Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineThis is how to find a winning combination of cheap stocks and inflation protection

In an inflationary environment buying an investment trust which offers exposure to both cheap equities and alternative assets like infrastructure which have inflation protection looks a sensible approach.

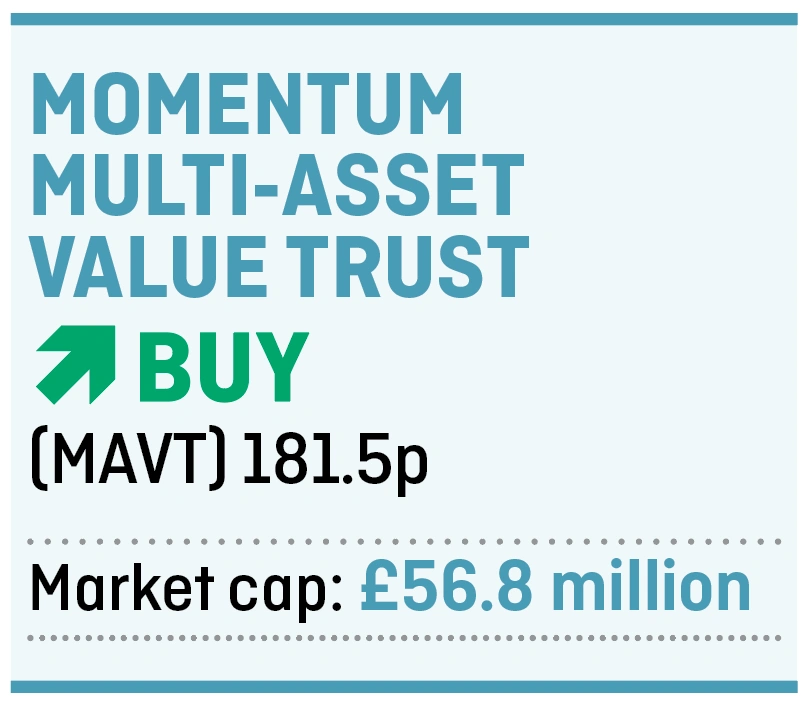

Shares has identified just such a vehicle in the form of Momentum Multi-Asset Value Trust (MAVT). The shares trade at a 1% discount to net asset value and offer a historic yield of 3.7% with dividends paid quarterly.

The near-£60 million trust has a stated aim of achieving at least the level of CPI (consumer price inflation) plus 6% a year (a potentially tall order in the current strong inflationary environment) by investing in UK and overseas shares as well as bonds and specialist assets like private equity, infrastructure and financial products.

Previously called Seneca Growth & Income Trust

Established more than 25 years ago, the vehicle has gone through several iterations in the interim, most recently changing its name from Seneca Growth

& Income Trust in February 2021 after Momentum Global Investment Management bought Seneca Investment Managers.

The latter was a Liverpool-based firm launched in 2002 focused on a multi-asset

and value-focused approach. Day-to-day running of the portfolio did not change as a result of the deal.

UNUSUAL APPROACH

The trust is unusual in that it combines a focus on value with a multi-asset strategy and we think this could be a winning combination in the current environment.

As of 31 January 2022, the portfolio was split approximately one third in UK shares, just over a fifth in overseas stocks, 7% in bonds, and another third in specialist assets like infrastructure, private equity, specialty finance (including areas like music royalties) and property.

The remainder is in cash and defensive assets like gold and government bonds. Interestingly the specialist assets accounted for nearly half of the income generated.

The four-man management team behind the trust pick the UK stocks and shares component themselves but use third party investment trusts and funds to access other asset classes and markets.

When it comes to identifying attractively valued UK stocks the managers use metrics like price to book, price to sales and CAPE (cyclically adjusted price to earnings). They will then take a deeper dive into how the earnings are generated and where they are coming from.

Recent additions to its portfolio from the UK market include fantasy miniatures firm Games Workshop (GAW) and the digital publisher behind Ladbible, LBG Media (LBG:AIM). Lead manager Gary Moglione says: ‘LBG has monetised Facebook really well and it’s now participating in trials with Instagram and TikTok to try and monetise its videos there. Ladbible has a huge following on both those platforms but it’s not being monetised.’

INVESTING THROUGH NICHE FUNDS

Moglione tells Shares the approach with the rest of the portfolio is to invest through so-called ‘boutique’ asset managers which might not be as familiar to investors. These are typically smaller and have a more specialised approach.

He adds: ‘We have a strong belief that a small assets-under-management, family-owned business where the manager eats their own bucket has a different mentality to a manager who’s on a fund that’s a £20 billion cash cow, needs to stay close to the benchmark and just not underperform.’

He says the team’s own analysis suggests there is a performance premium of just over 1% for boutique funds ‘because the manager’s mindset is all on performance in a boutique’.

Further summing up the approach behind the trust he explains: ‘We don’t have a house view. Attempting to predict the future has at best a hit rate of 50%. Instead, we focus on the strong correlation between valuations and the performance of asset classes over the long term. We just have to remain disciplined and patient.’

MANAGING THE RISKS

As Moglione acknowledges there are risks associated with investing in value. ‘You’ll never eliminate these entirely,’ he says. ‘It’s about minimising your losses and maximising your gains.’

He says the fund has a robust process whereby any potential new addition to the portfolio must meet with the whole team’s approval after heavy scrutiny and there is competition for capital whereby managers can argue they have a potential investment which should replace an existing holding.

This has underpinned a decent level of performance over time. As of 31 January 2022, the trust had delivered a five-year return of 40.6%.

The trust uses gearing (borrowing to invest) to help boost returns, with a current gearing level of 11% of its net assets, and it can go as high as 25%. The ongoing charge at 1.63% is relatively high but reflects the complexity and range of investments included in the portfolio.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Feature

Great Ideas

- Find out why WH Smith remains an exciting Covid recovery play

- A tight power market continues to drive earnings upgrades at Drax

- Why we’re sticking with formidable long-run performer Fidelity Special Values

- 2022 should prove a pivotal year for GlaxoSmithKline

- Shares in comparison website owner Moneysupermarket are too cheap to ignore

- This is how to find a winning combination of cheap stocks and inflation protection