VOL 24 / ISSUE 36 / 15 SEPTEMBER 2022 / £4.49 Companies which can ride out the storm SURVIVORSRETAILSURVIVORSRETAIL What further hikes from the Bank of England would mean for stocks4% INTEREST RATES:

ThinkThinktemplebarinvestments.co.ukvalueinvesting?TempleBar

For further information, please visit

The Temple Bar Investment Trust is well placed to benefit from a continued rotation into UK value stocks. That’s why, if you want to gain exposure to the UK value opportunity, you should consider Temple Bar.

Temple Bar Investment Trust is a well-established investment company with a disciplined, value-oriented investment approach. Managers Nick Purves and Ian Lance have more than fifty years of investment experience between them and are focused on investing the Temple Bar portfolio in businesses that they believe are available at a significant discount to intrinsic value.

No investment strategy or risk management technique can guarantee returns or eliminate risks in any market environment. Investments can go up and down in value and you may not get back the full amount invested. The information shown above is for illustrative purposes only and is not intended to be, and should not be interpreted as, recommendations or advice. RWC Asset Management LLP is the appointed portfolio manager to the Temple Bar Investment Trust Plc, and is authorised and regulated by the Financial Conduct Authority.

“UK stocks look attractively valued in a global context and when compared to history. We believe that recent market behaviour suggests the stars are aligned for an improvement in the performance of value stocks in the years ahead. Timing such a change in market conditions precisely is always difficult, but the long-term opportunity for UK value investors is significant.”

Ian Lance, Portfolio Manager, Temple Bar Investment Trust

This discipline is known as value investing, and it has a very long history of outperformance. More recently, however, it has struggled in the growth-dominated markets of the last decade. Many investors have abandoned the approach as a result, but recent market behaviour suggests value investing may be resuming its former dominance.

05

Cash rates are improving: this is what you need to know

Why high returns can sometimes justify high ongoing fee charges

What now for European stocks as ECB unveils new record hike?

VIEWEDITOR’S

FEATURE AMC’s new preferred stock explained

Members of staff of Shares may hold shares in companies mentioned in the magazine. This could create a conflict of interests. Where such a conflict exists it will be disclosed. Shares adheres to a strict code of conduct for reporters, as set out below.

FEATURE What would interest rates at 4% mean for investing in stocks?

26

FEATURE Is weakness in Somero Enterprises shares a great opportunity or a value trap?

Shares publishes information and ideas which are of interest to investors. It does not provide advice in relation to investments or any other financial matters. Comments published in Shares must not be relied upon by readers when they make their investment decisions. Investors who require advice should consult a properly qualified independent adviser. Shares, its staff and AJ Bell Media Limited do not, under any circumstances, accept liability for losses suffered by readers as a result of their investment decisions.

TRUSTSINVESTMENT

1. In keeping with the existing practice, reporters who intend to write about any

22

Why the food delivery story has stalled and what the big names can do to recover

2. Reporters will inform the editor on any occasion that they transact shares, derivatives or spread betting positions. This will overcome situations when the interests they are considering might conflict with reports by other writers in the magazine. This notification should be confirmed by e-mail.

06

New: Pernod Ricard / Bellevue Healthcare Trust

38 ASK TOM How big a pot of money do I need to retire on? 41 INDEX Shares, funds, ETFs and investment trusts in this issue

FEATURE Retail survivors: companies which can ride out the storm

NEWS

Updates: CentralNic

4. A reporter should not have made a transaction of shares, derivatives or spread betting positions for 30 days before the publication of an article that mentions such interest. Reporters who have an interest in a company they have written about should not transact the shares within 30 days after the on-sale date of the magazine.

19

FINANCEPERSONAL

36 HEWSONDANNI

IMPORTANT

Truss plan for energy independence fires up the oil and gas sector

3. Reporters are required to hold a full personal interest register. The whereabouts of this register should be revealed to the editor.

15 September 2022 | SHARES | 3 Contents

IDEASGREAT

14

FEATURE

30

DISCLAIMER

securities, derivatives or positions with spread betting organisations that they have an interest in should first clear their writing with the editor. If the editor agrees that the reporter can write about the interest, it should be disclosed to readers at the end of the story. Holdings by third parties including families, trusts, self-select pension funds, self select ISAs and PEPs and nominee accounts are included in such interests.

09

29

33

US inflation proves stickier than hoped as UK introduces energy bill freeze / UK tech in the sights of private equity again as GB targeted / Two new alternative investment trusts prepare for main market listing

Capital at risk. Pension rules apply. YOURRETIREMENTWAY? Open our low-cost Self-Invested Personal Pension for total flexibility and control over your retirement with free drawdown. youinvest.co.uk SIPPs | ISAs | Funds | Shares

he European Central Bank’s decision to lift rates by a record 75 basis points (8 September) came as no surprise. After all it was playing catch up with its global counterparts in moving to address the current inflationary pressures by lifting rates.

However, there’s still a good chance European shares could get even cheaper in the eyes of the investment bank’s equity strategy team, led by the widely-followed Graham Secker.

Given that prior to July’s 50 basis point increase rates had been at our below zero for some time this would represent a big change and could exacerbate a downturn in the Eurozone economy.

What are the implications for European stocks and just what has been priced in by markets? There is no doubt the European market trades at a significant discount to the US market and materially below its long-term average. This has happened despite European earnings being upgraded by 14% in 2022 according to Morgan Stanley.

Secker and his colleagues see a risk that the price to earnings ratio for European stocks will hit 10 times, implying a double-digit fall from current levels.

Secker and co also observe that the 17% increase in earnings per share forecast for 2022 would have been just 7% if you strip out the impact of the energy sector. They also argue forecasts for

2023 earnings growth of 2% look optimistic given a highly uncertain backdrop – not least the pressure on margins from soaring input costs. What about the longer-term picture though?

Writing in July before the most recent surge in gas prices which greeted Russia’s shutdown of the Nord Stream 1 pipeline, BlackRock argued: ‘Europe is home to many “best-in-class” companies that we believe are well positioned to help global governments meet their net-zero emissionsBlackRocktargets.’adding that: ‘We believe European stocks now represent good value for investors seeking to capitalise on recent market volatility to gain exposure to long-term structural trends – such as the shift to a net-zero future.’

What now for European stocks as ECB unveils new record hike?

They comment: ‘We remain cautious on European equities against a backdrop of heightened geopolitical/energy uncertainty and where central banks continue to tighten monetary policy into a deepening economic slowdown.’

T

The argument over European valuations won’t dissipate soon, barring a miraculous turnaround in fortunes. What is true is European stocks are often unfairly overlooked by UK investors given the breadth and depth of the market and Shares will continue to look to mainland Europe for quality opportunities even as this valuation debate continues toByrage.

The ECB has different considerations than other central banks because it has to manage the interests of a whole economic bloc but Reuters has reported sources outlining a scenario where rates may have to increase to at least 2%.

Tom Sieber Deputy Editor

A debate is raging about the valuation of shares on the Continent

15 September 2022 | SHARES | 5 EDITOR’S VIEW

Fears about the inflationary backdrop were stoked once more by a reading of US inflation for August which came in hotter than expected, with CPI (consumer price index) up 8.3% year-on-year against the 8.1% forecast.

In terms of growth, September will most likely be a sombre month in more ways than one with many events postponed, a more reflective bank holiday than usual and subdued trading in hospitality and in-store.

Much of governor Bailey’s concern for the economy is rooted in fears of soaring inflation due to the October hike in energy prices and a consequent collapse in confidence and spending by businesses as well as consumers.

NEWS 6 | SHARES | 15 September 2022

And although average petrol prices are still around 25% higher than they were in 2021, they have been falling for the last two months which has eased some of the pressure on households, with the RAC predicting further falls to come.

So, with both price rises and activity slowing, all eyes are on the Bank of England’s meeting next week. [IC]

The CEBR (Centre for Economics and Business Research) estimates that capping energy bills at £2,500 from October could reduce peak inflation by as much as 5% by early 2023.

UK Bank of England Base Rate 2010 2015 2020Chart:420 Shares magazine • Source: Refinitiv

Bank of England governor Andrew Bailey recently predicted a recession could start in the final quarter of this year, after the bank raised rates by the most in 27 years in order to head off double- digit inflation. Some comfort may have been taken from UK CPI data which showed inflation slowed for the

Perhaps of more concern was the fact core CPI (stripping out the impact of volatile food and energy prices) was up 0.6% month on month, double what had been pencilled in ahead of time.

US inflation proves stickier than hoped as UK introduces energy bill freeze

first time in a year in August to 9.9%, but prices for key items are still rising fast. And while a slump in the UK economy might not be as deep as the 2008 financial crisis, it could last as long warned Bailey. Yet, while it clearly isn’t in rude health, the economy continues to plodJune’salong.disappointing growth in GDP (gross domestic product) was due in part to an extended bank holiday for the Queen’s Platinum Jubilee, while July’s recovery was slightly behind forecasts due to lower electricity and gas consumption as the country sweltered in 40-degree heat.

The 75 basis points rate hike expected from the US Federal Reserve on 21 September now looks more of a certainty.

Focus on Bank of England and US Federal Reserve

o paraphrase US senator Robert Kennedy, we live in interesting times whether we like it or not.

T

With a change of monarch, a change of prime minister, an energy crisis, a weakening economy and rising interest rates, they are also uncertain times.

However, the news of a price guarantee and help for firms and households from the new administration may help.

The interest comes after a good set of 2022 results (to 31 March), in which GB grew adjusted operating profit by 2% to £58.8 million on revenue up 11% to £242 million. The company also anticipated a strong 2023, with profits anticipated up 22% to £72 million on revenue up a similar amount to £297 million.

The company added more than 500 clients in the fourth quarter bringing its full-year total to over 7,400, up 32%. It is also improving its ARR (annual recurring revenue) retention rate, from 103.1% to 105.5%. Growth came from all angles, with its biggest US market up 34% to $143 million, albeit with a $3.8 million revenue recognition adjustment.

‘Therebefore.isprecedence for a high-20 times offer,’ said Megabuyte’s Indraneel Arampatta, who pointed to compliance software supplier Ideagen (IDEA:AIM), which is currently being courted by Hg at around 28.7-times EV/EBITDA.

Interestingly,since.

I

Darktrace (%) 2021Oct 2022Jan Apr JulChart:0−50 Shares magazine • Source: Refinitiv

Conversely, private equity firm Thoma Bravo has walked away from a deal for cybersecurity firm Darktrace (DARK), sending its stock plunging.

dentity data intelligence platform provider GB Group (GBG:AIM) has become the latest UK technology company to catch the eye of potential buyers after confirming talks with Chicago-based private equity firm GTCR.

Analysts at Peel Hunt believe a trade buyer from the credit agency industry could easily emerge to up the ante. This could include the UK’s Experian (EXPN) or TransUnion (TRU:NYSE) of the US. [SF]

Analysts at Megabuyte calculate GB’s EV/EBITDA (enterprise value to earnings before interest, tax, depreciation and amortisation) at around 22 times once the news broke, versus about 17.5 times

No financials details have been disclosed so far although we do know that the discussions surround a possible cash offer. GB’s shares rallied hard as the news hit the screens of investors, sending the stock up from 435p to 647p.

profit of $1.46 million, versus the previous year’s $146 million loss. This was a strong performance driven by new customer wins that says a lot about demand for Darktrace’s artificial intelligence cybersecurity tools.

UK tech in the sights of private equity again as GB targeted

NEWS 15 September 2022 | SHARES | 7

Investor buying had sent Darktrace stock surging from 377p to 540p when talks investigating a deal to take the firm private where revealed last month. Yet those gains were washed away after Thoma Bravo ended talks. Darktrace shares fell 32% to 350p, although the price has edged up to 388p

Back to GB, and analysts believe an offer would have to come in above 700p if it is to have any chance of turning heads at board and shareholder level.

Interest may lure industry peers into rival offer for identity and anti-fraud specialist as Darktrace suitor walks

the Darktrace news was announced alongside full year to 30 June 2022 figures that saw the company chalk-up its first ever annual net

Shares readers may recall a similar trust – Global Sustainable Farmland Income – was slated to launch in early 2020 but failed to generate enough interest, so it will be interesting to see if the market is more receptive this time.

Farmland makes a comeback and assisted living sector to expand

The US company behind the trust, Intl Farming Investment Management LLC (IFC), has more than $2.2 billion of group assets under management and a track record dating back to 2009.

a net initial yield of 4.5% with an NAV (net asset value) target return of between 7% and 9% based on the 100p issue price and a management fee of 1% per year.

NEWS 8 | SHARES | 15 September 2022

Helpfully for investors there are already a couple of trusts against which to compare this new arrival in the form of Home REIT (HOME) and Impact Healthcare REIT (IHR), which cater respectively for homeless people and those with long-term physical and mental care issues. [IC]

Atrato Partners, the firm behind Atrato Onsite Energy (ROOF) and Supermarket Income REIT (SUPR), is acting as investment adviser to the trust, which is targeting an initial annual dividend of 5p per share and an NAV total return of between 7% and 10% per year.

First up is The Sustainable Farmland Trust which aims to raise £200 million to invest in US agricultural assets.

T

here was interest this week in two new investments trusts coming to market, each promising an inflation linkage aimed at offsetting potentially higher costs and interest rates.

Two new forinvestmentalternativetrustspreparemainmarketlisting

The company is targeting three areas for investment: specialized supported housing for adults with learning difficulties, mental health issues or physical disabilities; extra care for adults aged 55 and over who need specialist care; and homeless accommodation.

The trust will invest at least half the money raised in ‘a performing and diverse portfolio of US farmland assets’ held in an existing private fund run by IFC as well as investing directly in farming, agricultural supply and infrastructure assets in the US.

The company claims farmland assets are historically negatively correlated with equity markets but positively correlated with higher inflation.Itistargeting

Rents are expected to be funded by the Department for Work and Pensions with annual uncapped inflation-linked uplifts, while at the same time generating ‘material savings’ for UK taxpayers compared with the cost to the NHS of keeping patients in hospital.

The second new trust on the launchpad is Independent Living REIT, which is aiming to raise £150 million to invest in ‘supported housing assets which are let to compliant tenants’.

He has skewed the portfolio to the high-growth super-premium segment and insists ‘there has definitely been a newfound appreciation for conviviality since the Covid outbreak’.

RIGHT PLACE, RIGHT TIME

The firm’s drinks portfolio, covering all drinks occasions and price points and distributed across more than 160 markets, spans everything from Absolut Vodka and Ricard pastis, to Chivas Regal and The Glenlivet Scotch whiskies.

This is an attractive point of entry into a high quality, prodigiously cash generative company whose competitive advantages include a portfolio of prestigious brands and one of the best routes to market of any global spirits business.

We share Bank of America analyst Andrea Pistacchi’s view that Pernod Ricard offers exposure to ‘resilient earnings in the current environment, with its geographic diversification and portfolio which should be relatively protected from potential trading down’.

nvestors who’ve been richly rewarded by backing alcoholic drinks maker Diageo (DGE) should buy another large cap consumer defensive with tasty long-run growth prospects, namely its smaller spirits rival Pernod Ricard (RI:EPA)

Shares in the French drinks group are trading on a prospective price earnings ratio of 20.6 for the year to June 2023, falling to 18.9 for 2024 based on estimates from Berenberg, a not-to-be-missed discount relative to the firm’s own history, EU consumer staples and close peer Diageo.

(RI:EPA) €192.6

Other brands Pernod Ricard sells include Jameson Irish whiskey, Martell cognac, Havana Club rum, Beefeater gin and Perrier- Jouët champagne.

High-quality drinks pick Pernod Ricard sells at a tasty discount to peers

15 September 2022 | SHARES | 9

.

For the uninitiated, Pernod Ricard is the world’s number two wines and spirits producer and owns 17 of the top 100 spirits brands, yet like Diageo, still has significant scope for growth in a fragmented global drinks market.

Pernod Ricard is exposed to favourable consumer trends, with spirits taking a greater share in total beverage alcohol and the drinks market undergoing ‘premiumisation’, a trend which sees consumers drinking less but spending more on premium tipples.

PERNOD RICARD BUY

Market Cap: £42.9 billion

Euronext-listed and part of the CAC 40 and Eurostoxx 50 indices, Pernod Ricard, company strapline ‘Créateurs de Convivialité’, is stewarded by its thoughtful chairman and CEO Alexandre Ricard –the Ricard family has a 14.27% stake.

I

One of the most exciting aspects of the story is

The cash-generative spirits and wines seller is in an upgrade cycle and trades at an unwarranted discount to Diageo

PRESTIGIOUS PORTFOLIO

Regional organic sales growth in year to June 2022 % Growth by region WorldEuropeAsia-RoWAmericas 17%19%19%12% Chart: Shares magazine • Source: Pernod Ricard presentation STOCK

While Pernod Ricard’s finished the year with a 2.4 times leverage ratio, mainly the result of spending related to earlier acquisitions and last year’s €750 million share buyback, 2022 was a year of record high cash generation. In a show of confidence in its future prospects and cash generation, Pernod increased the dividend by 32% to €4.12 per share and announced a new

Crucially, Berenberg also believes that Pernod Ricard is in the early stages of an earnings upgrade cycle, ‘driven by management’s greater focus on operating leverage’.

the risks to consider are the potential for Pernod Ricard to overpay for acquisitions or significant increases in alcohol excise duties in lucrative markets such as the US, France, China, Spain and India, which could negatively affect the spirits producer’s tasty profit growth trajectory. [JC]

10 | SHARES | 15 September 2022

Berenberg, which has a €235 price target implying 22% upside, forecasts pre-tax profits growth from €2.8 billion to €3.2 billion this year, ahead of almost €3.5 billion in fiscal 2024. The broker likes Pernod Ricard’s exposure to super-premium spirits and its track record of selfhelp margin expansion and notes the company has one of the largest exposures to the recovery in global travel retail as international travel recovers.

Bumper gross margins above 60% suggest Pernod Ricard can cope with current inflation in input costs. In fact, Ricard and his team intend to deliver gross and operating margin expansion in the current financial year through a cocktail of cost efficiencies, further price increases and a positive sales mix, hopefully helped by a recovery in China and travel retail volumes in AmongAsia.

The £42.9 billion cap served up (1 September) forecast-beating results for the year to June 2022, with sales bubbling up 17% organically to a record €10.7 billion as Pernod Ricard distilled double-digit growth across all key regions, namely the Americas, Asia-Rest of World and Europe. The company delivered market share gains in most markets and flexed its pricing power muscles to achieve price increases across all markets, of ‘mid single digit on average’ according to Pernod Ricard.

€500 million to €750 million share buyback for the new financial year.

STIRRING UP GROWTH

Pernod Ricard 2021 8.83 6.16 3.12 2022 10.70 8.18 4.12 2023 (F) 11.70 9.36 4.65 2024 (F) 12.20 10.17 5.05 Year to June Net sales (€m) EPS DPS Table: Shares magazine • Source: Company data, Berenberg (€) (€)(€m)

that Pernod Ricard offers a play on a global legal drinking age population set to grow at a compound annual growth rate of 1.3% between 2020 and 2025, largely driven by emerging affluent middle classes in China andTheIndia.business is also embracing technology to ensure it remains relevant in the future, relying on its ‘Conviviality Platform’, a new growth model based on data and artificial intelligence, to meet the everchanging demands of consumers.

Bellevue Healthcare (p) 201720182019202020212022Chart:200100 Shares magazine • Source: Refinitiv

Dividends have grown in double digit percentages since launch. In 2021 the company paid 6.03p per share which represents a trailing yield of 3.4%.

A DIFFERENTIATED APPROACH

A great way to get exposure to companies driving change to tackle ageing populations and creaking healthcare systems

It is worth noting around 77% of the portfolio is invested in mid and small-cap companies which means the value of the trust swings around more than the benchmark. Approximately 95% of the portfolio is invested in the US compared with 73% for the benchmark.

The managers point out that during times of heightened uncertainty, investors often flock to the relative safety of mega-cap pharma which can harm short-term performance, given the trust’s relative underweight position in larger companies.

15 September 2022 | SHARES | 11

The managers start from the premise that the

The trust has an ongoing charge of 1.08% a year, slightly higher than other listed healthcare trusts, Polar Capital Global Healthcare (PCGH) (0.92%) and Worldwide Healthcare (WWH) (0.85%). [MGam]

T

he Bellevue Healthcare Trust (BBH) has built an enviable track record since launching in 2016. Shares believes the 5.6% discount to NAV (net asset value) presents investors with an attractive entry point.

Portfolio managers Paul Major and Brett Drake have more than two decades of healthcare experience each.

BUY (BBH) Market177.4pCap:£1.04 billion Discount to NAV 5.6% STOCK

Western healthcare systems are not fit for purpose. They argue the systems are very costly to run, wasteful and therefore unsustainable.

Historically the healthcare sector has provided relative defensiveness and perhaps surprisingly, good protection against rising prices.

HEALTHCAREBELLEVUE TRUST

Grab a slice of top performing Bellevue Healthcare Trust at a discount to NAV

The strategy addresses all stages of patient interactions and costs within the healthcare system focusing on investments aimed at providing solutions to the cost challenge. Some of the key themes include greater integration of technology, innovation in therapeutics and novel treatments, increased diagnostic personalization, population genomics and shifting payment models.

The trust is managed by Bellevue Asset Management, part of Swiss investment manager the Bellevue Group.

The trust has delivered three-and five-year total returns in NAV of 70.3% and 91.8% respectively, comfortably beating its benchmark (MSCI World Healthcare) returns of 48.6% and 71.2%.

Within these themes the managers undertake bottom-up fundamental analysis to isolate the most promising stock candidates. The team construct a high conviction, concentrated portfolio currently consisting of 29 names selected for their three-to-five-year return potential. Portfolio turnover is low.

AGT’sall.

Once an investment has been made, we seek to establish a good relationship and actively engage with the managers, board directors and, often, families behind the company. Our aim is to be a constructive, stable partner and to bring our expertise – garnered over three decades of investing in asset-backed companies–for the benefit of

A unique proposition for global equity investing

AVI has a well-defined, robust investment philosophy in place to guide investment decisions. An emphasis is placed on three key factors: (1) companies with attractive assets, where there is potential for growth in value over

Asset Value Investors (AVI) has managed the c.£1.3* bn AVI Global Trust since 1985. The strategy over that period has been to buy quality companies held through unconventional structures and trading at a discount; the strategy is global in scope and we believe that attractive risk-adjusted returns can be earned through detailed research with a long-term mind-set.

long-term track record bears witness to the success of this approach, with a NAV total return well in excess of its benchmark. We believe that this strategy remains as appealing as ever, and continue to find plenty of exciting opportunities in which to deploy the trust’s capital.

time; (2) a sum-of-the-parts discount to a fair net asset value; and (3) an identifiable catalyst for value realisation. A concentrated core portfolio of c. 26± investments allows for detailed, in-depth research which forms the cornerstone of our active approach.

The companies we invest in include family-controlled holding companies, property companies, closed-end funds and, most recently, cash-rich Japanese companies. The approach is benchmark-agnostic, with no preference for a particular geography or sector.

Value with a difference

Past performance should not be seen as an indication of future performance. The value of your investment may go down as well as up and you may not get back the full amount invested. Issued by Asset Value Investors Ltd who are authorised and regulated by the Financial Conduct Authority. *As at 31 January 2022 ±As at 31 January 2022, holdings >1% of NAV Discover AGT at www.aviglobal.co.uk @AVIGlobalTrust AVIGlobalTrust

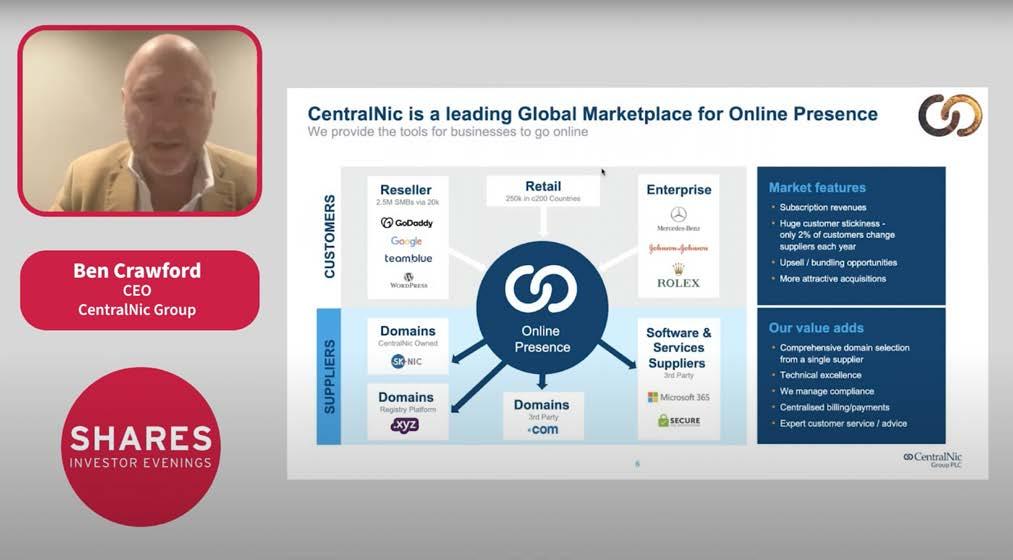

Small cap internet expert CentralNic (CNIC:AIM) continues to stubbornly frustrate shareholders even in the face of continued rapid growth.

If we take Berenberg’s expected 2022 forecasts at face value, it implies that revenues will have almost tripled in two years to roughly $600 million while adjusted EBITDA (earnings before interest, tax, depreciation and amortisation) will have gone from $29 million to $70 million.

WHAT SHOULD INVESTORS DO NEXT?

In recent first-half results (30 Aug) CentralNic reported revenues up 93% to $335 million, 62% of that growth organic. This was propelled by Online Marketing, which grew 167% (98% organically) to $258 million. Its domain names business was basically flat at $76.8 million, demonstrating management’s eye for developing the business as opportunities and markets change.

Net debt at the end of this year is estimated at $52 million, so the balance sheet is far from extended. This would surely change the market’s view of the company, reducing the stream of adjustments to earnings and delivering the re-rating the share price seemingly deserves.[SF]

Why CentralNic should end constant share placings to fund M&A

WHAT’S HAPPENED SINCE WE SAID TO BUY?

Since November 2021, when we originally said to buy the stock, the share price has plunged 18.5%. Obviously, the market’s shift away from growth as inflation soars has hurt the investment case, yet the financial performance continues to race ahead.

Since shifting focus from domain name management to online marketing services the company has produced a series of guidance hikes and rampant growth metrics that promise to catapult revenues and profits to new records this year. Yet the stock remains as ignored by the wider market as ever.

15 September 2022 | SHARES | 13

Presumably, the market’s reluctance to give CentralNic credit is due to its constant use of equity issues to fund acquisitions. This has capped earnings per share (EPS) growth to 57% in two years versus 141% EBITDA growth over the same timeframe. With a forecast $51 million of free cash flow anticipated this year, according to Berenberg, perhaps management needs to stop issuing new shares and start funding M&A from existing resources.

CENTRALNIC (CNIC:AIM) 116.5P Loss to date: 18.5% Sea of earnings adjustments from acquisitions has held back the share price

CentralNic Group PLC (p) 2020 2021 202210050Chart: Shares magazine • Source: FE Analytics

14 | SHARES | 15 September 2022

Earnings expectations have been cut and investors have priced in a recession already, which means bargain hunters may take the view retailers are now oversold, particularly as prime minister Liz Truss’ energy price guarantee will put some cash back in the pockets of hard-pressed consumers.

Companies which can ride out the storm

By James Crux Funds and Investment Trusts Editor

T

he retail sector has had a dire 2022, heavily sold off on fears earnings will disappoint as households curb spending due to rising UK inflation and the energy price crisis.

be left with battered finances and diminished prospects, if they make it through the crisis at all.

RETAIL SURVIVORSRETAIL SURVIVORS

CONSUMER CRUNCH

Given this challenging backdrop, investors need to be highly selective when it comes to retailers and focus solely on those with strong competitive positions and fortress balance sheets. Retailers that survive the crisis should emerge with enhanced market share opportunities as competitors will have fallen by the wayside, while the losers will

Though the consumer has held up well so far, supported by pandemic savings in many cases, soaring utility bills will leave less discretionary income for shoppers to spend on goods and services, a nightmare for retailers already struggling with cost Consumerinflation.confidence has fallen to historically low levels, with GfK’s long-running Consumer Confidence index decreasing three points in August to -44, the lowest since records began in 1974.

According to the ASDA Income Tracker, UK discretionary income saw a 16.5% contraction in July. As measured by the BRC-KPMG Retail Sales Monitor, UK retail sales were marginally ahead year-on-year in August, up 1% versus a robust 3% comparative, but this performance was boosted by clement weather, notably around the Bank Holiday, and as Shore Capital suggests, was ‘perhaps a calm

Other retailers targeting lower income consumers include B&M European Value Retail (BME), the variety discounter in a very favourable space given the squeeze on consumers’ finances.

warning (8 September) pinned on margin pressure at Primark, having to absorb rising costs caused by surging energy prices and a strengthening US dollar.

Also famed for its value proposition is Sports Direct, the sportswear chain at the heart of Mike Ashley’s retail conglomerate Frasers (FRAS). Sports Direct controls the value end of the UK sporting goods market and through Flannels, Frasers has

Little wonder then that shares in high street bellwether Marks & Spencer (MKS) have declined 50% year-to-date at the time of writing, with fashion seller Next (NXT) and home improvement giant Kingfisher (KGF) both down by around 30%; tellingly, Kingfisher is among London’s top five most shorted stocks along with online fast-fashion retailers Boohoo (BOO:AIM) and ASOS (ASC) according to Shorttracker.co.uk.

Led by experienced retailer Simon Wolson, Next looks better positioned than many other sector peers due to its strong balance sheet, robust cash flows and high margins, which shold provide a cushion in the tough times ahead.

survival looks assured given the strong balance sheet run by Associated British Foods and the company’s conglomerate structure which sees it derives revenue from food processing.

before an energy hit autumn storm’.

The retailer has also decided not to push prices too far to help maintain its value credentials for its customers. Short-term pressures notwithstanding, Primark should benefit as shoppers trade down from more expensive retailers, though we concede its core customer demographic is really feeling thePrimark’spinch.

As Zeus Capital points out, Shoe Zone’s attractive value proposition means it is ‘well placed to win market share as consumers seek more affordable alternatives against the current backdrop of high energy costs and food price inflation’.

B&M©

The cost of living crisis is driving demand for great value products, which should play to the strength of discount retailer Primark, the hawker of cheap fashion that was one of the few retailers to maintain positive like-for-like sales during the financialHowever,crisis.shares in parent Associated British Foods (ABF) plunged to multi-year lows on a profit

Consumers are having to fork out more for essentials such as energy, transport and food, with the under-30s age group impacted the most by rampant inflation, which means they are having to cut back on non-essential items such as clothing and DIY products. Juryoutis

LIKELY SURVIVORS

Vulnerable Source: Shares magazine

The shares are down sharply year-to-date as B&M has found it difficult to fully pass through cost inflation and consumer behaviour has proved unpredictable, while analysts have expressed concerns over inventory levels and B&M’s loss of price food leadership.

Who looks safe and who’s in the danger zone? Next Marks Spencer& ASOS Shoe Zone B&M Boohoo Frasers Primark Kingfisher WH Smith Halfords Currys JDFashionSports AO World DFSMade.comFurniture Survivor

Bucking the sector-wide de-rating is Shoe Zone (SHOE:AIM), the discount shoes, slippers and boots seller which recently (31 August) delivered its third earnings upgrade in as many months off the back of strong August trading driven by bumper demand for summer and ‘back to school’ products and ongoing margin improvements resulting from good supply chain and cost management.

15 September 2022 | SHARES | 15

16 | SHARES | 15 September 2022

JD A STEP AHEAD

Books, stationery and snacks seller WH Smith (SMWH) continues to exhibit resilience, generating cash by running its legacy high street stores business as efficiently as possible while investing in its international travel business as the growth engine of the group. The fact travel sales are now above pre-pandemic levels is very encouraging.

Also proving its robustness is car parts-to-bicycles seller and autocentres operator Halfords (HFD), which reported (7 September) resilient trading over the 20 weeks to 19 August 2022 and maintained full year profit guidance in the £65 million to £75 million range. Over 70% of Halfords’ sales now come from motoring products and services, an area of spend that tends to be more needs-based rather than discretionary. Buying a new bike is unlikely to be a priority for cash-strapped households, but Halfords can afford to lean on the motoring business and wait for the next upswing in demand.

The needs-based nature of greetings cards, which people purchase for annual and everyday events, makes this a resilient space too. Step forwards Card Factory (CARD), the value cards and gifts retailer which has scope to raise prices while still leaving its products cheaper than rivals.

RETAILERS UNDER FINANCIAL PRESSURE

Thecomfort.presence of leaseholds on the balance sheet probably doesn’t help the scores of other names on the list, though there may be particular concern about sofa seller ScS (SCS) given it sells the kind of big-ticket items which hard-pressed consumers are likely to think twice about buying in the current climate. [TS]

a leading position in UK luxury – two areas that should prove robust.

The finances of the retail sector already bear the scars of a period when they were effectively unable to trade normally due to Covid

The table shows companies with an Altman Z-score of less than 1.8 according to data from Stockopedia. The Z-score was developed by Edward Altman, an assistant professor of finance at New York University, in the late 1960s. It looks to analyse a balance sheet to identify the risk of bankruptcy and a score below 1.8 indicates a high probability of financial distress within twoEyebrowsyears. may be raised by the presence of WH Smith on the list. While it is carrying significant debt, both as a result of the pandemic and thanks to acquisitions aimed at growing its travel division, its scale and track record plus the fact a significant chunk of its liabilities relate to leases on its shops provide some

Thisrestrictions.meansmany retailers could find it harder to weather the current consumer storm caused by the cost-of-living crisis.

Retailers under financial pressure The Works 0.95 Card Factory 1.02 Superdry 1.05 Moonpig 1.43 WH Smith 1.47 Currys 1.62 SCS 1.70 Company Altman Z-Score trailing 12-months Table: Shares magazine Source: Stockopedia, data as at 8 September 2022

Another name in negative share price territory this year is athleisure leader JD Sports Fashion (JD). Given its focus on the youthful demographic, the market evidently thinks the ‘King of Trainers’ could struggle as consumer incomes are squeezed. Yet JD Sports is an international business with strong relationships with Nike and Adidas, while its net cash balance sheet leaves it well-placed to survive the crisis. As Shore Capital argues, ‘JD’s differentiated offer allows the retailer to distance itself from the highly promotional environment’.

The outlook for digital fashion retailers ASOS and Boohoo is gloomy given their online-only businesses models generate skinny margins and they sell to a younger customer cohort being hammered by the cost-of-living squeeze.

pandemic and it has comfortable financial headroom, we would be wary of the potential for near-term downgrades here, as hardpressed shoppers can always defer the purchase of Superdry’s premium clothing, accessories and footwear.

KEY PICK – NEXT (NXT)

This is allowing the retail giant to offer more products on its website which makes it more attractive to customers, and it also earns a fee from clients for handling their e-commerce needs. Cash generation remains a key plank of the investment case, with the retailer returning cash to shareholders through earnings enhancing share buybacks.

DFS©

Admittedly, the Simon Wolfson-led clothing and homewares chain isn’t immune to the headwinds facing UK retailers, but Next is better at managing them than most and is delivering robust sales in physical stores and a resilient showing online. Long-term growth prospects for the business look better than they have done for some time, as less durable rivals like Topshop and Debenhams have disappeared from the high street, enabling Next to gobble up market share.

Retailers without a distinctive proposition or with fragile business models or weak balance sheets are in for trouble. Marks and Spencer’s clothing and home business lacks the value credentials of a Primark, while its margins are lower than those of Next, suggesting it might be less resilient in a downturn, though it has come through periods of pain in the past.

One of the retail sector’s biggest casualties is ‘British lifestyle group’ Joules (JOUL:AIM), the wellies-to-outwear purveyor whose shares have plunged following a string of profit warnings that have pressured the balance sheet, though they did rally on news Next was poised to inject some cash by taking a strategic minority stake – ‘positive discussions’ continue.

£57.66

LIGHTS FLASHING RED

Next©

With consumers avoiding big-ticket purchases, expect furniture sellers DFS Furniture (DFS) and beleaguered Made.com (MADE) to find things tough. An emergency fundraising might be on the cards at online furniture purveyor and initial public offering (IPO) flop Made.com as rising essentials inflation squeezes household spending. Investors should also be mindful that consumers stocked up on laptops and new TVs during lockdowns, so Currys (CURY) and AO World (AO.) will struggle to grow sales in the months ahead.

Shares in Next have plunged from their September 2021 peak, but only the brave would bet against the best-in-class retailer’s equity reclaiming those highs on a medium-to-long term view.

The pandemic-inflated home improvement boom is also fading, bad news for B&Q-owner Kingfisher and Wickes (WIX), as well as other discretionary retailers including Topps Tiles (TPT) and even sector star turn Dunelm (DNLM), though the UK homewares leader’s keenly priced-yetquality home furnishings will resonate with price sensitive shoppers and Dunelm has successfully navigated past periods of consumer uncertainty.

15 September 2022 | SHARES | 17

There is also growing excitement over the potential of the ‘Total Platform’, which sees Next leveraging the expertise, infrastructure and software it has developed for its own online business to provide an e-commerce outsourcing service for third party brands.

Though CEO Julian Dunkerton has steered apparel retailer Superdry (SDRY) through the

Time to rethink – real estate securities unlock ‘alternative’ property

Views and opinions expressed by individual authors do not necessarily represent those of Columbia Threadneedle TheInvestments.valueofinvestments and any income derived from them can go down as well as up as a result of market or currency movements and investors may not get back the original amount invested.

We are long-term proponents of the merits of accessing property via listed real estate, either solely or in combination with select physical assets. It’s an approach that allows us to sidestep the challenges facing more traditionally structured portfolios and harness opportunities that lie beyond their reach.

ADVERTISING PROMOTION

Risk Disclaimer

It’s also important to consider how opportunities vary by location. The UK is further along the online retail road than continental Europe so you may want to avoid UK shopping centres, but affordable rents and higher footfall mean their European counterparts remain selectively attractive.

UK high streets are under pressure but there’s growth in well-located retail parks and premium discount outlets. Convenience and ‘click & collect’ shopping are in vogue and as we buy more online there’s a boom for last mile delivery and urban warehousing property assets. Logistics has been an obvious beneficiary and although we’ve seen yield

compression there remain opportunities in land rich quality businesses both in the UK and Europe.

Retail – selective thinking

Property portfolios & the benefits of alternative thinking TR Property Investment Trust

Keep property in the mix

Avoiding the high street and old office space sounds simple but legacy real assets can be a challenge to exit. Liquidity, however, becomes a minor issue when investing in property via listed real estate through a universe like the FTSE EPRA/ NAREIT Developed Europe Index. Here it is possible to tap into a fast-evolving and geographically diverse opportunity set rich in ‘alternative’ sub-sectors.

Elsewhere, sectors like healthcare, social housing, selfstorage, and student accommodation look interesting. The former is a diverse sector, so it pays to be selective.

Perspectives on healthcare

Just now, we place an emphasis on premises utilised by primary healthcare providers like the NHS but are cautious on nursing homes where margins look relatively thin. Of course, we’re not the only ones with a positive take on these areas so we use market volatility to build positions when the price is right.

it makes sense to consider alternative approaches to the traditional property model.

The value of directly-held property reflects the opinion of valuers and is reviewed periodically. These assets can also be illiquid and significant or persistent redemptions may require the manager to sell properties at a lower market value adversely affecting the value of your investment.

Against the backdrop of structural and regulatory change

There are several trends at play – some posing challenge, others opportunity. The pandemic accelerated themes like the transition to online retail and re-examination of office space suitable for the ‘hybrid’ working model just two examples. Traditional bricks & mortar portfolios can find themselves on the wrong side of these shifts.

Traditional portfolios – causes for concern

Past performance should not be seen as an indication of future performance. The value of investments and income derived from them can go down as well as up as a result of market or currency movements and investors may not get back the original amount invested.

less globalised economy, the Russian invasion of Ukraine and the supply chain disruptions caused by Covid, (particularly in China), have caused a surge in inflation.

What would interest rates at 4% mean for investing in stocks?

A BIG CHANGE FOR INVESTORS

Rising rates will benefit value stocks and those with pricing power

government bonds is sometimes used as the socalled ‘risk-free rate’.

An inflationary and rising interest rate environment will tend to increase the appeal of value stocks relative to growth stocks. This is because during a period of rising interest rates current earnings become more highly valued while investors are less willing to pay up for cash at some point in the Businessesfuture.withpricing power (the ability to increase price without experiencing a loss in demand) are also likely to prosper in the current

A

UK inflation is running at the fastest pace in 40 years, rising from 9.4% to 10.1% in July. This marks a continued structural shift in the cost of goods and services that is squeezing discretionary spending. This is important because consumption constitutes the largest constituent (over 60%) of the UK economy, and as it slows so will the UKAteconomy.thesame time central banks have been forced to raise interest rates in an attempt to tame inflation. Money markets, which see trading in very short-term debt, suggest that interest rates will hit 4% by next spring.

This has significant implications for investors. First, the interest rate you receive on a savings account will rise. This along with the yield from long-term

The flip side of this is that the additional return that investors will require for holding shares as opposed to the return they would receive on a savings account (the equity risk premium) will also beThishigher.islikely to make investors more cautious about investing in stocks and increases the appeal of holding cash. However, over the long term shares as an asset class have proven to outperform bonds and the return derived from cash.

FEATURE 15 September 2022 | SHARES | 19

DASH FOR CASH

For a one-year fixed rate UK savings account rates range from 3% to 3.35%. Easy access rates are in the 1.7% to 1.8% range. These rates look increasingly likely to rise in the coming months.

As a result, they will typically also trade at lower price to earnings or PE multiples. The PE ratio is the share price divided by earnings per share.

THE INCREASING APPEAL OF VALUE STOCKS

environment. Rising costs can erode a company’s profit margins, and ultimately investor returns. Pricing power can help companies fight inflation and protect their margins by passing costs along to the customer.

Critically stocks in the cheapest 30% of the market by price to book ratio (also known as price to net asset value) outperformed the most expensive 30% by 9.97 percentage points per year

Secure Trust Bank

investors, holding cash no longer detracts from a portfolio’s yield.

Ken French is a professor of finance at the Tuck School of Business, Dartmouth College. He is most famous for his work on asset pricing with EugeneAnalysisFama.based on data from French’s own Data Library suggests that value stocks perform well when interest rates and inflation are high.

This view was cogently articulated from a US perspective in a recent research note by the Morgan Stanley strategy team.

Their key finding was that except for two years (2013 and 2018), US dollar cash underperformed both the S&P 500 and the US 10-year Treasury bond every year from 2010 to 2020. Morgan Stanley strategy believe that we are experiencing a regime switch arguing that for US dollar

Value stocks are those which trade at a lower level than their fundamentals (the underlying economic conditions, the state of the wider sector and their own financial performance) suggest they should.

Proivder Rate (AER variable)

FEATURE 20 | SHARES | 15 September 2022

1.81%

1.80%

According to Barclays’ annual Equity Gilt Study, UK share returns have averaged 4.9% a year after tax and inflation since 1900 – compared with 1.3% from UK government bonds and 0.6% from cash.

Shares magazine •

Money Saving Expert,

Table: Shares magazine • Source: Money Saving Expert 9 September 2022 fixed savings

September 2022

rates United Trust Bank 3.35% Virgin Money 3.32% Tandem 3.30% Provider Rate (AER variable)

Shawbrook Bank

Best easy access savings rates

Best one-year

Table: Source: 9

And yet over time, history would suggest it makes sense to hold stocks.

US six-month treasury bills are currently yielding 3.1%, which is the highest level since late 2007. While the current interest rate returns in the UK are lower than in the US, they still signify a significant shift in the appeal of cash as an asset class.

Zopa 1.81%

Given the increasingly bearish macro-economic backdrop the appeal of cash versus other asset classes including bonds, stocks and gold is likely to rise. In recent decades holding cash has been perceived as being overly defensive and the paltry returns on offer were outpaced by inflation, even when inflationary pressures were much less acute than they are now.

Businesses with pricing power (the ability to increase price without experiencing a loss in demand) are likely to prosper in the currentTobaccoenvironment.giant

• In an inflationary and rising interest rate environment current earnings become more valuable and future earnings tend to become less valuable.

between January 1970 and December 1979, a period marked by persistently high inflation.

FEATURE 15 September 2022 | SHARES | 21

During periods of low interest rates, there is often a flow of capital to companies that have good potential for growth, implying that investors are willing to pay a higher premium for the future growth of such companies.

Given the highly challenging macro-economic backdrop investors may increasingly appreciate BAT’s defensive traits as people find it hard to shake the smoking habit irrespective of their economic situation. It is highly cash generative and pays a 6.2% dividend yield.

In non-technical terms this means a 10% increase in price would lead to a 4% to 6% drop off in Theconsumption.strengthofthe cigarette business is built on the group having strong global brands at every price point British American has led the US market on price over the last two years with eight price increases with no change in demand.

• Inflationary periods have favoured value stocks and deflationary periods have favoured growth stocks.

The critical point of distinction is that value orientated companies are valued on their nearterm cash flow (current earnings) and are impacted less from any increase in interest rates. This is in sharp contrast to growth-orientated corporates where the majority of their value comes from long-term cash flows.

THE IMPORTANCE OF PRICING POWER

Tobacco is addictive which makes it difficult for people toBritishquit American Tobacco is a good example of a company with pricing power

British American Tobacco (BATS) is a good example of a company with pricing power, though there are obvious regulatory and ethical considerations to factor in.

An upward movement in interest rates changes the market’s assessment of what a future stream of cash flow or earnings is worth today.

Tobacco is addictive which makes it difficult for people to quit. The tobacco industry also operates in a highly consolidated market with the four largest companies controlling more than 80% of the market value.

By Mark Gardner Senior Reporter

THREE FORCES DRIVING THE ROTATION FROM GROWTH TO VALUE

A growth stock refers to a company that’s expected to increase its profits or revenue faster than the average business in its industry or the market broadly. Growth stocks are typically in demand when interest rates are low or falling.

A 10% increase in price would lead to a 4% to 6% drop off in consumption

Given the strong position of its global brands British American Tobacco has been able to continually improve the price mix. Finance director Tadeu Marroco told Shares in 2021 that the elasticity of cigarettes across the world was still very benign at 0.4 to 0.6.

• Typically value stocks are assessed on their current earnings while growth stocks are valued on their future earnings.

Cash rates are improving: what you need to

nless you have been living in a particularly well-fortified and soundproof bunker, you will have noticed that UK interest rates are rising quite rapidly, as the Bank of England does its level best to combat spiralling inflation.

While that’s not good news for anyone with high levels of borrowing, including mortgage debt, there is a silver lining for cash savers, who are now seeing significantly higher interest rates on offer.

PERSONAL FINANCE 22 | SHARES | 15 September 2022

The rising tide of interest rates is not lifting all boats to the same extent though, and savers usually need to look beyond high street banks and building societies to find the best offers.

As well as return on their capital, savers are wary

You may be able to get more from the high street banks if you fulfil certain conditions in terms of being a premium customer, or making limited withdrawals or regular deposits, but generally speaking, the standard flexible accounts offered by these providers are not very competitive.

know High street bank savings rates versus best-buy Barclays Everyday Saver 0.15% Lloyds Club Lloyds Saver 0.20% NatWest Everday Saver 0.20% Nationwide Instant Access Saver 0.25% HSBC Flexible Saver 0.40% Moneyfacts best rate Al Rayan Bank Everyday Saver 2.10% Bank Account Interest on £10,000 lump sum Table: Shares magazine • Source: Relevant bank websites, Moneyfacts, as of 8 September 2022

this is

Key things to consider if you want to stash money

of return of their capital, which is why many of them probably stick with well-known high street names. That’s understandable, but in fact, provided the bank account you choose is covered by the Financial Services Compensation Scheme – also known as the FSCS – you will receive up to £85,000 of your money back, even in the unlikely event in

The table shows a selection of typical instant access savings accounts from the high street compared to the best currently available on the market, according to Moneyfacts.

U

a savings account

One nasty little shock which savers might once again find themselves experiencing is paying tax on their cash interest.

Given the huge shift we’re seeing in interest rate policy, all this is liable to frequent change, so savers would do well to keep an occasional eye on the savings market.

By Laith Khalaf AJ Bell Head of Investment Analysis

CASH SUPERMARKETS

While interest rates are heading in the right direction for savers, it’s entirely fair to point out that against a backdrop of double-digit inflation, your money is still going backwards in real terms.

One way to deal with this is to invest money you might not need in the next five to 10 years, or longer, in the market. In the short term the stock market can be extremely capricious, but it’s surprisingly reliable over longer time periods, and one of the best ways to guard your money against the ravages of inflation.

It’s important to note the FSCS treats all banks sharing the same banking license as one entity, and therefore only eligible for one £85,000 compensation payment per customer as a maximum. For instance, HSBC and First Direct are treated as one entity, because they are part of the same banking group, even though they operate under separate brands.

Another puzzler for savers to chew over is whether they may want to lock up some of their money for a set period in fixed-term bond accounts, to get a better interest rate.

HIGHER RATES IF YOU LOCK UP FOR LONGER

WATCH OUT FOR TAX

That tax-free allowance is £1,000 of interest for basic rate taxpayers, £500 for higher rate taxpayers, and zero for additional rate taxpayers.

that your bank goes bust and your money is lost. However, holding more than this with one bank clearly comes with some risk attached.

As interest rates rise, savers might well find themselves breaching these limits, especially those with larger cash piles. A cash ISA can help here, because all interest from these accounts is taxfree. However, the rates on offer are often a bit lower than non-ISA accounts, so savers might need to indulge in a bit of maths to calculate if they’re better off saving in a cash ISA or not.

DISCLAIMER: AJ Bell owns Shares magazine. Editor Daniel Coatsworth owns shares in AJ Bell

PERSONAL FINANCE 15 September 2022 | SHARES | 23

In theory, while interest rates are rising this shouldn’t be such a good idea, but one-year bond rates are now looking relatively attractive and seem to have already priced in some of the interest rate hikes to Accordingcome.to Moneyfacts, the best one-year fixed bond account is currently offering a rate of 3.35%, compared to a top rate of 2.1% for instant access savings. That looks like a reasonable trade for locking up at least some of your money for 12Youmonths.currently don’t get a huge amount more interest for locking away for longer. The best rate on both a three-year fix and a five-year fix is 3.6%, and there is a greater risk that interest rates rise further over these longer time periods, which you would miss out on if your money is tied up.

In some ways, this is a nice problem to have, because for many years interest rates have been so low that for most people, the annual tax-free savings allowance has more than covered the income they’ve received from cash in the bank.

They might find a useful way to do this is to use one of the new cash supermarkets, such as Raisin or the AJ Bell Cash Savings Hub. These cash marketplaces have competitive accounts available from lots of different banks, making it easier to compare providers, and switch between them, which can be done within the cash supermarket account.

• Chinese markets have been weighed down by geopolitics, the government’s Covid strategy and weakening economic growth.

It has been taken as the heavy hand of an all-powerful government, stifling innovation and business growth. However, we think in many cases, the Chinese government is only doing what other countries are trying to do – curb the social harms associated with internet usage and address privacy concerns. The risk appears to have passed with the government refocusing on growth.

However, that is not to say that we can ignore these problems completely on the abrdn China trust. We have focused our portfolio on a number of long-term themes. These themes remain largely unaffected by shifts in government policy, geopolitical tensions or the short-term impact of Zero Covid, but we have made tweaks to the portfolio to reflect the current situation.

• The recent falls in the Chinese market look extreme.

This backdrop goes some way to explaining the volatility in the Chinese market this year. However, we believe ultimately the gap between operational and share price performance will become too big to ignore. This should start to rectify as companies report their results. This has already started to be seen in the very short-term.

The first of these themes is the development of the domestic consumer economy. This has been an explicit goal of the Chinese government as it strives to move away from manufacturing-led

ADVERTISING FEATURE

China: time to look again?

Views on China often polarise, but the reality is nuanced. On the zero Covid policy, the narrative has been that China’s dogmatic enforcement of lockdowns threatens economic growth. In reality, China doesn’t yet have the vaccine coverage or healthcare infrastructure to support a ‘living with Covid’ policy. However, it is putting this in place, with new treatments and an mRNA vaccine emerging. As such, the situation is difficult, but we believe it does not threaten growth over the long term. Similarly, investors have been deterred by the Chinese government’s crackdown on certain industries – including the internet giants and education providers.

Adapting the portfolio

By Nicholas Yeo, Investment Manager, abrdn China Investment Company Limited

The final area of concern for investors has been over shifting geopolitical relationships. The US/China relationship has fractured in recent years and that conflict has been exacerbated by the Russia/Ukraine crisis, which has put the two countries on opposite sides. This will undoubtedly have consequences for China’s access to technology in future. The delisting of American Depository Receipts (ADRs) of Chinese firms from US stock exchanges has also been difficult, exerting downward pressure on share prices. However, this is unlikely to affect the long-term growth trajectory of China in a meaningful way.

For many investors, China represents a conundrum: on the one hand, it seems unwise to ignore the potential opportunities created by the world’s second largest economy, as 1.4 billion people grow wealthier. On the other, it has been a particularly difficult place to invest since the start of this year, weighed low by geopolitics, the government’s Covid strategy and weakening economic growth.

• The gap between operational and share price performance is becoming too big to ignore.

The value of tax benefits depends on individual circumstances and the favourable tax treatment for ISAs may not be maintained. If you are a basic rate tax payer and you do not anticipate any liability to Capital Gains Tax, you should consider if the advantages of an

• Emerging markets or less developed countries may face more political, economic or structural challenges than developed countries. This may mean your money is at greater risk.

• As with all stock exchange investments the value of the Trust shares purchased will immediately fall by the difference between the buying and selling prices, the bidoffer spread. If trading volumes fall, the bid-offer spread can widen.

• Specialist funds which invest in small markets or sectors of industry are likely to be more volatile than more diversified trusts.

Issued by Aberdeen Asset Managers Limited which is authorised and regulated by the Financial Conduct Authority in the United Kingdom. Registered Office: 10 Queen’s Terrace, Aberdeen AB10 1XL. Registered in Scotland No. 108419. An investment trust should be considered only as part of a balanced portfolio. Under no circumstances should this information be considered as an offer or solicitation to deal in Findinvestments.outmoreat

Other areas of focus in the portfolio include digitisation. There is widespread adoption of technology among China’s vast population, which has helped create opportunities across multiple sectors, including e-commerce and gaming, plus digital transformation and data centres. We have used share price weakness to add to certain areas. For example, we’ve been adding to semiconductors as valuations have dipped.

• Investing globally can bring additional returns and diversify risk. However, currency exchange rate fluctuations may have a positive or negative impact on the value of your investment.

ISA investment justify the additional management cost/ charges incurred.

Important Information

• Investment trusts are specialised investments and may not be appropriate for all investors.

• There is no guarantee that the market price of a Trust’s shares will fully reflect its underlying Net Asset Value.

•

• Investment trusts can borrow money in order to enhance investment returns. This is known as ‘gearing’ or ‘leverage’. However, the use of gearing can result in share prices being more volatile and subject to sudden or large falls in value. Where permitted an investment trust may invest in other investment trusts that utilise gearing which will exaggerate market movements, both up and down.

Other important information:

Growth areas

The portfolio also holds a number of financials, with growing demand for wealth management products a feature of rising wealth. This also brings some defensiveness to the trust at a time when

Risk factors you should consider prior to investing:

growth. Wages have risen significantly in recent years, with households becoming wealthier as a result. We have made shorter-term adaptations to the stocks we hold within this theme. While China is not facing the same inflationary pressures as Western economies, prices are still rising. Discretionary spending is likely to be weaker as households spend more on necessities. As such, within our consumer segment, we’ve shifted the portfolio to some more ‘staples’ rather than discretionary names. We believe these companies can continue to deliver against the current backdrop. The next generation of Chinese consumer tends to favour domestic rather than international brands, such as the spirit Moutai baijiu made by Kweichow Moutai. We also recognise that Covid will continue to create some disruption, with individual cities locked

• Past performance is not a guide to future results.

www.abrdnchina.co.uk or by registering for updates. You can also follow us on social media: Twitter and LinkedIn

there has been a notable rotation in Chinese markets from growth to value. Healthcare is another area of focus, as an emerging middle class demands improved care, particularly in the wake of the pandemic. The energy transition is another fertile source of opportunities. The Chinese markets have been buffeted by a series of problems. However, none of these challenges are likely to stall the long-term growth trajectory for the country. There are still real opportunities in the Chinese market, and signs that investors are starting to reexamine them after a difficult period.

• The value of investments and the income from them can go down as well as up and you may get back less than the amount invested.

down. As such, we’ve sought to prioritise those companies with warehouses across the nation, rather than those confined to a single region.

ADVERTISING FEATURE

Companies selected for illustrative purposes only to demonstrate the investment management style described herein and not as an investment recommendation or indication of future performance.

The main UK-listed shale player IGas Energy (IGAS:AIM) has switched its focus to conventional onshore oil and gas production. Its shares have performed very strongly in 2022 but last week fell as it responded to the removal of the fracking ban – with investors perhaps disappointed by a lack of detail on how the assets would be developed.

EMULATING THE US

There is also some good news for investment trusts in the renewable energy space

Up until now, very limited progress has been made on UK shale gas despite the big claims for itsConventionalpotential.

To put this in perspective UK natural gas consumption in 2021 totalled just 2.7 tcf. However, as the Cuadrilla episode illustrates, there are concerns about safety and fracking might not be popular in the communities which surround this prospective resource. This might make politicians’ newfound support for shale gas a bit shaky.

Truss plan for theindependenceenergyfiresupoilandgassector

here were two positive developments for the UK oil and gas sector as new prime minister Liz Truss announced her plan to address the UK energy crisis.

The process involves injecting high-pressure chemically treated water and sand to crack tight shale rock formations and release trapped oil and Frackinggas.operations have a significant footprint – sometimes encompassing as many as 15 large pumps covering an area as large as a football pitch and there is a requirement for a significant amount of water.

First, she confirmed she wouldn’t be using a windfall tax on energy producers to help pay for the planned freeze on bills. Second, she announced plans to cut up sector red tape, including an immediate lifting of the moratorium on fracking, as part of a bid to make Britain energy independent byThis2040.means the UK should be a net energy exporter rather than a net importer as has been since 2004. The 2040 target is instructive; these changes aren’t going to make a big difference in the short term as they will require long-term investment to bring to fruition.

T

What is fracking?

The UK is looking to emulate the US whose own energy independence has been achieved in large part due to its successful exploitation of shale gas.

offshore oil and gas may also get a boost from a new North Sea licensing round – with more than 100 licenses on offer. The UK’s offshore energy industry body OEUK noted in a 2022 report that exploration and appraisal activity has been at ‘record low levels in recent years’ with just five exploration wells drilled in 2021 – the lowest number since the beginnings of the North Sea as

Estimates from the British Geological Survey, published in 2013, indicate there could be more than 1,300 trillion cubic feet (tcf) of natural gas trapped within shale rock in the Bowland-Hodder basin which straddles north and central England.

The effective ban on fracking has been in place on safety grounds since 2019 when activity by private operator Cuadrilla caused stronger than expected tremors in Lancashire.

FEATURE 26 | SHARES | 15 September 2022

Performance2022todate(%)

An election is expected in 2024 and some current polls have the Labour Party, which made a strong case for a windfall tax on the sector’s so-called ‘excess profits’, enjoying a double-digit lead over the

Table: Shares magazine • Source: SharePad, data to 12 September 2022 market rate and still claim subsidies.

Serica Energy 66

Out to the end of this decade, OEUK has identified £26 billion worth of investment opportunities in the North Sea at various stages of progress. If they were all greenlit this would deliver four billion barrels of oil equivalent (boe) of oil and gas (37% gas and 63% oil) by 2030.

IOG −26

RENEWABLES RELIEF

FEATURE 15 September 2022 | SHARES | 27

Jersey Oil and Gas 78

an oil and gas province 60 years ago.

Energean 70

Where is the renewables space in all this? There was relief that its own profits would not be subject to a levy. Investment bank Stifel commented: ‘We recently said that the threat of a windfall tax was diminishing as Liz Truss had indicated she was not keen on the idea. However, the risk of the additional levy has been a cloud over the renewable funds and, while lower levels of inflation potentially means lower future uplifts to net asset values, this is good news overall for the sector, with the risk now ruled out.’

Company

Union Jack Oil 268

EnQuest 67

UK Oil & Gas Investments −15

Harbour Energy 43

Orcadian Energy 6

A further risk which may put energy companies off from making big long-term capital investment decisions is a change of government which could result in much less favourable fiscal and regulatory arrangements for the industry.

Egdon Resources 555

Europa Oil & Gas 107

IGas Energy 602

One lingering cloud hanging over renewables funds is a reported plan to make them agree new long-term contracts at fixed prices below current rates. Currently wind and solar farms built more than eight years ago can sell electricity at the

Kistos 42

Angus Energy 254

How UK oil and gas shares have fared in 2022

i3 Energy 93

Conservatives.By

Parkmead 48

However, only £8.5 billion of these potential developments has been sanctioned and if no further work were to be signed off then production would, according to OEUK, decline at an average rate of around 15% per year until 2030. It notes this would mean the UK would be left dependent on international imports for around 80% of its gas needs and around 70% of its oil requirements.

Tom Sieber Deputy Editor

Parliament’s Climate Change Committee estimates consumption of eight billion boe during this time frame. Therefore, net imports would still represent 50% of consumption.

Hurricane Energy 108

SHARPEN YOUR INVESTING SKILLS WITH A SUBSCRIPTION TO SHARES HELPS YOU TO: • Learn how the markets work • Discover our best investment ideas • Monitor stocks with our customisable watchlists • Enjoy our guides to sectors and themes • Get the inside track on company strategies • Find out how fund managers make money Digital magazine Online toolkit Investment ideas

Martin Gamble Education Editor

During the last big economic downturn in 2008 Somero’s revenue dropped sharply, from $66.4 million to $22 million while profits turned into losses. Construction firms were particularly hard hit during the banking crisis.

historically.By

Could there be factors not yet visible which explain the low rating of the shares or is more patience

FEATURE 15 September 2022 | SHARES | 29

Is weakness in Somero Enterprises shares a great opportunity or a value trap?

VALUE TRAP OR LONG-TERM OPPORTUNITY?

Somero designs and manufacturers top of the line laser-guided concrete floor flattening equipment that is becoming vital for the acres of automation-laden warehouse space needed as more businesses embrace digital commerce.

That said, the company’s long-term growth profile suggests structural growth despite the ups and downs of the general economy. Somero has grown net profit by a CAGR of 15% a year since floating in 2006.

odd, given clear momentum in the business, rising cash balances and higher dividends. Finncap estimates the shares offer almost a 10% dividend yield based on the expected 2023 pay out.

A management vacuum could attract predatory activity. Shares recently highlighted the company could be vulnerable to a takeover by private equity.

Earnings per share have grown at a CAGR (compound annual growth rate) of 20% a year over the last five years which arguably qualifies Somero as a growth share.

Had the market viewed the company as a growth stock the brutal share derating (falling PE) might be understandable. After all, growth stocks have been heavily punished in the last year as interest rates have risen.

oncrete levelling specialist Somero Enterprises (SOM:AIM) has seen its PE (price to earnings) ratio sink almost 40% to 7.9 times since the start of the year, despite 2022 earnings estimates rising by 10%.

But investors have seemingly been reluctant to attach a growth PE multiple to the stock. This is perhaps understandable given the cyclicality of Somero’s business which serves the construction industry.

Succession planning is a potential worry given the ages of CEO Jack Cooney (74) and chair Larry Horsch (87). Notably, Cooney has been selling shares over the last few years but still owns around 2% of the company.

Even a record first half performance wasn’t enough to reverse continued weakness in the shares which are around 30% lower than the peaks in ThisJanuary.looks