Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineRegular investing: how it works and the benefits of putting money aside each month

People are creatures of habit, especially when it comes to the mundane things in life. Creating good financial habits can really pay off later in life and provide more flexibility and freedom. Feeding your ISA or SIPP (self-invested personal pension) every month could be one the best decisions you’ll ever make.

Scientific evidence shows people might have good intentions, but often don’t follow through with them when push comes to shove. The temptation is just too great.

Sometimes individuals simply forget to put money aside, particularly as financial matters are not always at the forefront of people’s daily lives.

Automating the process makes it easier to side-step the behavioural challenges.

The sooner you start investing, the longer your ultimate exposure to the stock market will be and the greater your potential returns. The differences a few years can make may surprise you.

HOW REGULAR INVESTING WORKS

Let’s take a simple example of Joan who sets up a regular automated plan to transfer £100 every month into an ISA after she gets her first job at age 21.

By starting early, Joan hopes to take advantage of the positive effects of investing over longer periods.

David waited until he turned 31 before investing money in the markets.

To keep things simple, we assume both invest the same amount and get the same returns of 6% per year. Their monthly contributions also remain the same over time. Both continue to save until they are 50 years old.

David’s contributions amount to £22,800 and his portfolio is worth £41,816 when he turns 50.

Joan’s contributions are 53% greater because she invests for 29 years versus David’s 19 years. They add up to £34,800 which is an extra £12,000 of money put into her ISA.

However, she benefits from greater time in the market and her investments after 29 years would be worth more than twice those of David at £91,214. The figures do not take account of inflation or investment platform charges.

This simple illustration shows you do not need to have huge disposable income to build a nest egg. Time is as, if not more, important as size.

In fact, David would need to save more than double the amount Joan is saving at £218 a month to have the same value as her portfolio by the time he turns 50.

CHOICES WHEN INVESTING IN A REGULAR SAVINGS PLAN

Most investment platforms provide an automated investment service which takes the manual hassle out deploying savings into the stock market.

Step one is to set up a regular savings deposit into your ISA or SIPP via a direct debit from your bank account.

Step two is to choose the shares, funds or exchange-traded funds in which to invest.

With regular investing schemes, investment platforms will usually amalgamate all clients’ orders and offer a reduced dealing charge (typically £1.50) because they can make the trade in bulk on the same day each month.

This not only saves you money, but it means you can invest smaller amounts more cost effectively.

Making regular savings at the same time each month means you are buying at different prices. You buy more shares of what you like at lower prices and fewer at higher prices.

TIMING THE MARKET IS HARD

An alternative to using a regular monthly saving service is to feed your ISA or SIPP with cash and let it build up until you’ve got enough money to invest whereby any charges will only represent a very small percentage of the transaction amount.

Getting the timing wrong can lead to short-term losses which will be magnified by the larger amount invested. This can be demoralising and lead to feeling of regret and lost confidence.

Your temperament is an important factor in how you deploy the cash. Always try to keep a long- term focus.

Also, remember that accumulating cash means you are not investing in the market.

A study by Vanguard showed the FTSE All-World index has ended higher than the previous month in almost two out of every three months since the index was launched at the end of 1993. In other words, waiting can be costly.

Whichever method you decide is best for you, the advantages of starting a regular saving plan as early as possible is the best way to secure your financial goals.

Regular investing in practice

EXAMPLE 1

We’ve created a hypothetical company called Light Up The Sky to illustrate how regular investing might work in practice.

Shares in Light Up The Sky started the year at 100p and ended the year at 300p.

Investing £1,200 as a lump sum meant you could have bought 1,200 shares (£1,200 / 100p) at the start of the exercise. After 12 months your investment would have been worth £3,600 (300p x 1,200).

If you could only afford to invest £100 a month, you would have invested the same amount after a year as the lump sum investor (£1,200) yet bought a different number of shares.

Accounting for the ups and downs of the market, your £100 would buy a varying number of shares almost every month. After one year in the Light Up The Sky example above, you end up with 544 shares worth £1,632 (300p x 544). That is less than half if you’d invested the lump sum.

The shares saw lots of ups and downs but ended the year higher than the starting point.

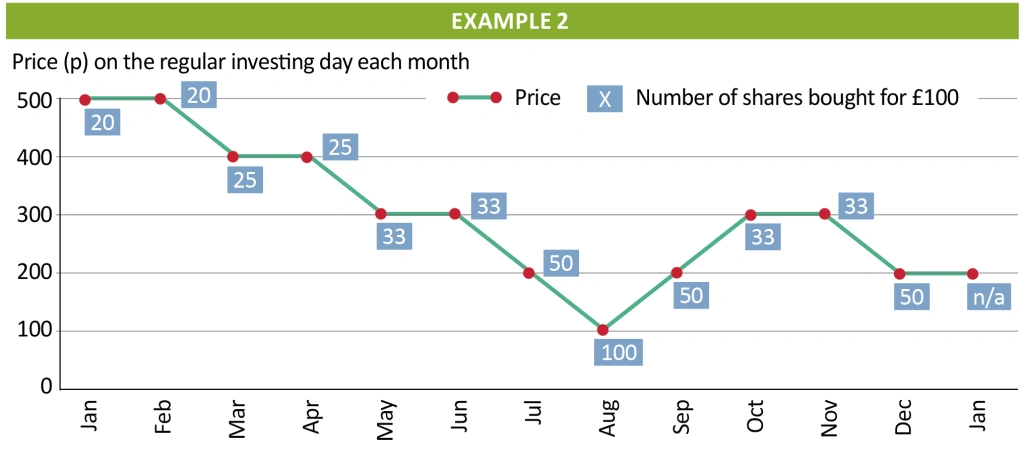

EXAMPLE 2

The second example looks at another hypothetical company called Bike Frame Expert whose shares started at 500p and ended the year at 200p.

Investing the same £1,200 lump sum would have got you 240 shares (£1,200 / 500p) if bought at the start of the year. At the end of the year they would have been worth £480 (200p x 240).

Going down the regular investing route at £100 a month would mean you bought more shares for your money as the year progressed, thanks to the share price falling.

You would have ended the year with 472 shares worth £944 (200p x 472). That’s nearly twice as much as the lump sum route.

Unfortunately, no-one knows how share prices will behave in the future, so it is impossible to say with accuracy which method is better. However, investing every month is the best way to get into the rhythm of putting money away for the future.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Feature

- Enough is enough: The FTSE 100 companies which face a grilling from investors

- Specialist distributor Diploma is a rare winner from global supply chain constraints

- How investors including people in retirement should deal with 7% inflation

- A complete exit from Russia is likely to cost companies dearly