareholders, in the form of dividends or even share buybacks. After October’s payment of the 2p-a-share interim dividend and the 10p-a-share special, the Scottish firm has returned more than £150 million in dividends alone to its shareholders since 2011.

Source: Company accounts. Financial year to January.

“AG Barr also ran share buyback programmes in its 2018, 2019 and 2020 financial years with a combined worth of £30 million, to take total cash returns over the decade to over £180 million.

“That is almost a third of the company’s current total market capitalisation and patient shareholders may well decide to stick with the shares, as a result, looking through the near-term uncertainties in the view that face the business in the view that its brands will, as before, bring it through.”

These articles are for information purposes only and are not a personal recommendation or advice.

Related content

- Wed, 08/05/2024 - 11:46

- Wed, 01/05/2024 - 18:32

- Wed, 24/04/2024 - 10:37

- Thu, 18/04/2024 - 12:13

- Thu, 11/04/2024 - 15:01