Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineDeere still going strong after 185 years at the forefront of farming

With its signature green and yellow branding, Deere may be the most recognisable tractor maker in the world, but it does a lot more besides selling farm equipment.

With the war in Ukraine highlighting the importance of food production and food security as well as efficient farming practices, Deere’s cutting edge agricultural equipment could be in strong demand.

Many of its products use up-to-the-minute technology which both save time and money and also improve sustainability, an increasingly important consideration as environmental concerns move to the forefront.

While it can trace its history back to 1837, and still has its group headquarters in Illinois, the company is far from being stuck in the past.

A LEADER IN ITS FIELD

From its origins as a plough maker, Deere hit the jackpot just under a century ago in 1923 with the introduction of the Model D tractor.

Originally equipped with a 30hp engine, the Model D turned mechanised farming into a reality in the US and was so popular production lasted 30 years.

During the Depression, farming was probably the hardest occupation in America as the global economic slowdown coincided with one of the worst and longest droughts in US history.

The firm survived, however, and in 1945 it introduced the Model M with its Quick-Tatch system of attaching implements, another quantum leap forward in farming.

Always looking for ways to improve its products, in 1954 Deere was the first firm to introduce power steering on its tractors.

This was followed by power brakes, a cab for protection and eventually functions such as air conditioning and dust filtration.

Today, Deere employs more software engineers than mechanical engineers and its tractors are jam-packed with the technology.

They employ precise global navigation satellite systems technology, advanced connectivity and telematics, on-board sensors and computing power and automation software.

Guided by sat-nav, they can ‘tell’ the spraying boom which plants are weeds and which are crops so that only the weeds are sprayed with pesticide.

At an average 12 miles per hour, that means the tractor and the boom are monitoring around 2,000 square feet per second, which makes it an incredibly efficient way of treating weeds.

It also cuts down the use of pesticides, which is important for farmers trying to establish a balance between higher yields and sustainability.

Using advanced telematics, the tractor’s systems can even connect equipment owners, business managers and dealers to equipment in the field to provide real-time alerts and information about its location, utilisation, performance and maintenance.

In January the firm unveiled an autonomous tractor. And in 2021 chief technology officer Jahmy Hindman told Decoder, a podcast produced by US tech news site The Verge, that ‘operatorless operation in, say, fall tillage or spring planting, we’re right on the doorstep of that.

‘We’re knocking on the door of being able to do it.’

STRUCTURE AND PERFORMANCE

The firm is organised into four divisions, the two largest of which are dedicated to agricultural machinery and make up roughly two thirds of sales.

Production and Precision Agriculture develops and manufactures equipment and technology for production-scale farming such as tractors, combines and seeding and crop care equipment.

Small Agriculture and Turf supplies mid-size and small growers, and also makes production systems for dairy and livestock. Products include small tractors, ride-on mowers, golf course equipment and utility vehicles.

The Construction & Forestry division manufactures earth movers, material handling, timber harvesting and road building equipment and accounts for roughly a quarter of sales

The fourth division is Financial Services, which provides credit to buyers of Deere equipment and makes up roughly 10% of sales.

In the financial year to October 2021, the firm generated net sales of $44 billion compared with $35.5 billion the previous year.

Equipment sales reached $39.7 billion compared with $31.3 billion the previous year, an increase of 27% thanks to a combination of higher volumes and higher selling prices.

Operating profits for the equipment business almost doubled from $3.56 billion to $6.87 billion thanks to more sales of high-margin products and a gain on the sale of a factory in China.

Net income for the equipment business more than doubled from $2.18 billion to $5.08 billion, while net income for the financial services business increased 55% from $556 million to $881 million.

At a group level, cash flows from operations were $7.73 billion, which allowed the firm to buy back $2.54 billion of its own shares and pay out $1 billion in dividends, so shareholders were well rewarded.

CURRENT TRADING AND OUTLOOK

In the first quarter to 30 January, revenues were $9.57 billion against a FactSet consensus of $8.28 billion, with net sales from equipment operations alone reaching $8.53 billion.

Net earnings per share were $2.92, below last year’s figure of $3.87 per share due to higher production costs and supply chain bottlenecks but significantly ahead of the FactSet consensus of $2.27 billion.

By division, the firm is expecting 25% to 30% revenue growth in its Production and Precision Agriculture business, 15% growth in Small Agriculture and Turf and between 10% and 15% in Construction and Forestry.

Chief executive John C. May raised full year net earnings guidance for the group from $6.5 billion to $6.7 billion to between $6.7 billion and $7.1 billion citing the ‘strong fundamentals’ of demand for farm and construction equipment.

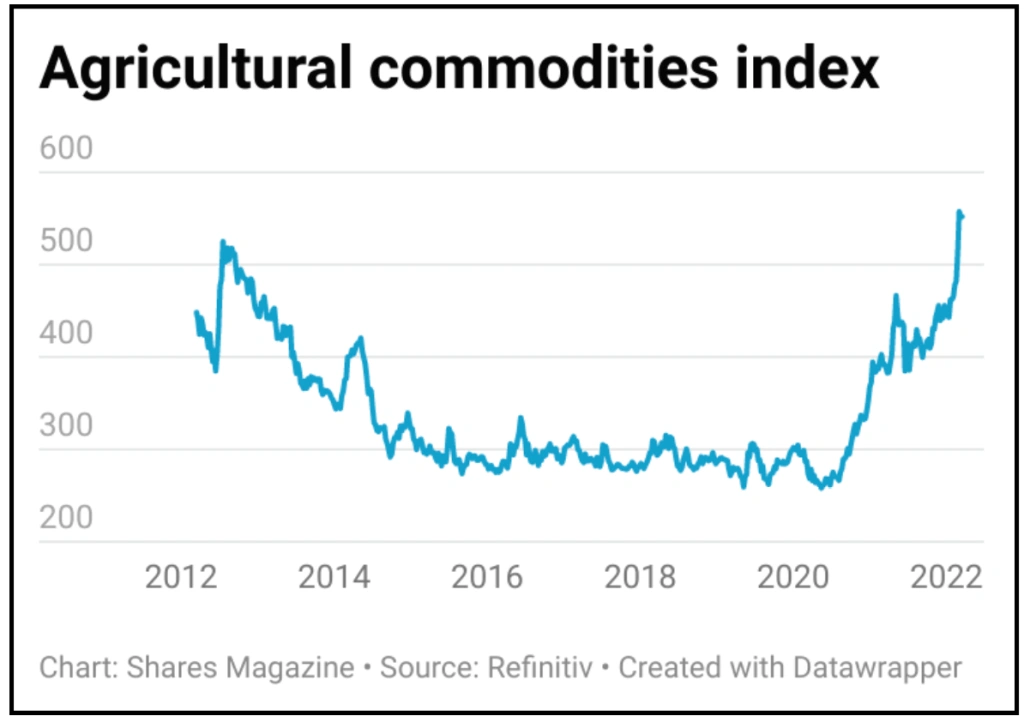

Zacks Equity Research says the ongoing rally in commodity prices will continue to fuel agricultural equipment demand, encouraging farmers to boost spending on new farm equipment.

It points out that corn and soybeans are the most important grains for cash crop farming in the US. Given Russia and Ukraine account for around a fifth of global corn output, prices are likely to keep rising.

At the same time, owing to high potash prices, farmers are opting to cultivate soybean as it is a less fertiliser-intensive crop. With soybean prices also rising, farm income is growing meaning more demand to upgrade old equipment.

Meanwhile, Deere’s construction equipment business is likely to benefit from growth in non-residential investment and strong order activity from independent rental companies.

Global roadbuilding markets are expected to be up between 5% and 10%, with growth in the North American market offsetting some weakness in China, adds Zacks.

Morningstar believes the big issue for heavy machinery firms like Deere isn’t demand but supply, although it sees pressures easing over the course of the year.

‘Deere’s first quarter results showed its continued resiliency despite a challenging operating environment’, says analyst Dawit Woldermariam.

Pressure on margins will start to reverse in the next couple of quarters, according to Woldermariam.

Deere’s position as a premium equipment maker gives it the ability to consistently raise prices through the cycle, he adds.

OWNING DEERE

UK investors can buy shares in Deere directly, although dealing charges are typically higher for overseas shares than for UK shares and there are also foreign exchange charges to take into account.

For those looking for a broad exposure to agriculture as a theme there are a couple of funds worth considering.

The Pictet Nutrition Fund (B54YLC1) invests in companies developing solutions to help secure global food supplies, including improving farming productivity and maximizing the nutritional content of what we eat.

The fund’s biggest position is Deere, followed by Dutch ingredients firm DSM and Irish nutrition company Kerry Group (KYGA).

The fund has lagged the MSCI World Index in sterling over the last six months, which might make this a good time to take a closer look especially as it only has an ongoing charge of 1.1%.

The Sarasin Food & Agriculture Opportunities Fund (B77DTQ9) also lists Deere as its number one holding and has also under-performed its benchmark, although it has a ongoing charges of 1.75%.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

Feature

- Why Magners maker C&C can cope with unprecedented cost inflation

- Fighting cyber attacks: Invest in the world's digital defenders

- Which is better - high yield today or dividend growth tomorrow?

- New world order: the big impact of a geopolitical earthquake

- Private equity has made a lot of people rich – how do you get invest in it?

Great Ideas

- BlackRock Throgmorton is a great fund for a small cap recovery rally

- Cordiant Global Infrastructure remains a way to play the growth in digital assets

- Why Berkshire Hathaway is hitting fresh highs

- FDM shows substantial recovery potential at shares rally 21% in two weeks

- US growth can drive undervalued Homeserve shares higher

- Essentra to become a streamlined components champion

News

- Chancellor Sunak’s spring statement full of surprise support measures

- Ferguson to leave the FTSE 100 in May as it focuses on the US

- Robust results from Nike as direct to consumer strategy delivers

- IG and Plus500 venture overseas with mixed success

- Hospitality enjoys good times despite spending pressures

- Value and inflation protection leave FTSE 100 well placed

- Hong Kong suspends shares in Chinese property giant Evergrande