Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhich is better - high yield today or dividend growth tomorrow?

Given present geopolitical and economic uncertainties and the stock market declines seen year-to-date, the portfolio support provided by dividends remain important to investors.

Thankfully this year, we have continued to witness a restoration of dividend payments by an array of companies following the hiatus seen in 2020 when firms suspended payouts to preserve cash at the onset of the pandemic.

For years, investors have worried about the sustainability of UK dividends and come to view higher yield stocks as value traps. The UK stock market has its fair share of large caps in more mature, slower growth sectors such as banking, telecoms, tobacco, oil and mining and tobacco sectors, which partly explains why the market’s above-average dividend yield versus other developed markets. During the Covid crisis, some companies did use the pandemic as an excuse to cut their dividends.

But the encouraging news is dividend cover in the UK has improved since the nadir of the pandemic with banking, oil and mining company earnings bouncing back especially strongly.

As Graham Ashby, UK fund manager at Schroders (SDR), explains: ‘What happened with Covid is some of the issues around the sustainability of dividends came to the fore and overall dividends ended 2021 around 20% lower compared with prior to the pandemic.

‘As a consequence, dividend cover is back closer to two times compared to 1.5 times for a number of years prior to the crisis. We are in a stronger position than we have been for a while for dividend growth and the sustainability of yields.’

THE INCOME TRADE-OFF

Income investors have always faced a trade-off between maximising their income today and growing dividends in the future and there is no right or wrong answer when selecting a fund, trust or stock for income.

A 70 year-old retiree wouldn’t be well served by a strategy that delivers higher levels of annual income at a timescale beyond their life expectancy. Conversely, a younger investor seeking to build up a pool of income generating assets to fund a future retirement might choose to forego present income with a view to enhancing future income streams.

High dividend paying stocks are often well-established businesses that generate lots of distributable free cash, yet are mature with limited growth prospects. Dividend growth companies on the other hand tend to pay lower yields as they reinvest part of their cash flows to generate future growth, though dividends of smaller companies are, in general, more volatile but they enjoy higher cover.

GRAPPLING WITH THE DILEMMA

‘It is a dilemma that we grapple with day in, day out,’ says Matthew Bennison, UK Equity Fund Manager at Schroders. ‘The approach that we take in the Schroder Income Growth Fund (SCF) and Schroder UK Alpha Income (B7F32Y0) fund is a “barbell” approach, very much designed to balance our requirement for yield today versus growth tomorrow.’

Bennison explains that ‘if you focus too much on the former, you can crowd into companies that are perhaps overdistributing or don’t have high enough growth prospects and you are unlikely to beat inflation with the growth in the income in the medium term.

‘Focus too much on the latter and you are less likely to be able to satisfy your income requirements today. If you just have a portfolio of low yielding high growth companies, the absolute yield might only be 1.5%-2% of the portfolio and that is probably unlikely to satisfy the requirements of an investor that is probably looking for 4%.’

With these aforementioned funds, Schroders ‘blends the two aspects together’ to give a premium yield to the market with dividend growth ahead of inflation. Large high yielders at the value end of the spectrum provide the yield today, while the ‘more exciting, more innovative, more growthy companies that have strong franchises and cash generative models’ deliver the dividend growth of tomorrow.

TRUST OPPORTUNITIES

In a recent piece of research John Dowie, analyst at investment trust researcher Kepler, pointed out it is important for investors to ‘make careful consideration of whether a trust is tilted towards generating a high yield as soon as possible or is orientated towards dividend growth when selecting an investment, in order to make sure it suits their needs and time horizons.’ Fortunately, the investment trust space has a mixture of approaches that should meet most requirements.

Dowie drew attention to Troy Asset Management, which has committed to dividend growth in both Securities Trust of Scotland (STS), the global equity income trust Troy took over management of in late 2020, and in UK equity income trust Troy Income and Growth (TIGT).

Troy has rebased the dividends for both to allow for more robust and sustainable future dividend growth, reflecting its view that the current dividend/dividend growth dilemma will become exacerbated over time due to the diminishing quality and growth prospects of today’s large, incumbent, old economy dividend payers.

Speaking to Shares about Securities Trust of Scotland, manager James Harries explained: ‘We are trying to build an optimum balance of quality, income and growth. We have a yield of about 2.7% today and we think that will grow pretty consistently. And we were also keen to rebuild the revenue reserve, which we are doing, so that we can be more secure and certain and give investors a more resilient growing income over time.’

Other trusts with allocations to high dividend payers and stocks with good dividend growth prospects include Aberdeen Standard Equity Income (ASEI), which has 21 years of consecutive dividend growth under its belt and greater exposure to small and mid caps with better capacity for dividend growth than many UK equity income peers.

According to the Association of Investment Companies, the trust boasts a bumper 6.1% yield and also has an attractive five year dividend growth per annum rate of 6.6%. Manager Thomas Moore recently told Shares ‘it is possible for a high yield trust to be achieving dividend growth. I don’t think the two things are incompatible.’

Also shifting to more of a barbell strategy is BMO UK High Income (BHI), whose manager Philip Webster has transitioned the portfolio from a more traditional approach to UK equity income investing to a highly active and often contrarian style, investing in high-quality, innovative firms with attractive growth prospects.

WHY HIGH YIELD WORKS

Simon Gergel manages Merchants Trust (MRCH), which offers an attractive 4.9% dividend yield according to the AIC website. Merchants seeks to provide an above average level of income, income growth and long-term growth of capital through a policy of investing mainly in higher yielding large UK companies.

Holdings span Scottish & Southern Energy (SSE), Shell (SHEL) and Rio Tinto (RIO) as well as retailers Next (NXT) and Tesco (TSCO) and dividend growth stocks DCC (DCC) and Homeserve (HSV).

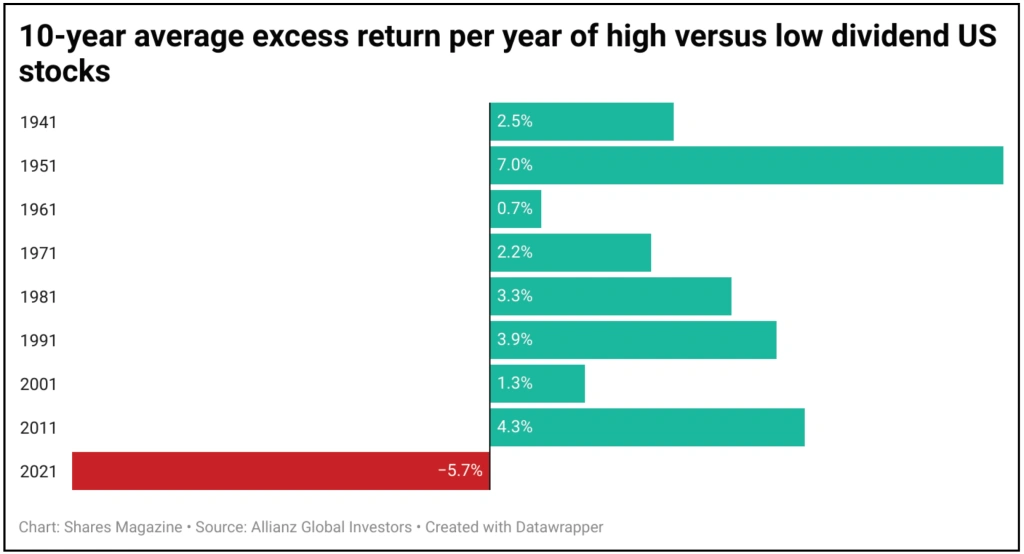

‘There’s a lot of evidence that high yielding shares have historically performed well,’ Gergel recently told Shares. Not so much in the last few years when investors have chased growth names higher, ‘but over longer periods of time, definitely’.

Gergel hasn’t ‘seen the evidence that dividend growth necessarily works particularly well’. He pointed out many of the companies with the highest dividend growth ‘tend to have the highest ratings because they tend to have the highest earnings growth, and high valued companies tend to underperform over time, statistically.

‘That doesn’t mean that you can’t make money as a growth investor, but I’m not sure there’s evidence that high dividend growth has been a particularly successful investment style.’

Whereas some posit that if you’d bought the companies with the best dividend growth of the last decade you’d have made a fortune, the difficulty according to Gergel is ‘you would have had to identify 10 years ago which companies were going to have the best dividend growth and avoid the ones which blow up along the way’.

As for Merchants, Gergel explained: ‘We tend to find over time that we get underlying dividend growth out of our portfolio but that’s supplemented by this rotation effect, where you might buy a company with a yield of 5% and sell it when it has got a yield of 4% because it goes up 25%.

‘And then you’ve got more money to invest back in at a yield of 5% again, and by doing that you actually boost the income by a substantial amount over time. We get underlying dividend growth but we also get an element of income increasing from this rotation factor.’

Though he fishes in a pond of high yielding stocks, Gergel stressed that ‘identifying and avoiding value traps is absolutely critical for any value style and we never buy a company just because it has got a high yield – we only buy companies where we think can make money.’

SUSTAINABLE PAYOUTS

Also weighing in on the debate is Mark Whitehead, who co-manages the Sanlam Sustainable Global Dividend Fund (B518H39) with Alan Porter using a bespoke sustainability scorecard, in addition to excluding companies with more than 10% exposure to alcohol, tobacco, gambling, weapons, adult entertainment, and fossil fuel extraction.

‘Over the 15 or so years that I have been investing in dividend paying companies I believe focusing on a company’s ability to pay a dividend consistently and to grow it throughout the business cycle could be the best approach to take for more reliable returns,’ said Whitehead.

Simply selecting a company with a high yield, however attractive, can ‘very often lead to sub-optimal outcomes for investors’, he warned.

‘Companies exhibiting a high yield very often do so for a reason. The share price may have fallen and therefore the yield is artificially high indicating that the company is not performing. Or the company operates a high earnings pay-out approach as they have nothing better to do with the cashflow they are generating, as the returns on reinvestment in their business are poor.’

Whitehead also noted that looking at past performance, no guide to future returns of course, ‘the MSCI World Dividend Masters Index has consistently outperformed the MSCI World High Dividend Yield Index over long periods. The latter has a higher yield premium to the MSCI World Index, confirming that overreaching for yield can be detrimental to total returns.

‘That’s why we favour companies that can grow their revenues, earnings and cashflows, even in more difficult operating environments, whilst maintaining their asset bases and re-investing into future growth opportunities. These attributes, combined with prudent balance sheets, liquidity management and sustainability leadership, offer the potential of superior returns to shareholders. These qualities are the hallmark of a successful dividend paying company.’

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

Feature

- Why Magners maker C&C can cope with unprecedented cost inflation

- Fighting cyber attacks: Invest in the world's digital defenders

- Which is better - high yield today or dividend growth tomorrow?

- New world order: the big impact of a geopolitical earthquake

- Private equity has made a lot of people rich – how do you get invest in it?

Great Ideas

- BlackRock Throgmorton is a great fund for a small cap recovery rally

- Cordiant Global Infrastructure remains a way to play the growth in digital assets

- Why Berkshire Hathaway is hitting fresh highs

- FDM shows substantial recovery potential at shares rally 21% in two weeks

- US growth can drive undervalued Homeserve shares higher

- Essentra to become a streamlined components champion

News

- Chancellor Sunak’s spring statement full of surprise support measures

- Ferguson to leave the FTSE 100 in May as it focuses on the US

- Robust results from Nike as direct to consumer strategy delivers

- IG and Plus500 venture overseas with mixed success

- Hospitality enjoys good times despite spending pressures

- Value and inflation protection leave FTSE 100 well placed

- Hong Kong suspends shares in Chinese property giant Evergrande