Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineHow much risk are you prepared to take with investing?

Investing is about maximising returns for a given level of risk. The problem is each investor’s risk appetite and circumstances will be slightly different and so getting the right balance is a key factor in setting up a sustainable investment strategy.

In this feature we look at what risk appetite means, the methods the wealth management industry has developed to measure risk attitude and how that drives asset allocation.

This author took an online risk appetite questionnaire developed by investment manager Royal London, and some of the key takeaways will be revealed later in the article.

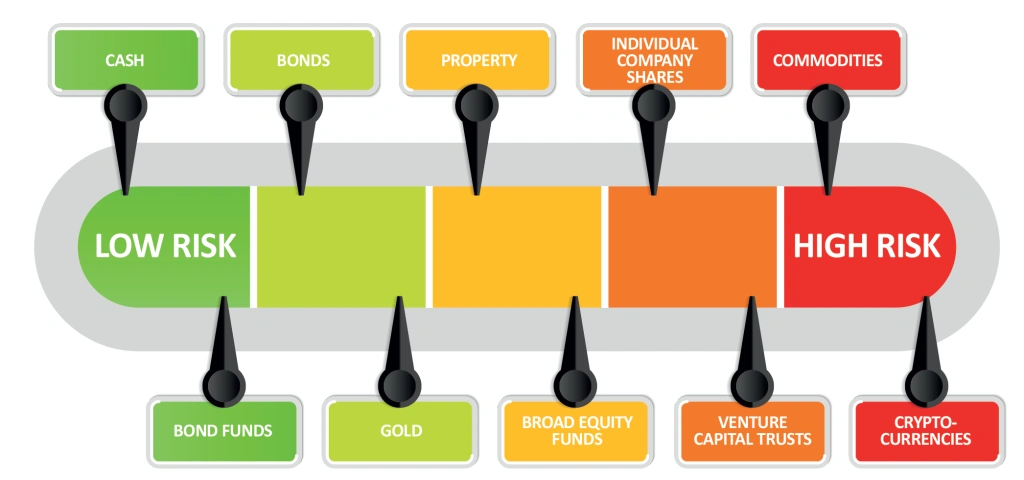

WHAT IS RISK?

It is tempting to think of risk as negative, something that is undesirable, but the nature of investment risk is more nuanced. You might think it better to reduce risk to its lowest possible level, but that fails to account for the return part of the equation.

In a second quarter 2022 investment letter Jonathan Ruffer, founder and chairman of the investment firm which bears his name said: ‘Our job is to put risk in portfolios and try (on a one-year rolling basis) not to lose money.’

US treasuries are widely considered to be the closest thing to a risk-free investment, but while allocating 100% of capital into them is relatively safe, their return potential is low compared with putting money into shares or property.

Every investor should strive to build a diversified portfolio of investments because that helps to smooth the natural ups and downs of investing. It then comes down to how much risk each investor can tolerate while staying the course.

After all, investing is a marathon, not a sprint. The longer you stay invested the better the chance of achieving your investment goals.

Individual temperament and psychological make-up will determine the right amount of variability suitable for every investor. There is a deep trove of academic research which underpins behavioural science.

VOLATILITY AS A MEASURE OF RISK

The investment industry defines risk as volatility which essentially measures how much the value of your portfolio moves around monthly or quarterly.

If you are a nervous type who prefers relatively steady returns, you might be categorised as a cautious investor.

The wealth management industry is required by the regulator to classify their clients into risk baskets and only provide suitable products for their individual needs.

Some investment managers have developed questionnaires designed to get into the head of the client to understand risk appetite.

Questionnaires differ but they often take the form of several statements which invite possible responses.

One example is ‘I associate the word risk with the idea of opportunity’. The client is given five responses, from ‘strongly agree’ at one end of the spectrum to ‘no opinion’ in the middle and ‘strongly disagree’ at the other end of the spectrum.

If a client chooses the first response, they will likely get a higher risk score. Another statement might be ‘I generally look for safer investments even if that means lower returns.’

These attitudes to risk are scored from high (very adventurous) to low (very cautious). Personal information such as age, investment experience, the value of assets owned, and retirement date is also collected and affects the outcome.

Investors who show they are more comfortable achieving stable returns which move around less, are considered by the industry to be at the cautious end of the risk spectrum.

In the aforementioned Royal London questionnaire, this author was categorised as a ‘moderately adventurous’ investor. This means a ‘willingness’ to take investment risk and an understanding that it is crucial to generating long-term returns.

It also implies an understanding that occasional poor outcomes are an unavoidable part of long-term investment.

FINDING THE RIGHT BALANCE

Long-term studies of different asset class returns show a close relationship between return and volatility (risk).

Shares have provided the highest historical returns but are the riskiest while cash and government bonds provide the lowest returns but are more stable.

This risk and return framework can be used by wealth managers to theoretically provide a personalised investment plan.

WHAT DOES IT MEAN FOR RETURNS?

You might be wondering what this means for asset allocation and potential returns. How much more return might be possible for an adventurous investor compared with other risk types?

Investors willing to accept more variability in annual returns (volatility) and deeper drawdowns (percentage loss from peak to trough) are typically allocated a higher proportion of shares.

Adventurous investors might end up with more capital than cautious investors over a 20-year timeframe. But adventurous types would also need the fortitude to accept the possibility of a bigger annual loss along the way.

Although only three risk types feature in the accompanying graphics, in practice there could be several layers of different risk profiles and appropriate asset allocations.

It is important to understand the projections are made based on past returns which may not be representative of future returns.

Over the past year bonds have not provided their traditional stable positive returns. The Bloomberg global aggregate bond index is down around 15% year-to-date.

Rising interest rates and surging inflation have had a punishing effect on bond prices. However, this must be seen in the context of the prior years of negative interest rates and low inflation.

With 10-year US government bond yields now close to 3%, up from around 1% a year ago, there has been a big price adjustment.

DISCLAIMER: Financial services company AJ Bell referenced in this article owns Shares magazine. This article was edited by Tom Sieber who owns shares in AJ Bell.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Education

Feature

Great Ideas

News

- Collapse of Elon Musk’s Twitter deal could spark Tesla share price recovery

- Kistos aims for £1 billion tie-up with Serica to create North Sea oil and gas champion

- The 2022 AGM season is seeing shareholder rebellions on pay gather pace

- The big US companies reporting over the next week and what it could mean for the economy

- Latest Fundsmith letter offers investors comfort despite tough market conditions