Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

Softbank’s decision to list ARM on the New York Stock Exchange, rather than its London equivalent, and a seemingly growing queue of FTSE 100 firms that desire to switch their listing Stateside, is causing much angst and prompting the London Stock Exchange to ease its rules for new market entrants.

This raises two issues. The first is investor protection and whether the risk profile of the London market will increase as a result of the proposed changes. The second is valuation and the relative price tags attached to American and UK equities.

The number of firms that are thinking of switching their listing to New York from London seems to be growing. This is, in turn, is leading to much handwringing and comment that London is in decline as a financial centre, as well as proposed reforms from the London Stock Exchange to ease its listing requirements and by implication lessen investor protections.

It is hard to see how increasing the risks facing investors can help the London market over the long term, as the authorities prepare to admit firms without even three years of accounts or let related party transactions go through on the nod without a shareholder vote. This, it could be argued, means the Main Market increasingly comes to resemble the junior AIM market, whose own boom in new issuance spawned more than one scandal and in turn led to tighter regulation and a less laissez-faire approach in the early 2000s.

Source: London Stock Exchange

Loosening listing rules may help advisers, brokers and lawyers (as well as sellers of the paper) make a quick buck, but whether this creates a thriving environment for investors and potential buyers of newly-listed stock remains to be seen. It seems doubtful, for as John Maynard Keynes once tersely noted, When the capital development of a country becomes the key product of a casino, the job is likely to be ill done.”

But there is another potential issue which investors should ponder, as ARM, CRH and Flutter Entertainment consider following in the footsteps of Ferguson and decamping from London to New York, and that is valuation, for two reasons.

First, if the proposed reforms do open up investors to more risk on the London market, then investors will demand a higher return to compensate themselves for that, and they will do so by paying a lower multiple of price. The changes could therefore be self-defeating.

Second, investors – and executives – must take a view on whether US equities are appropriately valued.

According to analysts’ consensus estimates, Standard & Poor’s and FactSet, America’s S&P 500 index trades on around 20 times forward earnings for 2023 and 18 times for 2024. The FTSE 100, by contrast, is currently afforded forward price/earnings (PE) multiples of 11.5 times and 11.0 times, respectively. What stock-and-options laden executive would not consider switching their listing if it offered the prospect of a near-doubling in rating and therefore potentially also share price?

Investors may be tempted to tag along for the ride, but they must consider the implications.

Why is the shift taking place? If it is because the bulk of the assets are there, or the bulk of the employees, then it makes perfect sense for reasons of managing currencies, reporting, and making stock and dividend payments to staff and shareholders as efficient as possible from a tax and currency point of view. It may provide a currency for acquisitions. These all may help support and enhance the competitive position of the business, which is ultimately what the investor buys into when they acquire stock.

But if it is just a matter of financial engineering and hoping for a higher rating, then the benefits are potentially more ephemeral. And if the firm is listing in one place rather than another simply so it can get a higher earnings multiple and the vendor can sell the stock more expensively, in whose interest is that?

It may help the vendor, as in the case of Softbank with ARM, as the Japanese technology incubator looks to raise cash and prove it is not an indebted mess that just got lucky with one early-stage investment in Alibaba. But if the vendor is getting a higher price, then the implication is that there is less on the table for the investor as the buyer.

Any executive who switches their listing to the USA to get a higher rating and higher share price and then continues a share buyback programme too should come in for serious criticism, because the numbers then don’t make sense, as the chances of a buyback creating value go down just as fast as a share price goes up.

Executive teams and investors alike should also consider another issue before they hitch themselves to the momentum of the US equity market.

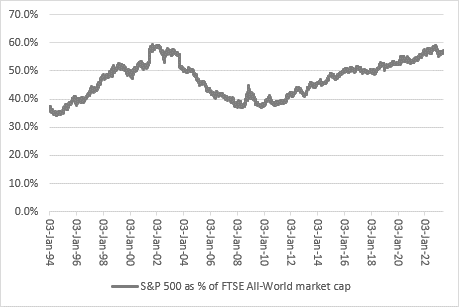

The S&P 500’s market cap is near its all-time high relative to that of the FTSE All-World. The last time it was this high, at roughly 60%, the US stopped outperforming and started underperforming, weighed down by a valuation that proved unsustainable as the technology, media and telecoms bubble burst. Indeed, it already looks like the US is gently underperforming other equity markets, almost unnoticed.

Source: Refinitiv data

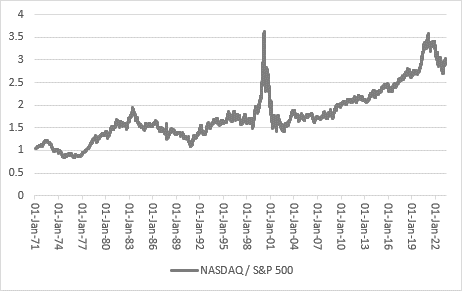

Within that context, the tech-laden NASDAQ has undeniably outperformed the S&P easily for many years. But its relative rating is now also just coming off an all-time high, even as most commentators continue to champion the sector.

Source: Refinitiv data

Executives – and investors – looking to piggy-back US tech stock momentum in search of a pay day should perhaps bear this in mind, just in case they hook up with something that is losing pace, rather than gaining it.

These articles are for information purposes only and are not a personal recommendation or advice.

Written by:

Russ Mould

Russ Mould has 28 years' experience of the capital markets. He started at Scottish Equitable in 1991 as a fund manager and in 1993 he joined SG Warburg, now part of UBS investment bank, where he worked as equity analyst covering the technology sector for 12 years. Russ joined Shares in November 2005 as technology correspondent and became Editor of the magazine in July 2008. Following the acquisition of Shares' parent company, MSM Media by AJ Bell Group, he was appointed AJ Bell’s Investment Director in summer 2013.

Related content

- Mon, 29/04/2024 - 09:30

- Wed, 17/04/2024 - 09:52

- Tue, 30/01/2024 - 15:38

- Thu, 11/01/2024 - 14:26